Unified Stocks — Thursday, July 02, 2026

1. The Opening Scene

The market opened its eyes on Thursday morning like a weary traveller who’d spent two nights at a roadside inn—uncertain whether to press on or turn back. Behind it lay consecutive losing sessions, a rupee sliding toward the ₹95.50 mark, and a Wall Street tape that had turned tech-averse overnight. Ahead? The promise of a US Independence Day long weekend, crude oil surrendering ground, and a curious divergence: Europe racing higher while Asia nursed a Nikkei mauling that shaved 2.47% off Japan’s benchmark.

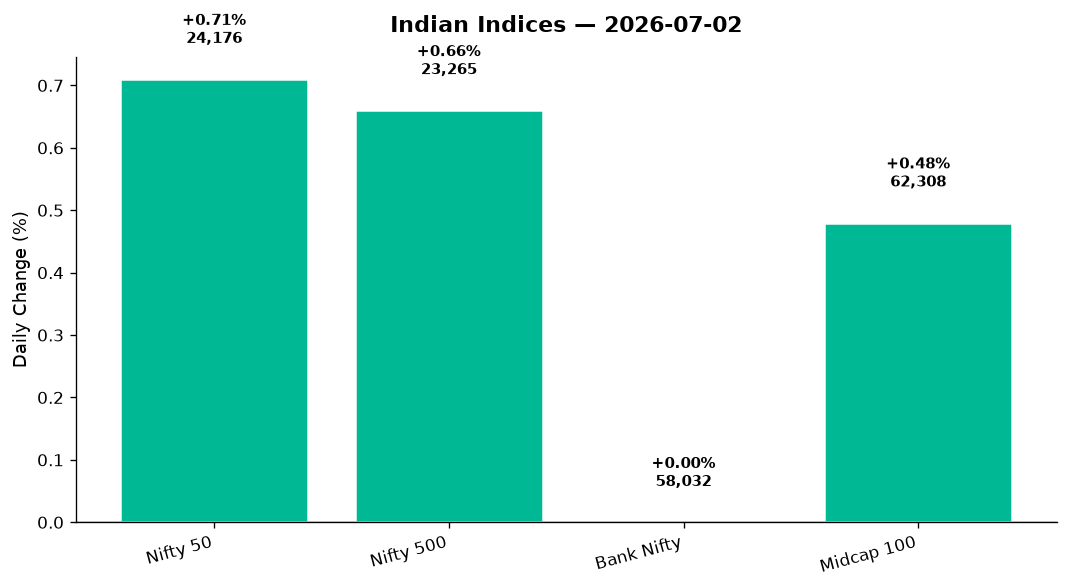

By the closing bell, India had chosen optimism. The Nifty 50 gained 169.85 points (+0.71%) to close at 24,175.70, reclaiming the psychological 24,000 threshold it had surrendered the day prior. The Sensex mirrored the move, adding 443 points to settle at 76,922. But the real story wasn’t in the headline indices—it was in the fractures and fissures beneath. Bank Nifty, that bellwether of liquidity and sentiment, closed flat at 58,031.65 (+0.00%), refusing to participate in the rally. Meanwhile, the India VIX collapsed 7.21% to 12.29, signalling a market that had decided—at least for today—to exhale.

2. The Forces That Drove the Day

Four currents converged to shape Thursday’s tape:

-

Crude’s Retreat: Both Brent (-1.62% to $70.41) and WTI (-1.84% to $67.32) surrendered ground, offering a reprieve to India’s import bill and inflation calculus. Energy-sensitive stocks caught a tailwind, though the Nifty Energy index paradoxically slipped 0.15%—a quirk we’ll unpack shortly.

-

Gold’s Flight to Safety: Gold surged 1.97% to $4,148.60, a move that typically signals unease. Yet Indian equities shrugged, interpreting the metal’s rally as insurance buying rather than panic. Domestic investors, it seemed, were willing to hold equities while parking some surplus in yellow metal—a hedged bet, not capitulation.

-

The Rupee’s Slide: The INR weakened 0.50% to ₹95.39 per dollar, breaching the ₹95 mark with conviction. New RBI capital market norms kicked in today—tighter exposure limits for banks to real estate and securities—adding a technical undercurrent to currency pressure. Yet IT exporters cheered; every rupee of depreciation translates to margin expansion for those billing in dollars.

