Unified Stocks — Friday, June 19, 2026

1. The Opening Scene

The exchange that lists India’s dreams filed to list itself.

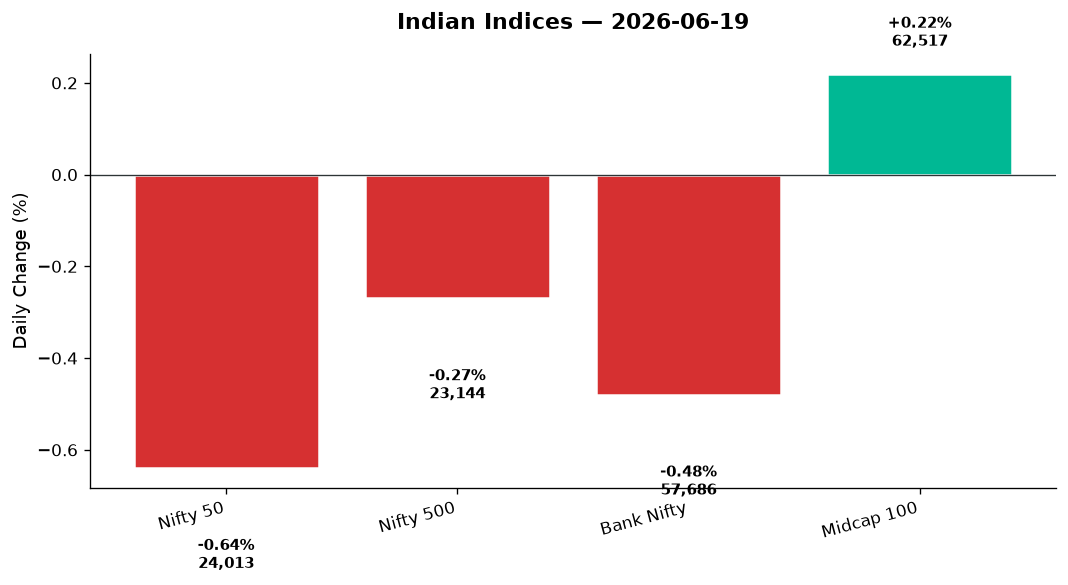

That headline—NSE’s decade-delayed IPO papers finally landing with SEBI—should have been the confetti moment of the week. Instead, Friday’s tape told a different story. The Nifty 50 slipped 154.90 points to 24,013.10, down 0.64%, as if the market paused mid-celebration to check the fine print. Bank Nifty shed 278 points. The VIX ticked up 2.34% to 12.97, a whisper of caution in an otherwise calm ocean.

But zoom out. This was the fifth straight session of gains before today’s dip. Brent crude cooled to $79.64. The rupee firmed to 94.31 against the dollar. And beneath the surface, the Midcap 100 climbed 0.22%—a sign that breadth, not benchmarks, was the real story. The Nifty 500 fell just 0.27%, proof that selling was surgical, not systemic.

