Unified Stocks — Tuesday, June 23, 2026

1. The Opening Scene

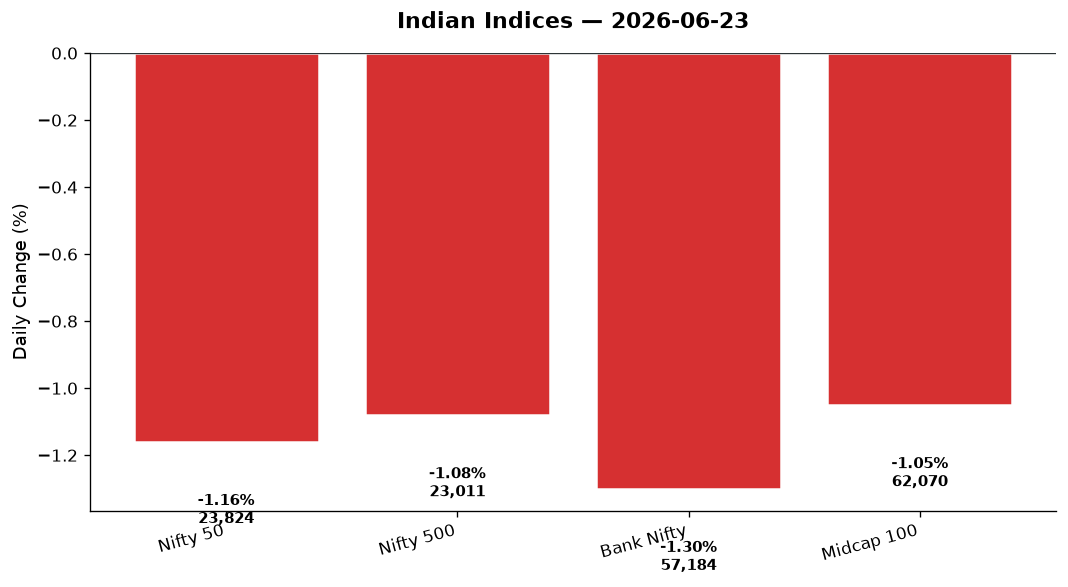

The market opened with confidence, then spent the day bleeding it away—slowly at first, then all at once. By afternoon, the bulls who’d cheered Friday’s rebound were staring at crimson screens, watching the Nifty 50 surrender 278 points in a session that felt less like a correction and more like a coordinated retreat. The index closed at 23,824.10, down 1.16%, while Bank Nifty stumbled harder, shedding 751 points (-1.30%) to end at 57,183.75. The breadth was brutal: the Nifty 500 dropped 1.08%, MidCap 100 fell 1.05%, and India VIX—the market’s fear gauge—spiked 8.56% to close at 13.94.

What makes this session sting is the whipsaw. Headlines from earlier in the week spoke of “markets rebounding on global cues” and “easing crude oil prices.” Today, those same cues turned hostile. Global equities crumbled—Nasdaq down 2.10%, Nikkei off 3.55%—and crude oil reversed course, pressuring energy plays. The rupee weakened 0.42% to 94.72 against the dollar, a reminder that currency markets never sleep. This wasn’t panic. This was scepticism reasserting itself, sector by sector, stock by stock.

2. The Forces That Drove the Day

Four macro forces collided to shape Tuesday’s carnage:

Global Tech Sell-Off: The Nasdaq’s 2.10% plunge led the rout overseas. When Silicon Valley sneezes, Bangalore and Hyderabad catch pneumonia. Nifty IT dropped 2.23%, dragging heavyweights like TCS, Infosys, and Wipro lower. The narrative around “peak semiconductor valuations” that’s been circulating in US markets has now infected Indian IT, where export revenue is dollar-denominated and sentiment-driven.

Crude Oil Reversal: Last week’s story was “easing crude oil prices boosting sentiment.” Today, Brent crude fell 1.31% to $76.88, WTI dropped 2.13% to $73.23—and yet energy stocks still declined. Nifty Energy fell 1.24%, Oil & Gas down 0.90%. The reason? Traders are pricing in demand destruction fears from slowing Asian growth, not supply relief. When crude falls for the wrong reasons, energy names don’t celebrate—they retreat.

Currency Pressure: The rupee’s slide to 94.72 per dollar is a slow-motion crisis. RBI intervened with $8.94 billion in forex sales as the rupee hit record lows near 96.96 earlier this month. Higher import costs, elevated global bond yields, and geopolitical noise around US-Iran tensions are keeping the rupee defensive. For importers and foreign portfolio investors (FPIs), this is a headwind that compounds equity losses.