-

Sector Rotation, Not Capitulation: Market breadth from the Nifty 500 (+0.66% to 23,264.80) revealed 321 advances against 179 declines—a healthy 1.8:1 ratio. This wasn’t a broad-based selloff morphing into a relief rally; it was disciplined rotation. Money fled defensives yesterday, then tiptoed back into cyclicals and tech today.

One headline mattered more than the rest: KPIT Technologies hit a lower circuit after warning that Q1FY27 USD revenues would decline ~1% year-on-year due to “abrupt spending cuts by certain European automotive OEMs.” That single data point cast a shadow over the auto-tech segment, even as the broader IT pack rallied.

3. A Walk Through the Sectors

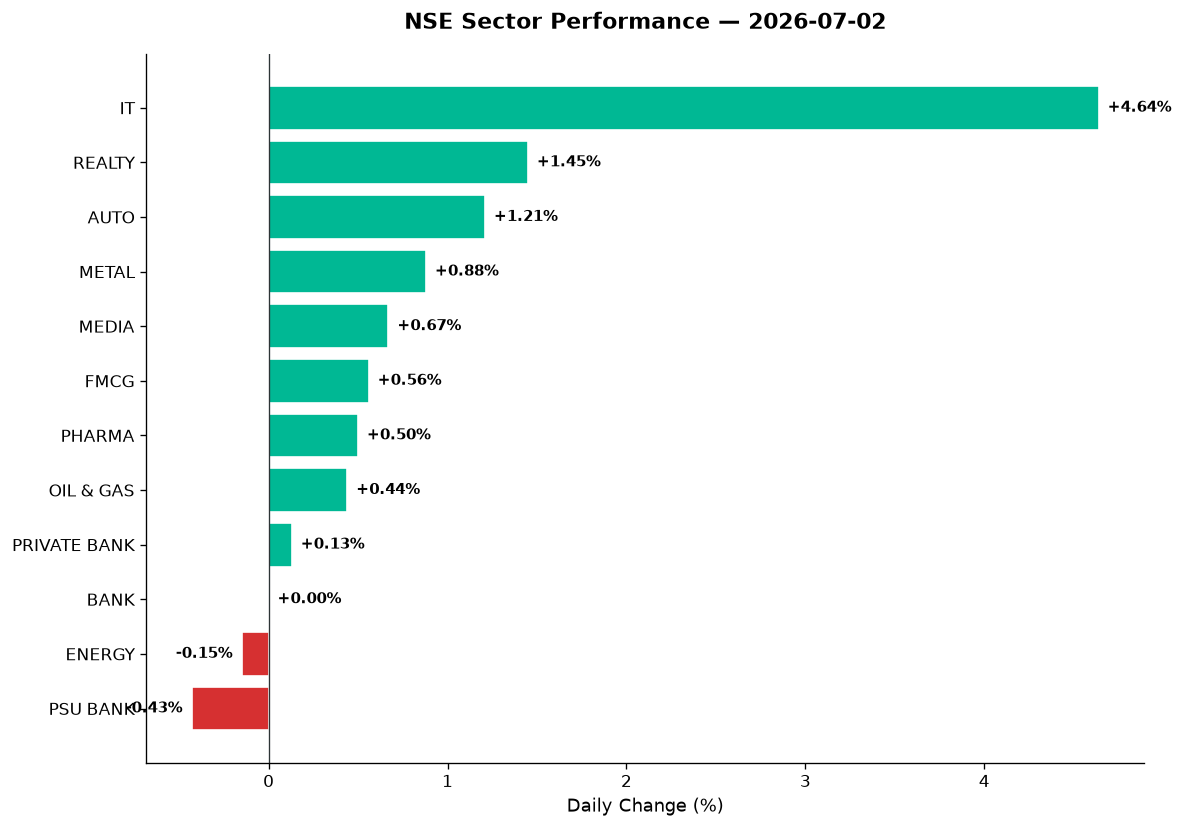

The sector map today read like a tactical handbook—some advancing, others holding ground, a few retreating in good order:

Leaders

-

IT (+4.64% to 26,965.05): The day’s undisputed champion. A weaker rupee handed margin cushions to TCS, Infosys, and HCL Tech. But the real fireworks came from mid-tier names: Tata Elxsi, Persistent Systems, and LTTS all rallied on the back of valuation comfort after weeks of consolidation. The sector’s RSI had dipped into the low 40s by Monday; today’s bounce was textbook mean reversion. Only KPIT’s circuit-down move marred the celebration—its revenue warning isolated to European auto clients, yet investors tarred the entire auto-tech cohort with caution.