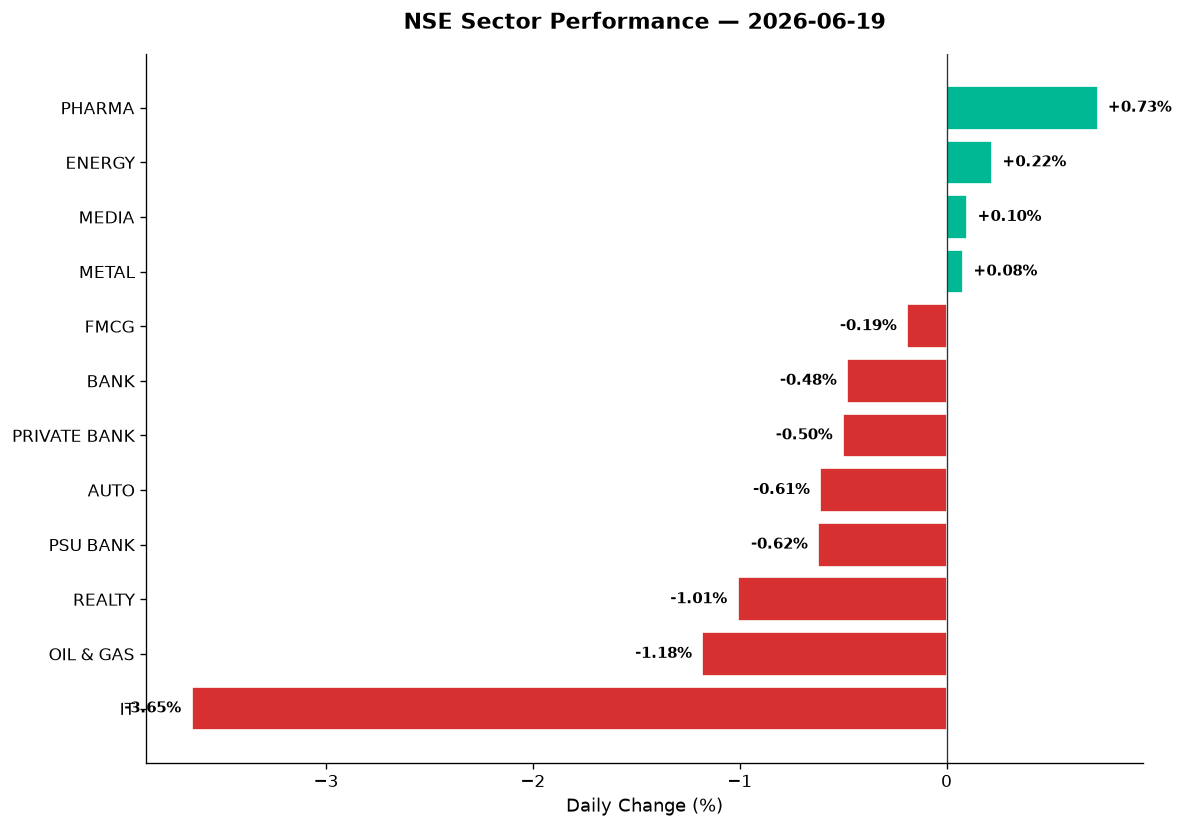

Wall Street handed us a gift overnight: the Nasdaq surged 1.91%, the S&P 500 added 1.08%. Yet India’s IT index bled 3.65%. That disconnect—between global optimism and domestic reality—is what made today’s session fascinating.

2. The Forces That Drove the Day

Four crosscurrents shaped Friday’s action:

-

Oil’s retreat: Brent crude down 0.26%, WTI off 0.89%. That’s real money saved for importers, real basis points of inflation relief. Bond traders noticed—Indian 10-year yields extended their sixth day of rally, as noted in The Times of India. For energy-heavy portfolios, though, it was a headwind: Oil & Gas fell 1.18%.

-

The NSE IPO filing: After a decade of regulatory delays, the National Stock Exchange submitted its draft papers for what could be India’s largest-ever IPO—a pure offer-for-sale, no fresh capital raise. Major shareholders—SBI, IDBI, IFCI, HDFC Life—will offload about 6% equity. The windfall? Estimated at $2.6 billion. Stakes rose: IFCI +3%, IDBI Bank +2.8%, SBI +1.1%. But the event also spotlighted BSE, whose shares had already priced in the comparison. Analysts warned: BSE’s upside now depends on execution, not just the NSE listing.

-

US Fed’s hawkish undertone: Despite the Nasdaq’s euphoria, Fed commentary this week kept rate-cut hopes muted. Indian bond bulls ignored it, betting on local factors (crude, FTA optimism with the UK). But equity traders weren’t so forgiving—defensives outperformed cyclicals.

