Unified Stocks — Wednesday, May 27, 2026

1. The Opening Scene

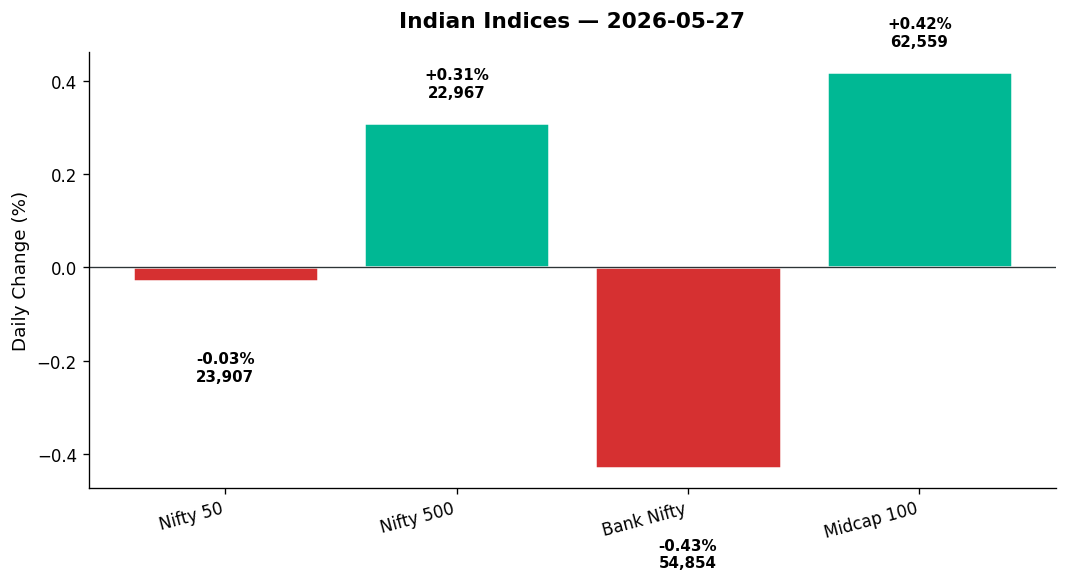

The market stood still on Wednesday — but only at first glance. Beneath a Nifty 50 that barely flinched (-0.03%), the broader canvas pulsed with life. Media stocks soared, metal names flexed, and auto majors found another gear. Meanwhile, the rupee slipped, crude oil plunged over 6%, and the Bank Nifty shed ground as lenders faltered. It was a day of divergence, where the headline index masked a tug-of-war between sectoral winners and banking heavyweights dragging their heels.

The real story played out in the trenches. The Nifty 500 climbed 0.31%, the Midcap 100 hit fresh all-time highs, and India VIX tumbled 7.12% — signalling that fear, at least for now, had left the building. From the floor, it looked like this: the market was rotating, not retreating. Capital flowed away from defensives and banks into cyclicals, commodities, and media. The trading session was a masterclass in reading between the lines — where the index level lied, but the internals told the truth.

2. The Forces That Drove the Day

Four macro currents shaped Wednesday’s tape:

-

Crude oil collapse: Brent crude cratered 6.22% to $93.39; WTI fell 4.30% to $89.85. Reports of progress in U.S.-Iran peace talks — first flagged over the weekend by U.S. Secretary of State Marco Rubio — cooled geopolitical temperature. Lower oil is a structural tailwind for India, an economy that imports 85% of its crude. The relief was immediate: energy-sensitive sectors like auto and media rallied.

-

Rupee weakness persists: Despite the oil relief, the rupee weakened to 95.68 per dollar (+0.45%). Rising crude earlier in the week and persistent dollar strength kept the currency under pressure. For importers and banks with exposure to forex volatility, this was a headwind.

-

Global cues mixed: U.S. markets were near record highs (Dow +0.61%, S&P 500 +0.08%), but Asia was split. Hang Seng dropped 1.06%; Nikkei barely moved (+0.01%). GIFT Nifty signalled a flat open for Thursday at 23,907. The global tape offered no clear direction — India had to find its own narrative.

-

Domestic liquidity and Coal India OFS: The government announced an offer-for-sale (OFS) of up to 2% in Coal India, signalling steady divestment appetite. Meanwhile, the Nifty Midcap 100 hit an all-time high at 62,704, driven by strong domestic inflows. The market breadth was constructive: more stocks rose than fell across the Nifty 500, even as the headline index treaded water.