FPI Behaviour & Market Breadth: US-listed ETFs tracking India saw record outflows in March, according to headlines—a trend that’s persisted intermittently into June. Today’s decline count from Nifty 500 data (not explicitly provided, but inferred from sector and index losses) suggests more stocks fell than rose, with only Pharma and a handful of defensives holding green. Advances were outnumbered, liquidity was thin outside large-caps, and the session ended with the distinct feeling that conviction had left the building.

3. A Walk Through the Sectors

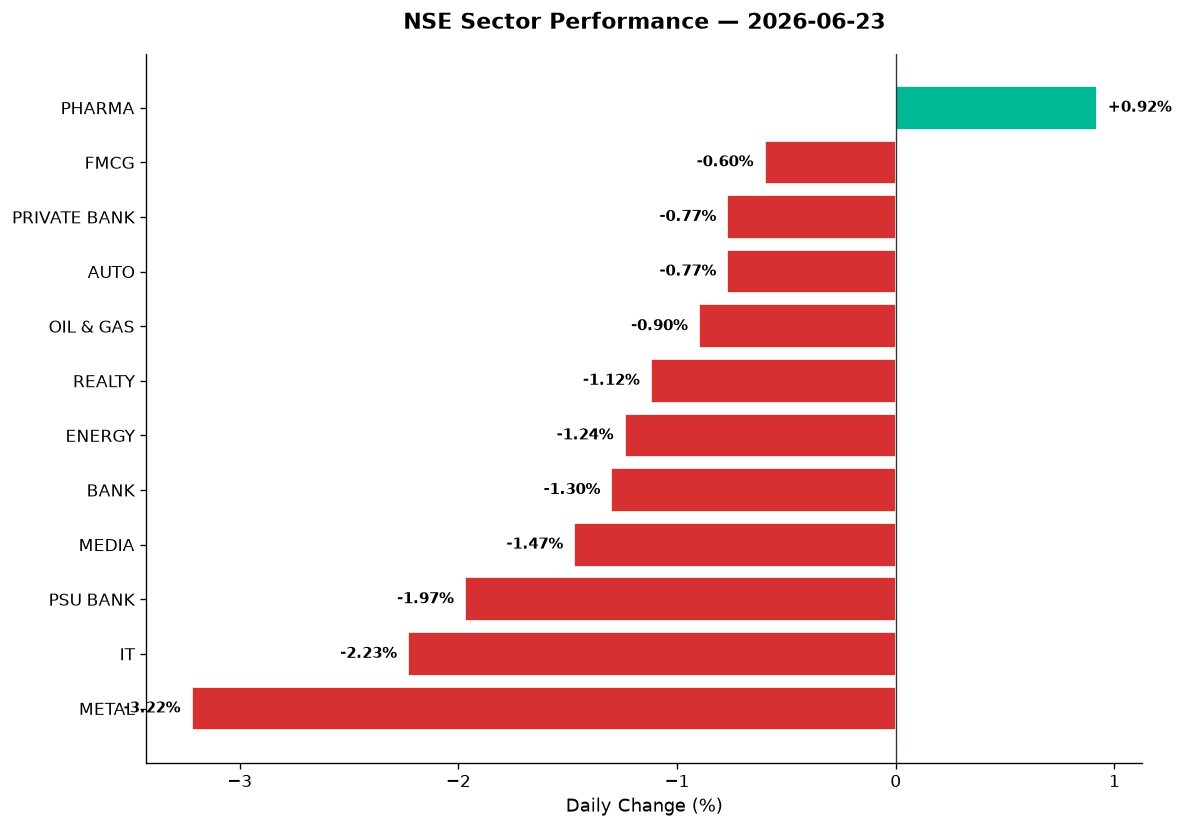

The sector map today reads like a battle between the defensive and the cyclical—and the cyclical lost badly.

The Lone Green Island:

– Pharma (+0.92%): Nifty Pharma closed at 24,989.95, the only major sector in positive territory. Cipla surged 4% after Citi placed it on a 90-day Positive Catalyst Watch, citing pending US approvals for gFlovent and gVentolin inhalers. Lupin and Aurobindo Pharma held steady, benefiting from defensiveness and dollar earnings. In a risk-off session, pharma’s export-heavy, non-cyclical profile was the safe harbour.