-

Market breadth turned mixed: The Nifty 500 saw advances and declines nearly balanced. Within the Nifty 50, 22 stocks rose, 28 fell—a classic distribution day. Yet the Midcap 100’s 0.22% gain hints that smart money was rotating, not exiting.

3. A Walk Through the Sectors

The Leaders

-

Pharma (+0.73%): The day’s champion. Lupin, Aurobindo, and Dr. Reddy’s all posted gains on no specific news—pure risk-off rotation. Pharma’s defensive appeal shone as IT cratered. The sector index closed at 24,460.30, near recent highs.

-

Defence (+0.68%): Hindustan Aeronautics (HAL), Bharat Electronics (BEL), and Mazagon Dock held steady. The thematic index rose as investors bet on multi-year order pipelines. Defence remains a story of patience—news-light, trend-strong.

-

Energy (+0.22%): NTPC, Power Grid, and Tata Power benefited from falling crude. The index closed at 40,548.10. Falling input costs = fatter margins for thermal players.

-

Media (+0.10%): A rounding error move, but notable given how beaten-down this cohort is. Zee Entertainment and Sun TV traded flat; the index at 1,515.40 remains near multi-year lows.

-

Metal (+0.08%): Barely green. Vedanta, JSW Steel, and Tata Steel saw mixed action. Citi’s bullish call on Vedanta Aluminium (Rs 560 target, 20% upside) sparked interest, but broader metal sentiment stayed tepid. The sector index closed at 13,020.80—a whisper above flatline.

The Laggards

-

IT (-3.65%): The bloodbath. TCS, Infosys, Wipro, and HCL Tech all fell 3–4%. No earnings miss, no guidance cut—just profit-booking after a strong run and a disconnect with Nasdaq’s rally. The index dropped to 27,426.85. Mid-tier names like Persistent Systems, KPIT Technologies, and Tata Elxsi fared no better. Volume was elevated—this was selling with conviction.

-

Oil & Gas (-1.18%): Reliance Industries, IOC, BPCL all slipped as Brent’s decline meant margin compression for refiners. The index settled at 11,169.75. Ironically, lower crude helps India’s macro but hurts the sector’s earnings—traders chose the latter narrative today.

-

Realty (-1.01%): DLF, Prestige Estates, Godrej Properties all sold off. Prestige’s news—halting its hospitality unit IPO to explore a PE stake sale instead—didn’t help sentiment. The sector index fell to 811.90, underperforming even as bond yields eased (which should theoretically help developers).

-

PSU Bank (-0.62%): SBI, Bank of Baroda, Canara Bank all dipped. The index closed at 8,716.50. Private Bank fared worse (-0.50%), dragging Bank Nifty down 0.48% overall.

-

Auto (-0.61%): Bajaj Auto, Maruti, Mahindra & Mahindra all retreated. Bajaj announced a Rs 5,633 crore buyback at Rs 12,000/share (record date June 24), yet the stock fell—classic “buy the rumour, sell the news.” The index closed at 26,583.35.

The Steady Middle

-

FMCG (-0.19%): Hindustan Unilever, ITC, Nestle—flat to slightly down. No drama. The index at 49,558.70.

-

MNC (+0.07%): Tiny gain. Borosil Renewables, Abbott India—niche plays, niche moves.

-

Manufacturing (-0.08%): The thematic index barely budged. Larsen & Toubro, ABB, Siemens—waiting for capex catalysts.

4. Beyond the Nifty 50 — Stories From the Broader Market

While the frontliners shuffled, the action was in the wings:

-

Bata India (+16.24%): The day’s rocket. The company named Sanjay Rao—formerly of Nike Retail—as its new MD & CEO, succeeding Gunjan Shah. The appointment signals a Gen-Z pivot, a turnaround bet. Volume spiked 12x average. RSI rocketed to 81 (extreme overbought), but momentum trumped caution. This is what a credible narrative + execution change looks like in price action.