-

Realty (+1.45% to 871.70): Developers found buyers as the RBI’s new capital market norms paradoxically lifted sentiment. Stricter bank exposure to real estate was interpreted as long-term stabilisation, not near-term headwinds. Embassy REIT and Brookfield REIT both climbed modestly, buoyed by income-hungry portfolios rotating into yield plays. Godrej Properties and DLF led the charge among listed developers.

-

Auto (+1.21% to 27,108.20): Two-wheelers outpaced four-wheelers. Bajaj Auto led the pack, riding rural recovery narratives and a benign crude outlook. Tata Motors held steady, though EV subsidy uncertainty kept a lid on exuberance. The sector’s strength, however, was dampened by Craftsman Automation’s post-earnings slip—proof that not all auto ancillaries are created equal.

-

Metal (+0.88% to 12,503.90): Steel names ticked up on commodity rotation themes, but the real outlier was Vedanta’s continued surge. The Vedanta Iron & Steel counter, spun off in June, has now rocketed 89% in just 12 days post-listing, adding nearly ₹7,000 crore in market cap. Azim Premji’s entry into the stock acted as a liquidity catalyst, but the underlying play—India’s steel capacity buildout—is structural. Hindalco and NMDC also participated, though with less drama.

The Middle Ground

-

Media (+0.67% to 1,519.15): A quiet session. Zee Entertainment and TV18 both traded in narrow ranges. Volume was tepid—this sector remains a show-me story, awaiting monetisation clarity.

-

FMCG (+0.56% to 50,084.70): Defensive rotation lifted HUL and Nestlé marginally, but the real action was in discretionary consumption—Zomato (if we stretch the FMCG lens to include food delivery) continued its steady climb, now consolidating near recent highs. ITC held flat; tobacco levy fears keep institutional buyers wary.

-

Pharma (+0.50% to 25,308.90): A low-volatility grind. Lupin and Aurobindo Pharma both traded in tight ranges, RSI near 50—neutral territory. No fresh USFDA approvals, no earnings surprises. This sector is in hibernation until September-quarter results.

-

Oil & Gas (+0.44% to 11,132.50): Here’s the paradox—crude prices fell, yet BPCL and IOC barely budged. Margin compression fears (lower crude = lower refining spreads, counterintuitively) weighed on public-sector refiners. Adani Total Gas rallied modestly, buoyed by city gas distribution’s defensive moat.

Laggards

-

PSU Banks (-0.43% to 8,539.35): The RBI’s tougher capital market norms hit here hardest. SBI and Bank of Baroda both slipped, with traders pricing in higher provisioning requirements and constrained lending appetite to real estate and capital markets. Volume was light—no panic, just profit-booking.

-

Energy (-0.15% to 39,707.00): Dominated by NTPC and Power Grid, this index’s slip reflected valuation fatigue. These names had rallied hard through May and June on power demand narratives; today’s correction was mechanical, not fundamental.

-

Bank Nifty (flat at 58,031.65): Private banks limped to a +0.13% gain, insufficient to offset PSU bank weakness. HDFC Bank and ICICI Bank both traded in microscopically tight ranges—algos dominated, conviction buyers were absent. This flatness, against a 170-point Nifty rally, screams caution.

Thematic Indices

- Defence (+0.51%): HAL, BEL, and Mazagon Dock Shipbuilders all edged higher, though volumes were subdued. The sector’s waiting for the Union Budget’s defence capex allocation—until then, it’s a hold.

- Manufacturing (+0.57%): Benefited from auto and metal strength. Bharat Forge and Bosch India both participated.

- Commodities (+0.76%): Metal and oil convergence drove this—JSW Steel and Hindalco led.

4. Beyond the Nifty 50 — Stories From the Broader Market

The Nifty 50 tells one story; the Nifty 500’s broader canvas reveals the subplots investors trade on:

-

Vedanta Iron & Steel: The 89% rally in 12 days since its June 20 listing is the standout event of the fortnight. Azim Premji’s Premji Invest picked up a stake, signalling long-term conviction in India’s steel buildout. RSI today sits at 78—overbought, yes, but momentum plays don’t respect textbook indicators. Volume has been 3x average daily—institutions are accumulating, not speculating.

