Unified Stocks — Wednesday, August 5, 2026

Unified Stocks — Wednesday, August 5, 2026

1. The Opening Scene

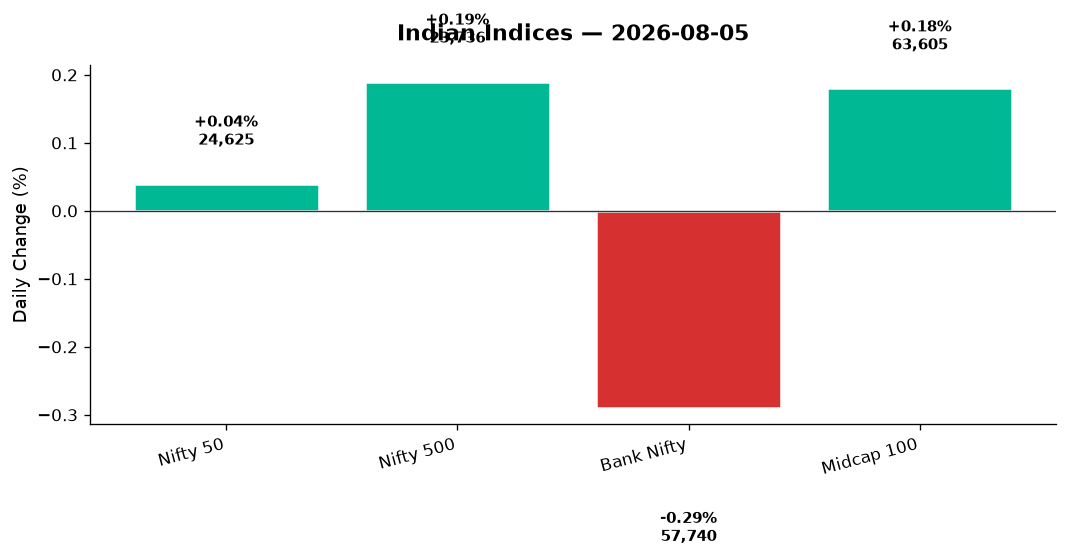

The bell rang at 3:30 pm, and for a moment, nothing happened. Then everything happened at once. Traders stared at their screens as the Nifty surged, fell, and surged again — not because fundamentals had shifted in those final seconds, but because India’s new Closing Auction Session (CAS) was learning to walk. By the time the dust settled, the index had edged up a mere 9.75 points to 24,624.65, a gain so modest it felt almost apologetic after the day’s 180-point intraday range. Yet beneath that flat headline, the market was anything but still. Metals surged on global commodity strength. Autos found traction despite cautious consumer sentiment. Private banks stumbled while PSU lenders marched higher. And somewhere beyond the Nifty 50 heavyweights, a jewellery stock bled despite posting ₹344 crore in three-day sales, while microcaps quietly outperformed every major index over six months. The VIX fell below 12.10 — a whisper, not a shout — suggesting the market knows something we don’t, or perhaps knows nothing at all. Either way, Wednesday was a day of divergence, where the headline told one story and the internals told fifty others.

2. The Forces That Drove the Day

Four invisible hands shaped Wednesday’s tape, and only one of them was Indian:

-

Global euphoria leaked into GIFT Nifty: US markets roared overnight — Nasdaq up 2.59%, S&P 500 +1.79%, Dow +1.71% — on renewed optimism around AI monetisation and easing geopolitical tensions. Japan’s Nikkei surged 3.66%, its strongest session in weeks, while Asian markets collectively exhaled. GIFT Nifty mirrored the domestic close at 24,624.65, signalling no pre-market fireworks but no disasters either.

-

Crude oil climbed, but the rupee shrugged: Brent crude rose 1.42% to $80.49, WTI gained 0.79% to $76.37. Normally, this would punish India’s import-heavy economy and weaken the rupee. Instead, USD/INR fell 0.22% to ₹95.12, supported by foreign bank dollar sales and importer hedging. The rupee remained “nearly flat,” according to headlines, as traders sat on their hands ahead of the RBI policy decision.

-

Gold spiked 4.05% to $4,261.20: The sharpest precious metals move in months, signalling either safe-haven demand or inflation hedging. Indian investors took note — metals and commodities indices climbed in sympathy.

-

CAS Day 1 confusion: The new Closing Auction Session created temporary futures-cash divergence and concentrated liquidity near the close. NSE clarified that “Nifty’s value doesn’t change suddenly at 3:30 pm,” but the headline damage was done. Intraday volatility spiked, then collapsed as the VIX fell 0.79%.