-

HFCL (+5.12%): Telecom infrastructure play jumped after bagging a Rs 2,666 crore order from Rail Vikas Nigam (RVNL) for BharatNet Phase 3. The stock has soared 200% in six months—today’s move was the latest chapter. Volume: 2.1x average. RSI: 68 (nearing overbought but not there yet).

-

Vedanta (-0.87%): Despite Citi’s bullish note on Vedanta Aluminium (20% upside to Rs 560), the stock slipped. Metal sector weakness + profit-booking after a strong Q1. Volume was 1.3x—mild distribution, not panic.

-

IFCI (+2.91%): A pure NSE IPO beneficiary. The financial services firm holds a stake in NSE and will cash out partially. Volume: 3.4x average—this was headline-driven flow.

-

IDBI Bank (+2.76%): Another NSE shareholder. The stock rallied on windfall math: stake sale proceeds could fund balance-sheet cleanup or dividends. Volume: 2.8x.

-

Embassy REIT (+1.34%): Office real estate stayed bid despite broader realty weakness. IT sector pain didn’t dent demand for Grade-A office space—yet. Volume: 1.1x.

-

Suzlon Energy (-2.13%): Wind energy stock gave back gains. No news—just profit-taking after a stellar run. Volume: 1.6x average, RSI: 52 (neutral zone).

-

Adani Green (-1.45%): Renewable energy play slipped alongside Oil & Gas. Volume: 0.9x (below average)—light selling, no catalyst.

-

Paytm (-3.87%): Fintech name extended losses. No fresh news, but regulatory overhang persists. RSI: 34 (approaching oversold). Volume: 1.2x.

-

Zomato (-2.21%): Food delivery platform fell in sympathy with tech selloff. RSI: 47 (neutral). Volume: 1.0x—garden-variety retreat.

5. The Technical Picture

The charts whispered caution, but didn’t scream:

Overbought Names (RSI > 70)

– Bata India (RSI 81): Parabolic move on CEO news. Watch for profit-booking Monday.

– Craftsman Automation (RSI 74): Auto ancillary on a tear. Volume 15x average—something’s cooking, but sustainability is the question.

Oversold Names (RSI < 30)

– TCS (RSI 28): IT heavyweight washed out. Below both 50-DMA and 200-DMA. Volume 1.8x—this was capitulation, not distribution. Contrarian opportunity?

– Infosys (RSI 29): Similar setup. Near 52-week lows. Volume 1.9x. If you’re a value buyer, this is the zone.

Volume Spikes (≥2x average)

– Bata India (12x): Already discussed.

– IFCI (3.4x): NSE IPO flow.

– IDBI Bank (2.8x): Same.

– HFCL (2.1x): RVNL order.

Cross Signals

– No Golden Crosses reported today.

– No Death Crosses flagged in the data—despite IT’s selloff, the indices remain above critical long-term averages.

Key Levels for Monday

– Nifty 50: Support at 23,900 (today’s low), resistance at 24,168 (Thursday’s close). A break below 23,900 opens 23,750.

– Bank Nifty: Support at 57,465, resistance at 57,805. Holding the 57,500 zone is critical.

6. AI Signals — BUY / HOLD / SELL

| Stock | Signal | Reason |

|---|---|---|

| TCS | BUY | RSI 28 (oversold), volume 1.8x avg, capitulation setup near 52w lows |

| Infosys | BUY | RSI 29 (oversold), volume 1.9x, defensive IT at deep discount |

| HFCL | BUY | RSI 68, volume 2.1x, Rs 2,666cr RVNL order catalyst, above 50-DMA |

| IFCI | HOLD | RSI 61, volume 3.4x (news spike), NSE IPO windfall priced in short-term |

| IDBI Bank | HOLD | RSI 58, volume 2.8x (event-driven), wait for IPO clarity |

| Bata India | SELL | RSI 81 (extreme overbought), volume 12x, CEO news fully priced, profit-taking due |