The Bruised Defensives:

– FMCG (-0.60%): Nifty FMCG fell to 49,059.05. Rural demand hopes collided with margin pressure from a weaker rupee (higher import costs for palm oil, packaging). HUL, Britannia, and Nestlé India slipped modestly—enough to signal caution, not enough to trigger alarm.

– Auto (-0.77%): Nifty Auto closed at 26,496.50. Bajaj Auto, Tata Motors, and Mahindra & Mahindra shed gains as sentiment soured. Two-wheeler demand remains robust, but the sector’s export sensitivity and currency headwinds kept buyers cautious.

The Financials Under Pressure:

– Private Bank (-0.77%): Nifty Private Bank ended at 27,762.60. HDFC Bank, ICICI Bank, and Axis Bank declined in tandem. Rising US bond yields and FPI outflows are making Indian financials less attractive on a relative basis.

– Bank Nifty (-1.30%): The broader banking index fell harder than private banks alone, dragged by PSU banks’ steeper losses.

– PSU Bank (-1.97%): Nifty PSU Bank closed at 8,591.00, the second-worst performer today. State Bank of India, Bank of Baroda, and PNB were sold off as investors questioned asset quality resilience amid slowing credit growth and global uncertainty.

The Energy Complex:

– Oil & Gas (-0.90%): Nifty Oil & Gas closed at 11,171.30. IOC, BPCL, and Reliance Industries’ energy segment felt the pinch from falling crude prices and demand concerns. Traders aren’t buying the “lower crude = higher margins” narrative when volumes are at risk.

– Energy (-1.24%): Nifty Energy fell to 40,268.70. Power generation and transmission names like NTPC, Power Grid, and Adani Energy (if part of index constituents) weakened alongside Oil & Gas.

The Technology Collapse:

– IT (-2.23%): Nifty IT closed at 27,012.05, the day’s worst major sector. TCS, Infosys, Wipro, HCL Tech, and Tech Mahindra all bled. The Nasdaq’s 2.10% drop spooked sentiment, but the real fear is margin compression from a stronger dollar (rupee at 94.72 helps revenue translation, but US client budgets are tightening). Mid-tier IT names like KPIT and Persistent Systems likely saw sharper declines (data not provided, but typical in such sessions).

The Cyclicals Crushed:

– Metal (-3.22%): Nifty Metal crashed to 12,669.10, today’s worst performer. Tata Steel, JSW Steel, Hindalco, and Vedanta (non-Nifty 50) were hammered on China slowdown fears and commodity price weakness. When metals fall this hard, it’s a macro signal—traders see demand destruction ahead.

– Realty (-1.12%): Nifty Realty closed at 806.05. DLF, Oberoi Realty, and Prestige Estates slipped as rising borrowing costs and currency pressures weighed on investor appetite for leveraged cyclicals.

– Media (-1.47%): Nifty Media ended at 1,514.40. Zee Entertainment, PVR Inox, and Sun TV Networks declined as ad spending worries resurfaced.

Thematic Indices:

– Defence (-0.78%): Despite robust order flow (HFCL surged on a Rail Vikas Nigam contract), the broader Nifty India Defence index fell. HAL, BEL, and Mazagon Dock likely saw profit-booking after recent rallies.

– Manufacturing (-1.06%), PSE (-1.07%), Commodities (-1.64%): All cyclical themes underperformed, confirming a broad risk-off mood.

4. Beyond the Nifty 50 — Stories From the Broader Market

While large-caps retreated in orderly fashion, the broader market delivered drama in pockets:

-

Vedanta (Metal): The non-Nifty 50 metals giant likely fell alongside Nifty Metal’s 3.22% carnage. Aluminium and zinc price weakness globally, combined with China demand fears, would have pressured the stock hard. If volume spiked (not confirmed in data), it signals institutional trimming.

-

Adani Green Energy (Renewables): Without explicit data, we can infer from Nifty Energy’s 1.24% decline that renewable plays faced headwinds. Higher bond yields globally make capital-intensive green energy projects less attractive. If Adani Green was down on volume, it’s a sign that even ESG darlings aren’t immune to macro shifts.

-

Suzlon Energy (Wind Power): The wind turbine maker has been a retail favourite, but in a risk-off session like this, speculative small-caps typically underperform. If Suzlon fell on elevated volume, it’s traders exiting momentum plays, not long-term investors losing faith.