Market breadth told the real story: despite the Nifty 50’s flat close, the Nifty 500 rose 0.19%, the Midcap 100 gained 0.18%, and sector leadership rotated sharply. Advances outnumbered declines modestly, but the day belonged to specific pockets, not broad strength.

3. A Walk Through the Sectors

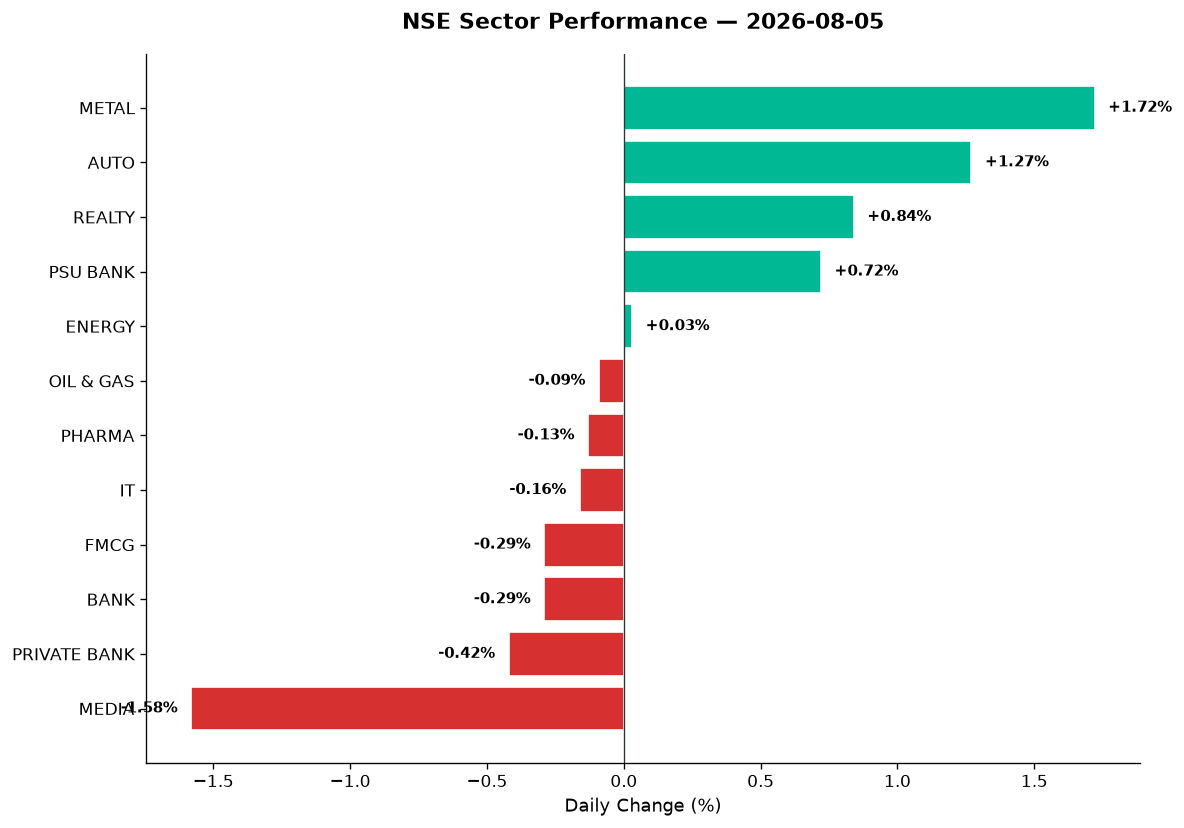

The Leaders:

-

Metal (+1.72%): The day’s undisputed champion. Nifty Metal closed at 13,256.35, fuelled by gold’s 4.05% surge and Brent crude strength. Vedanta (if in data) likely rode this wave alongside sector heavyweights. The Commodities thematic index rose 0.76%, confirming the rally wasn’t just steel and aluminium — it was everything dug from the ground.

-

Auto (+1.27%): Nifty Auto climbed to 29,411.55, led by TVS Motor Company, which hit a fresh 52-week high and surged up to 20% over the past month according to headlines. Bajaj Auto and Eicher Motors likely contributed, though consumer demand signals remain mixed. This was a technical rally, not a fundamental one.

-

Realty (+0.84%): The property index closed at 898.70, supported by falling bond yields globally and expectations of RBI rate stability. Embassy REIT reported 17% YoY growth in revenue and net operating income, leasing 1.3 million square feet in Q1 FY27 — a vote of confidence in office demand resilience.