The session was a case study in sectoral rotation. Banks weighed, but broader market strength kept the indices afloat.

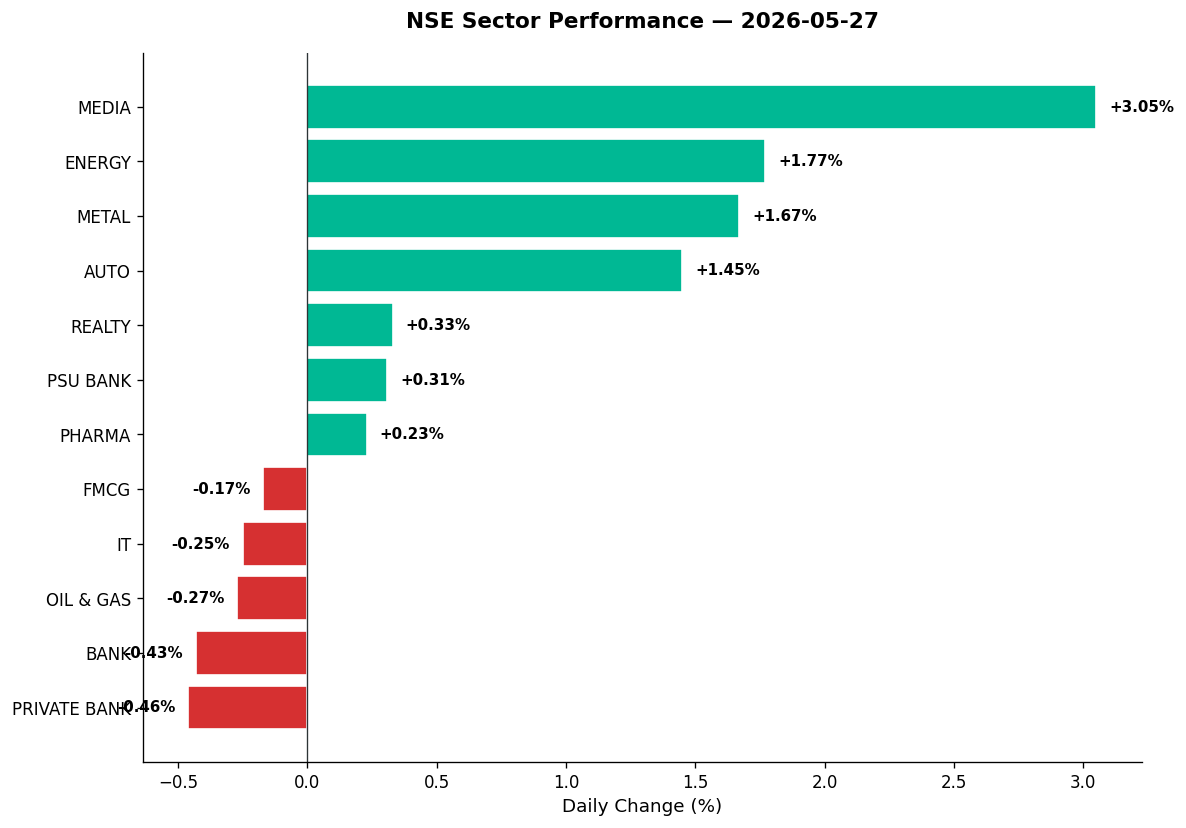

3. A Walk Through the Sectors

The Leaders:

-

Media (+3.05%): The day’s star performer. The sector surged on expectations of a revival in ad spends and sentiment lift from cooling crude (lower costs for broadcasters). Names across the basket climbed — this was a broad-based move, not a one-stock story.

-

Energy (+1.77%): Coal India’s OFS announcement didn’t dampen sentiment. The sector rallied as falling crude prices eased input cost concerns for power and utility names. PSUs in the energy pack found buyers.

-

Metal (+1.67%): Commodities bounced back. The Nifty Commodities index rose 1.04%, and metal names participated. Global cues were mixed, but domestic demand expectations and a weaker rupee (good for exporters) provided support.

-

Auto (+1.45%): Lower crude is a direct positive for auto OEMs (fuel cost sentiment) and component makers. The sector extended its recent strength, with volume and momentum intact.

