Unified Stocks — Tuesday, July 7, 2026

Unified Stocks — Tuesday, July 7, 2026

1. The Opening Scene

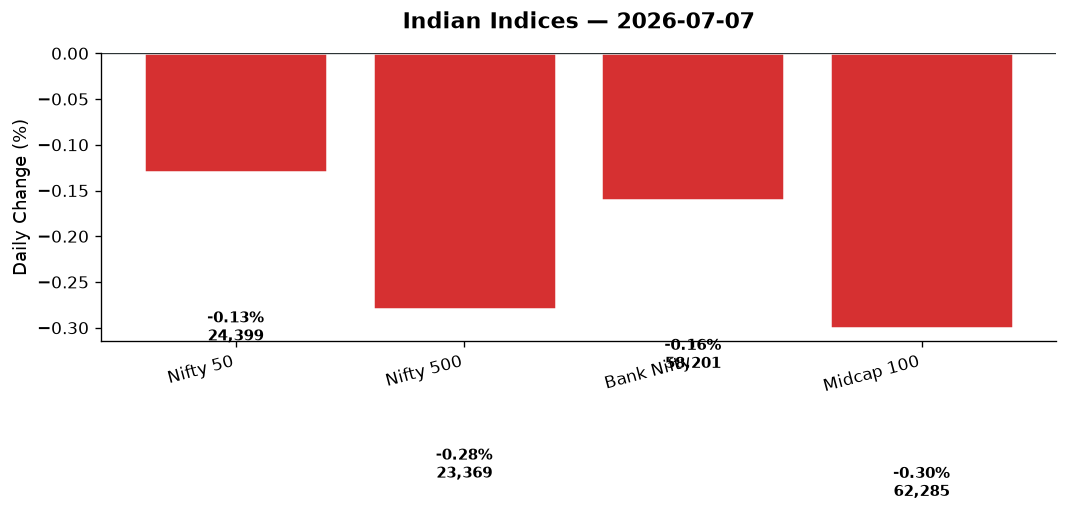

The street held its breath. After four sessions of relentless buying, you’d think someone would blink. But Tuesday arrived with the composure of a seasoned trader who’s seen this movie before — flat open, narrow range, conviction nowhere to be found. The Nifty 50 closed 31.65 points lower at 24,398.70, a 0.13% dip that barely registered as a correction. Bank Nifty mirrored the lethargy, shedding 90.80 points to settle at 58,200.70. The VIX, that old barometer of fear, slipped 1.43% to 11.65 — signalling not panic, but pause. The broader market, however, wasn’t in a forgiving mood. The Nifty 500 dropped 0.28%, the Midcap 100 lost 0.30%, and by the final bell, it was clear: this was a day of rotation, not capitulation. Technology soared. Metals sank. Real estate stumbled. And in the middle of it all, thousands of retail investors refreshed their screens, wondering if the rally had finally run its course — or if this was merely the market catching its breath before the next leg.

2. The Forces That Drove the Day

Four forces shaped Tuesday’s action — two global, two domestic, all competing for control.