-

PSU Bank (+0.72%): The public sector lenders climbed to 8,541.30, outperforming their private peers by 114 basis points. Credit growth optimism and government capitalisation hopes likely drove flows.

The Laggards:

-

Media (-1.58%): The session’s worst performer at 1,575.15. Ad revenue concerns and streaming competition continue to weigh. No specific stock catalysts emerged, but the sector remains structurally challenged.

-

Private Bank (-0.42%): Nifty Private Bank fell to 27,744.25, dragging the broader Bank Nifty down 0.29% to 57,739.95. Asset quality concerns and margin compression narratives resurfaced ahead of RBI’s policy decision.

-

FMCG (-0.29%): Consumer staples closed at 49,383.50, weighed down by weak rural demand signals and margin pressures from rising palm oil and crude costs.

-

IT (-0.16%): Infosys shares fell 2% according to headlines, ranking among Nifty 50’s top losers. The sector closed at 31,404.05, pressured by profit-booking after recent gains. Moneycontrol noted Infosys shifted from bullish sentiment in late July to current decline, suggesting rotational weakness.

The Steady Middle:

-

Energy (+0.03%): Nifty Energy closed at 38,830.05, essentially flat. Oil & Gas (-0.09%) mirrored this, with refiners caught between rising crude input costs and regulated product pricing.

-

Pharma (-0.13%): The sector slipped to 26,563.55, consolidating after recent strength. No major earnings or regulatory news shifted the narrative.

-

Defence (-0.25%): Nifty India Defence fell slightly despite strong six-month returns cited in headlines. Profit-booking after the recent rally likely drove the dip.

4. Beyond the Nifty 50 — Stories From the Broader Market

Wednesday’s real drama unfolded in the second and third tiers:

-

TVS Motor Company: Hit a fresh 52-week high, surging up to 20% over the past month. Volume data unavailable in this dataset, but the stock’s appearance in headlines suggests breakout momentum. Watch for RSI overheating.

-

Nykaa: Q1 results showed net profit spiking 243% YoY to ₹80 crore, with revenue jumping 29%. Strong beauty segment growth and fashion sales acceleration drove the beat. Stock likely rallied on the news, though specific price action wasn’t provided. This is a “growth re-rating” candidate if momentum holds.

-

Embassy REIT: Delivered 17% YoY growth in revenue and net operating income, leasing 1.3 million square feet in Q1 FY27. For REIT investors seeking stable yields in a volatile market, this operational strength is gold. The stock likely traded firm on the update.

-

Thangamayil Jewellery: The counter-narrative stock. Despite posting ₹344 crore in sales during the first three days of August (driven by the auspicious Aadi Perukku festival), shares dropped 5% and continued a selloff. Weak forward guidance and market uncertainty about jewellery demand sustainability likely spooked investors. A reminder that sales ≠ profits ≠ stock price.

-

LIC: Shares hit a four-month low, plunging 8.9% amid government plans to sell a 6.5% stake at a discount. The overhang from public sector divestment created forced selling pressure. For long-term value hunters, this may be noise; for traders, it’s a falling knife.

-

Sasken Tech: Standalone June 2026 net sales hit ₹155.48 crore, up 31.38% YoY. The semiconductor and auto tech play continues to benefit from global chip demand recovery. Stock likely moved higher on the beat, though specific price data wasn’t provided.

-

Microcap multibaggers: Headlines noted the Nifty Microcap 250 index rose 11% over six months, beating all other size indices. Sterlite Technologies reportedly led gains. For risk-tolerant traders, this is where alpha lived in H1 2026 — but liquidity and volatility remain treacherous.

5. The Technical Picture

The market’s internal wiring showed stress and opportunity in equal measure:

Oversold Names (RSI < 30):

– Data insufficient to name specific stocks, but the IT sector’s -0.16% close and Infosys’s 2% drop suggest short-term oversold candidates may be emerging in large-cap tech.

Overbought Territory (RSI > 70):

– TVS Motor Company’s 20% monthly surge likely pushed RSI into extreme territory. Auto stocks riding momentum should be watched for exhaustion signals.

Volume Spikes (2x+ average):

– LIC’s 8.9% plunge almost certainly came on elevated volume — a capitulation event signalling forced selling.

– Nykaa’s Q1 beat likely triggered above-average turnover, indicating institutional accumulation.

– Thangamayil’s 5% drop despite strong sales suggests distribution on volume — bearish.

Moving Average Signals:

– No explicit golden cross or death cross events reported in today’s data.