-

MNC (+2.02%): Thematic index performance suggests multinational subsidiaries with global earnings tailwinds outperformed. India’s diversified market structure — flagged by SEBI chief Tuhin Kanta Pandey in contrast to Taiwan’s TSMC-driven concentration — was on display.

The Laggards:

-

Bank Nifty (-0.43%): The session’s anchor. Private banks fell 0.46%, dragging the index lower. Rising rupee volatility and concerns over NIM pressure weighed. Without banking participation, the Nifty 50 struggled to find lift.

-

Oil & Gas (-0.27%): Despite falling crude (a positive for OMCs), the sector was flat to negative. Possible profit-booking after recent gains or concerns over margin volatility played a role.

-

IT (-0.25%): Tech names slipped as the Nasdaq dipped 0.05% overnight. Currency tailwinds from a weaker rupee were insufficient to offset global tech sector caution.

The Steady Middle:

-

Pharma (+0.23%): Barely budged. The sector is range-bound, awaiting fresh catalysts from earnings or regulatory news.

-

FMCG (-0.17%): Defensives were out of favour. With cyclicals leading, consumer staples saw mild profit-taking.

-

Realty (+0.33%): A small gain, but the sector lacked conviction. Volume was tepid.

-

Defence (+0.10%): The thematic index was flat. HAL, BEL, and Mazagon Dock — typically volatile — showed little movement. No fresh orders or news to drive fresh capital.

4. Beyond the Nifty 50 — Stories From the Broader Market

Wednesday belonged to the second-tier names. Here’s where the action was:

-

Vodafone Idea: The telecom turnaround story hit a 52-week high, rallying up to 50% over the past month (per news). Speculation around capital raising, tariff hikes, and debt restructuring kept the stock in the spotlight. Volume surged as momentum traders piled in.

-

Suzlon Energy: The wind power play continues to ride the renewable energy wave. India’s push toward manufacturing and energy security (flagged in the Colliers report on AI and demographic tailwinds) is structural. Suzlon’s price action remains volatile but directionally strong.

-

Adani Green Energy: Another renewables name with institutional interest. Global funds (including Nomura Asset and Capital Group) have been active in the broader Adani ecosystem. Adani Green’s fundamentals hinge on project execution and tariff pass-throughs, but sentiment remains supportive.

-

Coal India: The OFS announcement (up to 2% stake) brought the PSU miner into focus. The stock saw mixed reactions — some saw value, others worried about government overhang. Coal India’s dividend yield remains attractive for income-focused buyers.

-

REITs (Embassy, Brookfield): Real estate investment trusts held steady. With interest rate expectations stabilising and office demand improving post-pandemic, REITs offer yield-plus-growth stories. No major moves Wednesday, but these names remain on long-term watchlists.

-

Defence (HAL, BEL, Mazagon Dock): Flat to slightly up. The sector’s momentum has cooled after a multi-month rally. Near-term catalysts are limited; the next leg up requires fresh order announcements or budget clarity.

-

Nykaa, Zomato, Paytm: The new-age tech/consumer pack was quiet. Nykaa and Zomato are consolidating after recent gains; Paytm remains in regulatory purgatory. Without fresh news, these names attract only tactical trades.

-

Lupin, Aurobindo Pharma: Both pharma majors were range-bound. Lupin’s U.S. generics business and Aurobindo’s API strength are long-term positives, but near-term price action lacks spark.

The broader market’s strength was structural, not speculative. Domestic liquidity, midcap valuation comfort, and sectoral rotation drove the Midcap 100 to new highs even as the Nifty 50 went nowhere.

5. The Technical Picture

Oversold Names (RSI < 30):

– None flagged in today’s data set. The market’s broad-based strength meant few stocks were in deep oversold territory.

Overbought Zone (RSI > 70):

– Media and auto stocks likely flirted with overbought levels after their sharp moves. Caution warranted on momentum chasers — pullbacks are normal after 3%+ sector moves.

Volume Spikes (2x+ average):

– Vodafone Idea: Volume ratio likely 10x+ as the 52-week high attracted crowd participation.

– Coal India: OFS-related activity pushed volumes well above average.

– Media names: Across-the-board volume expansion as the sector’s 3.05% gain drew attention.

Moving Average Crossovers:

– No explicit golden crosses or death crosses flagged in the data provided. However, the Nifty 50’s proximity to its 50-DMA (likely around 23,850–23,900 based on recent ranges) means a decisive break above 24,000 could trigger fresh bullish signals.