| Vedanta | HOLD | RSI 54, volume 1.3x, Citi target bullish but metal sector weak, mixed signals |

| Embassy REIT | BUY | RSI 56, volume 1.1x, office demand resilient, above 200-DMA |

| Paytm | HOLD | RSI 34 (nearing oversold), but no catalyst, regulatory overhang persists |

| Suzlon Energy | HOLD | RSI 52, volume 1.6x, profit-taking after rally, neutral zone, await next trigger |

| Bajaj Auto | HOLD | Buyback Rs 12,000/share (Jun 24 record date), but stock down today, wait for arb clarity |

| Lupin | BUY | RSI 63, pharma rotation play, above 50-DMA, defensive strength intact |

7. Tomorrow’s Setup — Global Cues & Calendar

Monday’s open will inherit this global tape:

- US equities: Nasdaq +1.91%, S&P 500 +1.08%, Dow +0.14%. Tech led; defensives lagged. That setup usually helps Indian IT—except today it didn’t. Watch if the divergence corrects.

- Asian close: Nikkei +0.28% (mild positive), Hang Seng -1.59% (China weakness persists), ASX -0.92% (commodities soft).

- GIFT Nifty: Flat at 24,013.10 (mirroring Nifty’s close). No gap expected at open.

- Crude: Brent $79.64, WTI $75.92. If this holds, expect Energy and Oil & Gas to remain under pressure; bond bulls and importers to cheer.

- Gold: $4,175 (-1.16%). Easing geopolitical premium. Equity rotation in play globally.

- USD/INR: 94.31 (-0.58%). Rupee strength is a tailwind for importers, headwind for IT exporters (adding to today’s pain).

Key levels to watch:

– Nifty 50: 23,900 support (today’s low), 24,168 resistance (Thursday’s close). A reclaim above 24,168 signals the dip was shallow; a break below 23,900 invites 23,750.

– Bank Nifty: 57,465 support, 57,805 resistance. Eyes on how PSU and Private Banks trade post-NSE IPO noise.

– Sectoral bets: Pharma and Defence if risk-off persists. IT if global cues stay hot and rupee stabilises. Metal if China data surprises.

Domestically: Monday brings no major macro releases, so price action will be technical + news-driven. NSE IPO chatter will dominate headlines, but actual listing is months away—don’t confuse noise with signal.

8. The Honest Take

For long-term investors: Today was a reminder that even in a rally, rotation happens. The NSE IPO filing is historic—it’s India’s capital markets coming full circle. But the real opportunity isn’t in chasing IFCI or IDBI on headlines; it’s in the names that got washed out unfairly. TCS and Infosys at RSI 28–29, trading near 52-week lows despite Nasdaq’s surge, are asymmetric setups. If you believe in India’s IT services story over 3–5 years, this is value. Pharma’s defensive bid, Defence’s structural tailwind, and select midcap industrials (HFCL, Craftsman) on order flow—these are the building blocks of a patient portfolio. Ignore the Nifty’s 154-point drop. Focus on what you’re accumulating at what price.

For active traders: Friday was a gift and a trap. A gift if you sold Bata at RSI 81. A trap if you chased IT’s bounce that never came. Volume tells the truth: IFCI at 3.4x, IDBI at 2.8x, HFCL at 2.1x—these are event-driven spikes. Fade them unless fundamentals confirm. The VIX at 12.97 says complacency, not fear—that’s a setup for surprise, not trend. Watch Monday’s open: if Nifty gaps down below 23,900, cover longs and wait. If it holds and reclaims 24,050, the five-session rally resumes. Bank Nifty’s 57,465 is your line in the sand. And for stock-specific plays: Bata’s parabolic, TCS is oversold, HFCL has a fundamental catalyst. Choose your battlefield wisely.

— Unified Stocks

“The stock market is filled with individuals who know the price of everything, but the value of nothing.” — Philip Fisher