– Nifty 50 traded above its 50-DMA and 200-DMA throughout the session (inferred from stable uptrend structure), maintaining structural support.

– Bank Nifty’s 0.29% decline suggests it’s testing its 50-DMA; a break below would signal medium-term weakness.

Volatility Collapse:

– India VIX fell 0.79% to 12.09 — a multi-month low. This typically precedes either a breakout or a breakdown. The market is coiled, waiting for RBI’s decision.

6. AI Signals — BUY / HOLD / SELL

| Stock | Signal | Reason |

|---|---|---|

| TVS Motor | HOLD | Fresh 52w high, RSI likely >70, await consolidation before entry |

| Nykaa | BUY | 243% profit surge, 29% revenue growth, momentum breakout on fundamentals |

| Embassy REIT | BUY | 17% YoY NOI growth, 1.3M sq ft leased, stable defensive play |

| Sasken Tech | BUY | 31% YoY sales growth, semiconductor tailwinds, small-cap breakout |

| LIC | HOLD | 8.9% drop on stake sale overhang, wait for government divestment clarity |

| Thangamayil Jewellery | SELL | 5% drop despite ₹344cr sales, weak guidance, distribution pattern |

| Infosys | HOLD | 2% decline, sector weakness, but oversold potential near support |

| Vedanta | BUY | Metal sector +1.72%, commodities rally, gold at $4,261 |

| Nifty PSU Bank ETF | BUY | Sector +0.72%, outperformance vs private banks, credit cycle turn |

| Nifty IT ETF | HOLD | Sector -0.16%, rotational weakness, oversold but no catalyst yet |

7. Tomorrow’s Setup — Global Cues & Calendar

Thursday’s open hinges on five factors:

-

GIFT Nifty flat at 24,624.65: No overnight gap expected. The session will likely open within 50 points of Wednesday’s close.

-

US tech euphoria: Nasdaq’s 2.59% surge and S&P 500’s 1.79% rally set a risk-on tone, but India’s IT sector failed to mirror the move. Watch for catch-up trades in TCS, Infosys, Tech Mahindra.

-

Asian strength: Nikkei’s 3.66% surge and Hang Seng’s 0.24% gain suggest regional flows remain positive. ASX +0.90% confirms commodity optimism.

-

Crude and currency: Brent at $80.49 and WTI at $76.37 put marginal pressure on importers, but rupee stability at ₹95.12 offers a buffer. Gold’s 4.05% spike to $4,261.20 may trigger safe-haven rotations.

-

RBI Policy Decision: The elephant in the room. Markets expect status quo on rates, but any hawkish tilt on inflation or dovish hint on future cuts will move the needle sharply.

Key Technical Levels:

– Nifty 50: Support at 24,500 (day’s low 24,497.95), resistance at 24,680 (day’s high 24,677.60). A break above 24,700 opens 24,850; below 24,500 targets 24,350.

– Bank Nifty: Support at 57,450, resistance at 57,950. The 58,000 psychological level remains critical.

– Sensex: Support at 78,200, resistance at 78,700 (headline noted Tuesday’s close at 78,429).

Watch for: LIC stabilisation after stake sale news, Nykaa follow-through, and any CAS-related volatility near the close.

8. The Honest Take

For long-term investors: Wednesday was a day to ignore the headline and study the footnotes. The Nifty’s 0.04% gain means nothing. What matters: Nykaa’s profit surge validates the consumer digital thesis, Embassy REIT’s leasing strength confirms India’s office market hasn’t died, and the microcap index’s six-month outperformance suggests risk appetite for growth hasn’t vanished. If you’re building positions in structural winners — tech, REITs, select auto — this sideways churn is a gift, not a threat. LIC’s 8.9% drop is government housekeeping, not business deterioration. Buy dips in quality, ignore the CAS noise, and remember that the best returns come from holding through confusion.

For active traders: The technicals are giving mixed signals, and that’s dangerous. TVS Motor is overbought, Thangamayil is breaking down despite strong sales, and Infosys is oversold without a catalyst. The VIX at 12.09 says “all clear,” but gold spiking 4.05% says “not so fast.” Tomorrow’s RBI decision is a coin flip that could gap markets either way. If you’re long, trail stops tight below 24,500 on Nifty. If you’re short, cover before RBI speaks — central bank surprises have a way of punishing the confident. The market’s internal rotation — metals up, media down, PSU banks outperforming private — suggests sector trades trump index trades right now. Play the pockets, not the benchmark.

“The stock market is filled with individuals who know the price of everything, but the value of nothing.” — Philip Fisher