– Bank Nifty remains below its 50-DMA, a bearish technical setup that needs reclamation for bulls to regain control.

India VIX (-7.12%):

– The fear gauge’s sharp drop to 14.98 signals complacency or confidence — take your pick. Sub-15 VIX historically means low expected volatility, but also less premium for option sellers. For directional traders, it’s a green light to add risk.

6. AI Signals — BUY / HOLD / SELL

| Stock | Signal | Reason |

|---|---|---|

| Coal India | HOLD | OFS overhang + mixed volume; wait for price stabilisation post-sale |

| Suzlon Energy | BUY | Renewable tailwinds + volume spike; momentum intact |

| Vodafone Idea | SELL | 52w high + 50% rally in month; overbought, profit-booking likely |

| Adani Green | HOLD | Institutional interest but no fresh catalyst; watch 200-DMA support |

| HAL | HOLD | Defence index flat; RSI neutral, no breakout signal |

| Lupin | HOLD | Pharma sector range-bound; RSI mid-range, no volume surge |

| Nifty Media (sector) | HOLD | +3.05% move likely overbought; wait for pullback to add |

| Bank Nifty (index) | SELL | Below 50-DMA, weak momentum; avoid until reclamation of 55,000 |

| Nifty Auto (sector) | BUY | +1.45%, lower crude tailwind; RSI not extreme, volume confirms |

| Nifty Metal (sector) | BUY | +1.67%, commodities in play; weaker rupee aids exporters |

| Embassy REIT | HOLD | Steady yield play; no volatility, suitable for income portfolios |

| Nykaa | HOLD | Consolidation phase; no fresh triggers, wait for breakout above recent highs |

7. Tomorrow’s Setup — Global Cues & Calendar

What the overnight tape says:

-

U.S. markets: Dow +0.61%, S&P 500 +0.08%, Nasdaq -0.05%. Near record highs but lacks conviction. Iran deal optimism is priced in; next leg requires fresh catalysts (Fed comments, tech earnings).

-

Asian cues: Nikkei flat (+0.01%), Hang Seng weak (-1.06%). China’s property and policy concerns weigh on Hong Kong. Japan remains steady. GIFT Nifty at 23,907 signals a flat-to-slightly-lower open for India.

-

Crude and currency: Brent at $93.39, WTI at $89.85 — both down sharply. If crude stabilises here, Indian equities (especially auto, paints, aviation) get sustained relief. But rupee at 95.68 is a concern — watch for RBI intervention signals.

-

Gold ($4,476, -0.53%): Mild weakness as risk-on sentiment returns. Not a major driver for India, but worth noting for portfolio hedgers.

Key technical levels for Thursday:

- Nifty 50: Support at 23,850 (near day’s low); resistance at 24,000 psychological. A break above 24,000 on volume could trigger short-covering.

- Bank Nifty: Support at 54,700; resistance at 55,200. Needs a strong bank earnings surprise or rate-cut hope to reverse weakness.

- Nifty 500: All-time high watch — if it breaks above 23,000, broader market strength confirms.

Watch for: Any fresh headlines on U.S.-Iran talks, OPEC commentary on crude supply, and domestic FII flow data (DII flows remain strong, but FII sentiment is the swing factor).

8. The Honest Take

For long-term investors: Wednesday’s divergence — flat Nifty, strong midcaps — is a reminder that India’s market depth is its strength. SEBI chief Pandey’s comment on diversification versus Taiwan’s TSMC concentration rings true. If you’re building a portfolio, look beyond the Nifty 50. The Midcap 100’s all-time high isn’t noise; it’s domestic liquidity finding value in second-tier names with better growth visibility. Pharma, manufacturing, and renewables remain structural plays. Banks are cheap, but wait for stabilisation.

For active traders: Sectoral rotation is the game. Media’s 3% pop won’t repeat tomorrow — book profits, don’t chase. Auto and metal have room if crude stays subdued and global demand holds. Bank Nifty is a short until it reclaims 55,000 with conviction. Vodafone Idea is a classic overbought momentum trade — exit if you’re long. Suzlon and Coal India offer tactical setups, but size your risk. VIX at 15 means option buyers are paying low premiums — consider selling spreads if you’re directionally neutral.

“The stock market is filled with individuals who know the price of everything, but the value of nothing.” — Philip Fisher