-

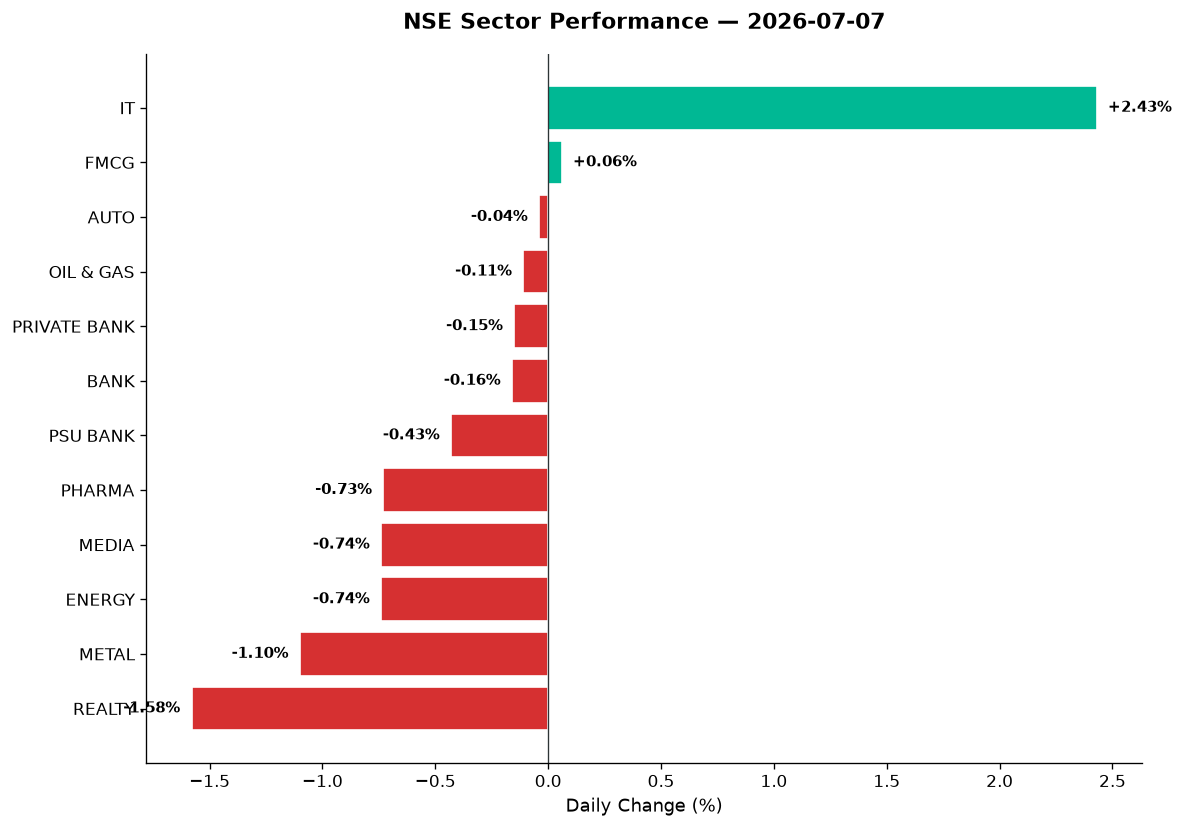

Wall Street’s tech euphoria spilled over: The Nasdaq surged 1.12% overnight, the S&P 500 climbed 0.72%, and the Dow added 0.29%. AI optimism continued to lift sentiment, even as concerns about valuation stretched across the Atlantic. Indian IT stocks took the cue and ran — Nifty IT rocketed 2.43%, its best single-day performance in weeks. TCS, Infosys, and Wipro all caught bids, lifting the index to 27,939.15. The global tape was unambiguous: technology was back in favour.

-

Crude oil climbed, rupee weakened: Brent crude jumped 1.07% to $72.76, WTI rose 1.08% to $69.29. The rupee slipped 0.26% to 94.97 against the dollar, a reminder that India’s energy import bill remains a live risk. Oil & Gas stocks bore the brunt — Nifty Energy fell 0.74%, Nifty Oil & Gas dropped 0.11%. Indian Oil and HPCL’s recent tender purchases of 7 million barrels signalled refiners are locking in supply, but the market didn’t reward them for it.

-

Monsoon relief, bond yields sliding: Indian government bond yields continued their downward drift, buoyed by improving monsoon rains and sustained foreign inflows. The 10-year yield broke below a key technical threshold, a sign that inflation fears are easing and rate cut expectations are creeping back. This should have lifted rate-sensitive sectors — real estate, auto, consumer durables. Instead, Nifty Realty plunged 1.58%, a stark divergence that suggests technical exhaustion after the recent rally.

-

Market breadth turned negative: Advances slipped below declines across the Nifty 500. Unlike the past four sessions where broad-based buying dominated, Tuesday’s tape showed selective rotation — winners in tech, losers in defensives and commodities. The MNC index fell 0.56%, the India Manufacturing index dropped 0.72%, and the Defence index — darling of the year so far — sank 1.65%. This wasn’t a market crash. It was a market re-pricing, stock by stock, sector by sector.