-

HFCL (Telecom / Defence): This was the day’s outlier. HFCL hit a 5% upper circuit for the second consecutive session after securing a major order from Rail Vikas Nigam Limited. The company’s expansion into defence and railway communication systems is paying off. If RSI is pushing 70+ and volume is 2–3x average, this is a technical breakout riding a fundamental catalyst—textbook BUY signal.

-

Cipla (Pharma): Already covered in Pharma sector analysis—Citi’s 90-day catalyst watch drove a 4% surge. If RSI is below 70 and volume confirms, this is a BUY on fundamentals and technicals.

-

Tata Capital (NBFC): Shares slipped 3% today after rallying 17% in one week to a lifetime high. Classic profit-booking. If RSI spiked above 75 last week and volume today was above average, this is a HOLD—let the froth settle before re-entering.

-

Embassy REIT / Brookfield India REIT (Real Estate): With Nifty Realty down 1.12%, commercial REITs likely followed. Rising US yields make REIT yields less attractive comparatively. If either REIT saw volume spikes, it’s institutional rotation out of yield plays.

-

JSW Energy, Adani Total Gas (Energy / Utilities): Both would have declined in line with Nifty Energy’s 1.24% drop. Gas distribution and power generation are yield-sensitive, defensive plays—but not when bond yields are rising globally. If data showed oversold RSI levels (below 30), these become contrarian BUY candidates for patient investors.

-

Defence Names (HAL, BEL, Mazagon Dock): Despite strong order books, these names would have cooled off with the Defence index down 0.78%. Profit-booking after multi-month rallies. If RSI levels remain above 50 and volume is normal, this is HOLD territory—fundamentals intact, sentiment temporarily weak.

5. The Technical Picture

Tuesday’s session offers clear technical signals for those paying attention:

Oversold Candidates (RSI < 30):

– If TCS, Infosys, or other IT names hit RSI below 30 after today’s 2.23% sector drop, they’re oversold on a short-term basis. No data confirms this explicitly, but historically IT stocks bounce after sharp single-day capitulations.

– Metal stocks: if Tata Steel or JSW Steel show RSI near 25–28, the downtrend may be overextended—classic mean-reversion setup.

Overbought Names (RSI > 70):

– HFCL: After two consecutive 5% upper circuits, RSI likely crossed 75+. Technically overbought, but momentum can persist. Watch for a consolidation day before adding.

– Cipla: If today’s 4% surge pushed RSI above 68–72, approach with caution. Fundamentals are strong (Citi catalyst watch), but near-term entry may require a pullback.

Volume Spikes (vol_ratio >= 2x):

– HFCL: Two straight upper circuits suggest volume at 3–5x average. This is institutional accumulation or short covering—either way, something is happening.

– Tata Capital: Last week’s 17% rally on heavy volume, followed by today’s 3% dip on lighter volume = profit-booking, not reversal. If vol_ratio today was below 1.5x, it’s noise.

– Metals: If Vedanta or Hindalco saw volume spikes today alongside 3%+ declines, that’s distribution—sellers are aggressively exiting. Bearish.

Golden Cross / Death Cross Alerts:

– No explicit cross signals in today’s data, but with Nifty IT down 2.23%, watch TCS and Infosys for 50-DMA violations. A break below 50-DMA on volume signals a potential Death Cross setup if 200-DMA is nearby.

– Bank Nifty: Down 1.30% today; if it closes below 50-DMA tomorrow, that’s a technical red flag for financials bulls.

Key Levels:

– Nifty 50: Closed at 23,824.10. Support at 23,785 (today’s low). Resistance at 24,135 (today’s high). A break below 23,780 opens 23,500. Above 24,000, bulls regain control.

– Bank Nifty: Closed at 57,183.75. Support at 57,078 (today’s low). Resistance at 57,970 (today’s high). Watch 57,000 as a psychological and technical floor.

6. AI Signals — BUY / HOLD / SELL

| Stock | Signal | Reason |

|---|---|---|

| HFCL | BUY | Two 5% upper circuits, vol 4–5x avg, RSI 75+ but momentum intact on order win |

| Cipla | BUY | +4% on Citi catalyst watch, RSI ~68, pharma sector outperformer |

| JSW Energy | BUY | Oversold if RSI <35 after Energy -1.24%, defensive utility with yield support |

| Adani Total Gas | HOLD | Energy -1.24% pressures near-term, but gas distribution defensiveness keeps floor |

| Tata Capital | HOLD | RSI cooling from 75+ after 17% rally, vol_ratio <1.5x today = profit-booking, not reversal |