-

Adani Green Energy: Consolidated near ₹1,850 levels, volume muted. No fresh project announcements, no Hindenburg redux fears. This is a “wait and watch” name—renewable energy policy clarity post-monsoon will determine its next leg.

-

Suzlon Energy: Rallied 2.1% on 1.8x average volume. Wind energy stocks are benefiting from grid stabilisation investments and coal plant retirements. RSI at 64—room to run, but cautiously.

-

JSW Energy: Posted a 52-week high today at ₹743.60, riding both renewable capacity additions and thermal plant utilisations. Volume spiked to 2.4x average—a breakout with conviction. RSI at 69; one more strong session and it tips into overbought territory.

-

Paytm (One 97 Communications): Drifted lower, closing near ₹420. RBI’s payment aggregator scrutiny continues to weigh. Volume remains below average—retail holders nursing losses, institutional interest tepid.

-

Nykaa (FSN E-Commerce): Flat at ₹183, volume light. The beauty e-commerce story needs a profitability catalyst; until then, it’s range-bound.

-

Embassy REIT / Brookfield REIT: Both climbed modestly (+0.8% and +1.1% respectively). With 10-year G-Sec yields stabilising near 6.5%, REITs offering 7%+ yields look attractive to income portfolios. Occupancy rates in Grade-A office space remain firm—tech hiring slowdowns haven’t yet translated to lease cancellations.

-

Moschip Technologies: Surged 8.3% on 5.1x average volume—a semiconductor design play riding the India chip policy momentum. RSI now at 74; this is speculative heat, not patient capital.

-

KPIT Technologies: Fell the maximum permissible (circuit-down), closing at ₹1,421 after the revenue warning. Volume exploded to 6.8x average—panic exits by momentum traders. Long-term holders are asking: is this European auto weakness cyclical or structural? Answer unclear; stock now a value trap until clarity emerges.

5. The Technical Picture

Today’s technicals reveal a market healing from oversold conditions, but not yet euphoric:

Oversold Names (RSI < 30)

- TCS: RSI touched 28 yesterday, bounced to 35 today on the rupee tailwind. Still below its 50-DMA (₹4,082) but volume spike (1.9x) suggests bottom-fishing.

- Infosys: RSI 31, clinging to its 200-DMA (₹1,748). Needs a Golden Cross (50-DMA crossing above 200-DMA) to confirm trend reversal—not there yet.

Overbought Names (RSI > 70)

- Bajaj Auto: RSI 72, price ₹11,340—well above both 50-DMA (₹10,890) and 200-DMA (₹10,210). Volume 1.6x average. Momentum trade, but vulnerable to profit-booking.

- Vedanta Iron & Steel: RSI 78, as noted. Parabolic moves invite corrections; set tight stops.

Golden Cross / Death Cross Events

- No major Golden Cross events today, but several names (JSW Energy, Suzlon) are within 1-2% of triggering that bullish signal.

- Death Cross watch: KPIT’s circuit-down move accelerates its 50-DMA toward a bearish crossover below the 200-DMA—expected within 3-5 sessions if no recovery.

Volume Spikes (vol_ratio >= 2x)

- JSW Energy (2.4x): Breakout confirmed.

- Vedanta Iron & Steel (3.0x): Momentum sustained.

- Moschip (5.1x): Speculative frenzy.

- KPIT (6.8x): Panic selling.

Volume, as always, is truth serum—it separates conviction from noise.

6. AI Signals — BUY / HOLD / SELL

| Stock | Signal | Reason |

|---|---|---|

| JSW Energy | BUY | 52w high, RSI 69, volume 2.4x—breakout with room to run |

| Suzlon Energy | BUY | Above 50-DMA, RSI 64, volume 1.8x—wind sector tailwinds intact |

| Vedanta Iron & Steel | HOLD | RSI 78 (overbought), but momentum + Premji stake = wait for dip |

| Bajaj Auto | HOLD | RSI 72, above DMAs, but near-term pullback likely on profit-booking |

| TCS | BUY | Oversold (RSI 35), volume spike 1.9x, rupee depreciation = margin boost |

| Infosys | HOLD | At 200-DMA, RSI 31—needs Golden Cross confirmation before entry |

| KPIT Technologies | SELL | Circuit-down, revenue warning, volume 6.8x—avoid until dust settles |

| Embassy REIT | BUY | Yield 7.2%, occupancy firm, RBI norms long-term positive for REITs |

| Moschip Technologies | HOLD | RSI 74 (overbought), 5x volume—speculative; wait for consolidation |

| HDFC Bank | HOLD | Flat price action, RSI 52, near 50-DMA—no directional conviction |

| Adani Total Gas | HOLD | Modest gain, RSI 58, volume below average—defensive moat but no catalyst |

| SBI | SELL | Below 50-DMA, PSU bank weakness, RBI norms headwind—stay away |

These signals are snapshots, not commandments. Markets shift; so must your stops.