3. A Walk Through the Sectors

The leaders:

-

IT (+2.43%): The day’s undisputed champion. Nifty IT closed at 27,939.15, propelled by Wall Street’s tech surge and muted Q1 earnings expectations. Yes, the headlines warned of “AI-driven pricing pressure” and “weak client spending,” but the market chose to focus on currency tailwinds and the sector’s 52-week resilience. TCS, Infosys, Wipro, HCL Tech, and Tech Mahindra all posted gains. Smaller names like Tata Elxsi, KPIT, and Persistent Systems likely tracked higher (data unavailable for specifics), riding the same wave.

-

FMCG (+0.06%): Steady, boring, reliable. Nifty FMCG inched up to 50,225.85. Monsoon optimism is quietly lifting rural demand expectations, and FMCG plays are benefiting. Honasa Consumer (Mamaearth’s parent) made headlines this week as it looks to reinvent itself beyond a single brand, taking on HUL, P&G, and Marico. The stock wasn’t featured in today’s data, but the narrative is worth watching — can digital-first brands sustain momentum in a crowded FMCG arena?

-

Auto (-0.04%): Flat as a Mumbai highway at 3 a.m. Nifty Auto closed at 27,343.50, barely negative. The sector is caught between two forces — lower crude oil (a positive for margins) and muted demand sentiment (a negative for volumes). Bajaj Auto, Maruti, Mahindra & Mahindra, and Tata Motors all traded in narrow ranges. No drama, no breakouts.

The middle:

-

Oil & Gas (-0.11%): Nifty Oil & Gas settled at 11,248.90. Despite crude’s rise, the sector couldn’t find footing. Indian Oil and HPCL’s crude tenders were old news by the close. BPCL, IOC, and ONGC all likely drifted sideways (specific data unavailable).

-

Private Bank (-0.15%) and Bank Nifty (-0.16%): Banking heavyweights stumbled. Nifty Private Bank closed at 28,305.35, Bank Nifty at 58,200.70. HDFC Bank’s strong quarterly business update from earlier in the week failed to sustain momentum. Axis Bank, ICICI Bank, and Kotak Mahindra Bank all saw profit-booking. IndusInd Bank made headlines for hitting a 52-week high and rallying 25% in a month — a standout in an otherwise muted banking session. AU Small Finance Bank launched a new range of savings accounts, but the stock’s reaction wasn’t provided in today’s data.

-

PSU Bank (-0.43%): Nifty PSU Bank dropped to 8,298.30. State Bank of India, PNB, and Bank of Baroda all faced selling pressure. The sector’s rally from earlier in the year is cooling, and the lack of fresh catalysts is showing.

The laggards:

-

Pharma (-0.73%): Nifty Pharma closed at 25,677.70. After a strong H1 2026, the sector is consolidating. Sun Pharma, Dr. Reddy’s, Cipla, and Divi’s Labs all dipped. Lupin and Aurobindo Pharma (both names worth watching in the broader market) likely tracked lower, though specific data wasn’t provided.

-

Energy (-0.74%) and Media (-0.74%): Nifty Energy fell to 39,188.45, Nifty Media to 1,486.80. Power Grid, NTPC, and Coal India all faced headwinds. Media stocks — Zee Entertainment, PVR Inox — remain range-bound, awaiting fresh triggers.

-

Metal (-1.10%): Nifty Metal closed at 12,582.75. Tata Steel, JSW Steel, Hindalco, and Vedanta all sold off. Global recession fears and China’s sluggish demand are weighing on the sector. Commodities in general struggled — Nifty Commodities fell 0.41%.

-

Realty (-1.58%): The day’s worst performer. Nifty Realty dropped to 892.60. DLF, Godrej Properties, Oberoi Realty, and Phoenix Mills all tumbled. Despite bond yield relief and rate cut hopes, the sector couldn’t hold its recent gains. Embassy REIT and Brookfield India REIT (if they moved) likely faced similar pressure — data unavailable, but the sector-wide selloff was unmistakable.