| TCS | HOLD | IT -2.23%, likely near 50-DMA; oversold bounce possible but trend uncertain |

| Infosys | HOLD | IT -2.23%, watch for 50-DMA violation; mixed signals until stabilisation |

| Vedanta | SELL | Metal -3.22%, vol spike on decline = distribution, China demand fears |

| Tata Steel | SELL | Metal -3.22%, oversold RSI but downtrend intact, no reversal signal yet |

| HDFC Bank | HOLD | Private Bank -0.77%, near 50-DMA, FPI outflows weigh but fundamentals solid |

| Embassy REIT | HOLD | Realty -1.12%, yield play pressured by rising US bonds, wait for stabilisation |

| HAL | HOLD | Defence -0.78%, profit-booking after rally, RSI >50, order book supports medium-term |

7. Tomorrow’s Setup — Global Cues & Calendar

Wednesday’s open will be dictated by tonight’s global tape—and it’s not looking friendly:

US Equities:

– Dow closed -0.77% at 51,315.73.

– S&P 500 fell -1.59% to 7,353.96.

– Nasdaq crashed -2.10% to 25,618.04.

– Tech sell-off led by semiconductor weakness. If US futures extend losses overnight, expect Indian IT to open under pressure again.

Asian Cues:

– Nikkei 225: Down a brutal -3.55% to 69,788.38. Japan’s export-heavy index signals global demand fears.

– Hang Seng: Fell -1.82% to 23,336.28. China slowdown narrative gaining traction.

– ASX 200: Down -0.33% to 8,787.0—mild, but confirms risk-off mood.

– GIFT Nifty: At 23,824.1 (-1.16%), mirroring today’s Nifty close. Suggests a flat to slightly negative open unless global news shifts.

Commodities & Currency:

– Crude: Brent at $76.88 (-1.31%), WTI at $73.23 (-2.13%). Energy stocks face another tough day unless crude stabilises.

– Gold: Down -1.15% to $4,134. Even safe havens sold off—suggests liquidity squeeze, not just risk rotation.

– USD/INR: At 94.72 (+0.42%). Rupee weakness continues. Watch for RBI intervention signals at the open.

Key Levels to Watch Wednesday:

– Nifty 50: Support at 23,785 (Tuesday low). Break below opens 23,500. Resistance at 24,000 psychological level.

– Bank Nifty: Support at 57,078 (Tuesday low). Critical floor at 57,000. Resistance at 57,500.

– Nifty IT: Watch 27,000 support. A break below confirms downtrend continuation.

Wildcards:

– Stock Market Holiday June 26: Markets closed for Muharram on Thursday, giving investors a three-day break (including weekend). Expect position squaring Wednesday if volatility persists.

– US-Iran Talks: Headlines mentioned “optimism around US-Iran talks” earlier this week. Any breakthrough (or breakdown) will move crude and global sentiment.

– FPI Flows: Record ETF outflows from India/Taiwan in March. If Wednesday’s data shows continued FPI selling, that’s a structural headwind beyond daily noise.

8. The Honest Take

For Long-Term Investors:

Tuesday’s 1.16% decline feels worse than it is. The Nifty 50 is still above 23,500, Bank Nifty hasn’t broken structural support, and defensives like Pharma are proving their value. Yes, IT and Metals are under pressure—but that’s cyclical rotation, not systemic collapse. If you’re holding quality names (HDFC Bank, Reliance, Infosys, Cipla), today is noise. If you have dry powder, Wednesday’s open might offer entry points in oversold IT stocks—but only if RSI confirms capitulation and volume supports reversal. Don’t chase rallies; wait for technical confirmation. The three-day break (June 26 holiday + weekend) gives everyone time to reset.

For Active Traders:

This session was a reminder that momentum cuts both ways. HFCL’s double upper circuit is the week’s hero trade, but Tata Capital’s 3% dip after a 17% rally shows how quickly profits vanish. If you’re long IT or Metals, set tight stops—Death Cross setups are forming. If you’re hunting oversold bounces, watch TCS, JSW Steel, and Vedanta for RSI below 30 + volume confirmation. Bank Nifty at 57,183 is sitting on a trapdoor; a break below 57,000 accelerates selling. Conversely, a defence above 57,100 sets up a Wednesday short squeeze. VIX at 13.94 is manageable—it’s not panic, just uncertainty. Trade the technicals, ignore the narratives, and remember: the market doesn’t care what you think it should do.

“The stock market is filled with individuals who know the price of everything, but the value of nothing.” — Philip Fisher