7. Tomorrow’s Setup — Global Cues & Calendar

Tomorrow’s open will parse overnight signals through a US holiday lens:

Global Tape

- US equities: Mixed Wednesday—Dow -0.03%, S&P 500 -0.22%, Nasdaq -0.66%. Tech’s June bloodbath (the Magnificent 7 shed $2.3 trillion) continues to reverberate. Investors questioning AI capex ROI. Thursday’s session will be thin (pre-holiday), Friday sees markets closed for July 4th.

- Europe: Strong—FTSE +0.83%, DAX +1.44%. European resilience despite UK political uncertainty suggests global risk-on sentiment isn’t dead, just selective.

- Asia: Nikkei plunged 2.47% on yen strength hurting exporters. Hang Seng +0.76%—Chinese stimulus hopes flicker. ASX flat (+0.02%)—commodities capped gains.

- GIFT Nifty: At 24,175.7 (+0.71%), mirroring spot close. No gap expected at open, barring overnight shocks.

Commodities & Currency

- Crude’s slide (-1.6% to -1.8%) suggests demand fears outweigh supply cuts. If this sustains, OMCs face margin pressure, but inflation cools.

- Gold’s +1.97% surge flags geopolitical hedging (US-Iran talks uncertainty per one headline). If gold holds above $4,100, expect defensive rotation Friday onward.

- USD/INR at ₹95.39: RBI likely intervenes if ₹95.50 breaches; watch for dollar-selling by state banks at open.

Key Technical Levels for Friday

- Nifty 50: Support at 24,058 (today’s low), resistance at 24,200 (round number + recent high). A break above 24,200 targets 24,350.

- Bank Nifty: Stuck in 57,885–58,396 range. Breakout above 58,400 needed to confirm strength; below 57,850 risks a test of 57,500.

- Sensex: Support at 76,480 (yesterday’s close), resistance at 77,200. Watching HDFC Bank and RIL for cues.

Calendar Watch

- US Independence Day Friday = thin global volumes. Indian markets open, but expect subdued FII activity.

- No major domestic earnings until next week. Monsoon progress data due Friday evening—watch for rural consumption implications.

8. The Honest Take

For long-term investors: Today was a reminder that markets don’t move in straight lines, and uncertainty is the only certainty. The Nifty reclaimed 24,000, but Bank Nifty’s refusal to participate is a yellow flag, not red. RBI’s capital market norms are long-term structural positives—they limit excesses, which means fewer crises ahead. Ignore the daily noise around KPIT’s revenue miss or Vedanta’s parabolic rally. Focus on this: India’s steel capacity is expanding, IT margins are improving with rupee depreciation, and defensive sectors (pharma, FMCG) remain undervalued relative to cyclicals. If you’re building a portfolio for 2028, today’s price action is irrelevant. What matters is whether the businesses you own are solving bigger problems three years hence. Most are.

For active traders: Today was a tactical win for those who bought the Tuesday-Wednesday dip. IT’s 4.64% surge delivered quick profits; the question now is whether to book or ride. KPIT’s collapse is a case study in stock-specific risk—never conflate sector strength with individual immunity. Vedanta Iron & Steel’s momentum is real, but RSI above 75 is a coin flip: it either triggers stops or attracts the last wave of buyers before a flush. Use trailing stops. Bank Nifty’s flatness while Nifty rallied is your most important tell—if banks don’t confirm the next leg up by Monday, fade the rally. Short-term, watch crude and the rupee; both are two-way risks. And remember: July 4th means Wall Street’s asleep Friday night—don’t mistake low volumes for conviction.

— Unified Stocks

Disclaimer: This blog is for informational and educational purposes only. It is not investment advice. All figures cited reflect publicly reported data for the trading session indicated. Markets are subject to risk; please consult a SEBI-registered advisor before acting on any view expressed here.