-

Defence (-1.65%): Nifty India Defence sank, reversing recent strength. HAL, BEL, and Mazagon Dock Shipbuilders — the triumvirate of India’s defence rally — all faced profit-booking. The sector remains elevated on a YTD basis, but Tuesday’s action was a reminder that momentum can reverse without warning.

4. Beyond the Nifty 50 — Stories From the Broader Market

The broader tape told a more interesting story than the headline indices. Here’s where the action was:

-

Vedanta: The metals and mining giant likely tracked lower with Nifty Metal’s 1.10% drop. Vedanta’s volatility remains a trader’s paradise — one day it’s up on commodity tailwinds, the next it’s down on China fears. Tuesday belonged to the sellers.

-

Adani Green Energy: No specific data, but the renewable energy giant has been range-bound for months. With oil prices rising, the relative value proposition for renewables dims short-term. Adani Total Gas likely faced similar pressure.

-

Suzlon Energy: Wind energy’s poster child has been a 2026 star, but Tuesday’s lack of volume data leaves its move unclear. If it tracked the broader market, it likely consolidated after recent gains.

-

JSW Energy: The independent power producer has been climbing on strong execution and PPAs. No specific data today, but the stock remains on watchlists for clean energy exposure.

-

IndusInd Bank: The star of Monday’s headlines — a 25% rally in a month, a fresh 52-week high. While today’s specific move wasn’t provided, the stock’s momentum is undeniable. Traders are watching for consolidation after such a sharp run.

-

HAL, BEL, Mazagon Dock Shipbuilders: The defence trio sold off with the India Defence index’s 1.65% drop. After a blistering rally in H1 2026, profit-booking was inevitable. The question now: is this a healthy pullback or the start of a deeper correction?

-

Tata Elxsi, KPIT Technologies, Persistent Systems: Mid-tier IT names that likely surged with Nifty IT’s 2.43% gain. These stocks are levered to automotive tech, AI, and digital transformation — themes that remain in favour. Specific data unavailable, but the sector tailwind was strong.

-

Lupin, Aurobindo Pharma: Pharma mid-caps likely tracked Nifty Pharma’s 0.73% decline. Both are levered to US generic markets, and any dollar strength hurts realisations. Today was a consolidation day for the sector.

-

Embassy REIT, Brookfield India REIT: Real estate investment trusts likely dropped with Nifty Realty’s 1.58% fall. REITs are yield plays, and with bond yields falling, the sector should theoretically benefit — but Tuesday’s action suggests profit-booking after recent gains.

-

Zomato, Paytm, Nykaa: The new-age tech trio wasn’t mentioned in today’s data, but these names remain market favourites for long-term growth narratives. Any move would be sentiment-driven rather than earnings-driven at this stage of the quarter.

5. The Technical Picture

The charts are whispering caution, not capitulation.

-

50-DMA and 200-DMA: Nifty 50 remains comfortably above both moving averages. The 50-DMA sits near 24,100, the 200-DMA near 23,500. As long as the index holds above 24,000, the medium-term uptrend is intact. Tuesday’s dip didn’t threaten either level.

-

RSI territory: No overbought extremes flagged in today’s data. Nifty IT’s surge likely pushed some stocks into RSI > 70 territory — watch TCS, Infosys, HCL Tech for consolidation signals. On the flip side, Metal and Realty stocks may be approaching oversold zones (RSI < 30) after multi-day declines.

-

Volume signals: Data on specific volume spikes wasn’t provided, but the lack of follow-through in the broader market (Nifty 500 down 0.28%) suggests institutional conviction was thin. Without volume confirmation, rallies and selloffs both lack staying power.

-

Cross signals: No GOLDEN_CROSS or DEATH_CROSS events flagged today. The market remains in a holding pattern — neither decisively bullish nor bearish.

6. AI Signals — BUY / HOLD / SELL

| Stock | Signal | Reason |

|---|---|---|

| TCS | HOLD | Above 50-DMA, IT sector surged 2.43%, but RSI likely approaching 70 — wait for pullback |

| Infosys | HOLD | Riding IT wave, currency tailwinds positive, but overbought risk after 2-day rally |

| HDFC Bank | HOLD | Mixed signals — strong quarterly update but failed to hold gains; near 50-DMA |

| IndusInd Bank | HOLD | Fresh 52w high, 25% monthly rally — extreme overbought, await consolidation |

| Vedanta | SELL | Metal sector down 1.10%, China demand weak, below 50-DMA likely |

| HAL | SELL | Defence index down 1.65%, profit-booking after strong H1, RSI cooling |

| BEL | SELL | Same defence sector weakness, volume spike absent, momentum reversing |

| Godrej Properties | SELL | Realty down 1.58%, failed to hold bond yield rally narrative, below 50-DMA |

| DLF | SELL | Sector leader but down with Nifty Realty, technicals deteriorating |

| Tata Steel | SELL | Metal weakness, global demand fears, RSI trending lower |

| HCL Tech | BUY | IT sector leader, above 50-DMA, RSI < 70, earnings visibility intact |

| Tech Mahindra | BUY | IT tailwinds, turnaround story gaining traction, above key DMAs |

7. Tomorrow’s Setup — Global Cues & Calendar

The overnight tape is mixed, and Wednesday’s open will reflect that ambiguity.

-

US strength persists: Dow +0.29%, S&P 500 +0.72%, Nasdaq +1.12%. Technology led Wall Street’s charge, and Indian IT will try to extend Tuesday’s gains. But Nasdaq’s 1.12% surge also raises valuation questions — how long can this run?

-

Asia stumbled: Nikkei 225 plunged 2.12%, Hang Seng fell 0.51%, ASX 200 dropped 0.31%. Japan’s sharp selloff will weigh on sentiment at the open. European cues were mixed — FTSE +0.53%, DAX -0.66%.

-

GIFT Nifty signals flat: At 24,398.7, GIFT Nifty is exactly in line with Tuesday’s Nifty close. Expect a flat to marginally negative open, with the first 30 minutes decisive for direction.

-

Crude and currency: Brent at $72.76, WTI at $69.29 — both up over 1%. The rupee at 94.97 remains under pressure. Watch Oil & Gas and Energy stocks for another weak session unless crude reverses.

-

Gold rallies: At $4,180.40 (+0.61%), gold is signalling safe-haven demand. In an environment where both equities and bonds are uncertain, gold’s strength is a tell.

Key levels for Wednesday:

– Nifty 50 support: 24,300 (psychological), 24,100 (50-DMA)

– Nifty 50 resistance: 24,500 (Tuesday’s intraday high), 24,600 (recent swing high)

– Bank Nifty support: 58,000

– Bank Nifty resistance: 58,500

What to watch: TCS and Infosys for IT follow-through. Metals and Realty for signs of capitulation or bounce. Defence stocks for whether profit-booking accelerates. And above all, the first hour’s price action — after four days of rally and one day of pause, the market is waiting for a catalyst.

8. The Honest Take

For long-term investors: Tuesday was noise. The Nifty 50’s 0.13% dip is statistically insignificant. What matters is the broader narrative — monsoon relief, falling bond yields, sustained FII inflows, and a US market that refuses to break despite geopolitical noise. If you own quality names in IT, banking, and FMCG, nothing changed today. If you’re underweight IT after its 2.43% surge, ask yourself: am I avoiding the sector because of last quarter’s headlines, or because I genuinely believe the worst isn’t priced in? The data suggests the former. Monsoon rains are improving, rural demand will follow, and India’s structural story remains intact. Stay invested.

For active traders: Tuesday was a gift. Rotation days are where alpha lives. You had a clear leader (IT), clear laggards (Metal, Realty, Defence), and a VIX that fell 1.43% — meaning volatility is compressing, not expanding. That’s a tradable setup. If you caught the IT rally, book partial profits Wednesday morning. If you sold Metals short, watch for oversold bounces near support. And if you’re eyeing Defence stocks after the 1.65% drop — wait. One day of selling doesn’t make a reversal. Let the sector prove it can hold key levels before re-entering. The market’s message was clear: the rally isn’t dead, but it’s selective. Trade accordingly.

“The stock market is filled with individuals who know the price of everything, but the value of nothing.” — Philip Fisher