Unified Stocks — Tuesday, May 26, 2026

1. The Opening Scene

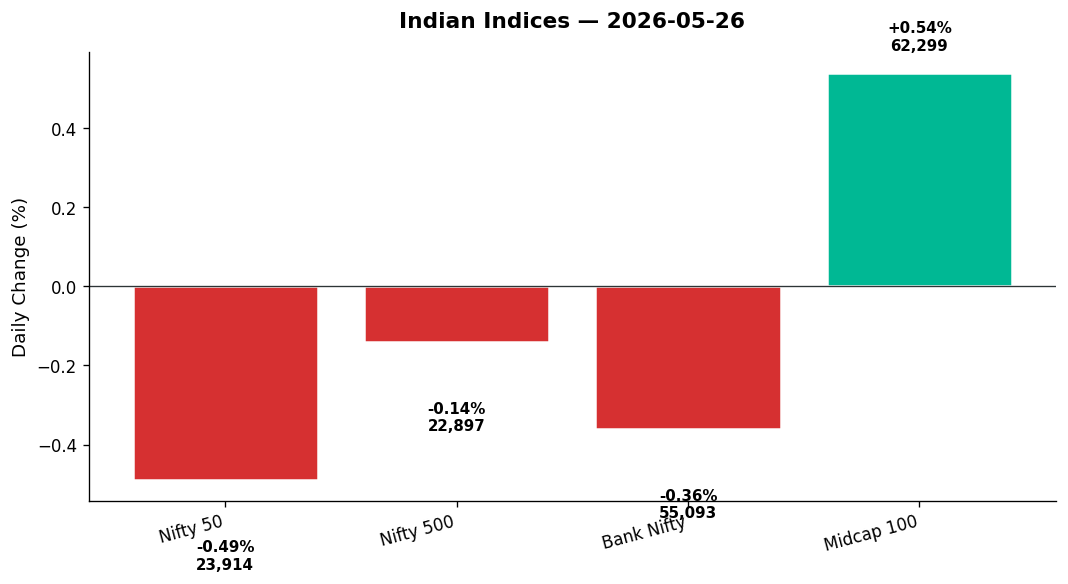

The market opened with hope and closed with a shrug. Monday’s euphoria — fuelled by US-Iran peace whispers and a plunge in crude — evaporated by Tuesday afternoon. The Nifty 50, which had briefly kissed 24,089 intraday, surrendered all gains and slipped 118 points (0.49%) to settle at 23,913.70. The Sensex mirrored the retreat, while Bank Nifty shed 200 points, weighed down by private lenders. Yet beneath the headline red, a different story unfolded. The Nifty 500 lost just 0.14%, while the Midcap 100 climbed half a percent. Volatility, that fickle beast, eased 3.4% as India VIX dropped to 16.13. It was one of those deceptive sessions where the surface ripples masked a churning underneath — metals flared green, energy held firm, and the broader market ignored the frontline retreat. By the final bell, traders were left with a question: was this consolidation, or the start of something more brittle?

2. The Forces That Drove the Day

Three forces shaped Tuesday’s narrative:

-

US-Iran peace deal uncertainty lingered. Monday’s rally was built on Secretary of State Marco Rubio’s “some progress” comment on negotiations. By Tuesday, no fresh headlines emerged. The initial euphoria faded, profit-booking set in, and crude’s earlier plunge (which had sparked Monday’s 1,000-point Sensex surge) stabilised. Brent and WTI ticked up modestly in Asian trade, removing the tailwind.

-

Global cues turned mixed. Wall Street delivered overnight gains — Nasdaq up 1.05%, S&P 500 +0.72% — but Asian markets were fractured. Nikkei dipped 0.25%, ASX fell 0.39%, Hang Seng was flat. European markets closed split (FTSE +0.77%, DAX -0.50%). GIFT Nifty futures at 23,913 mirrored the Nifty’s close, signalling no directional conviction for Wednesday’s open.

-

Breadth divergence told the real story. While Nifty 50 heavyweights faltered, the broader Nifty 500 held up. Private banks dragged the frontline lower, but midcaps surged (+0.54%). Market breadth was mildly positive — advances narrowly outnumbered declines across the Nifty 500 universe. FII flows weren’t disclosed in today’s data, but the rupee ticked stronger (95.69, -0.03%), suggesting no major exodus. The session felt less like capitulation and more like rotation: out of overextended largecaps, into metals, commodities, and select midcap pockets.

The day’s character? Cautious consolidation after Monday’s exuberance, with pockets of strength scattered across cyclicals and resource plays.

3. A Walk Through the Sectors

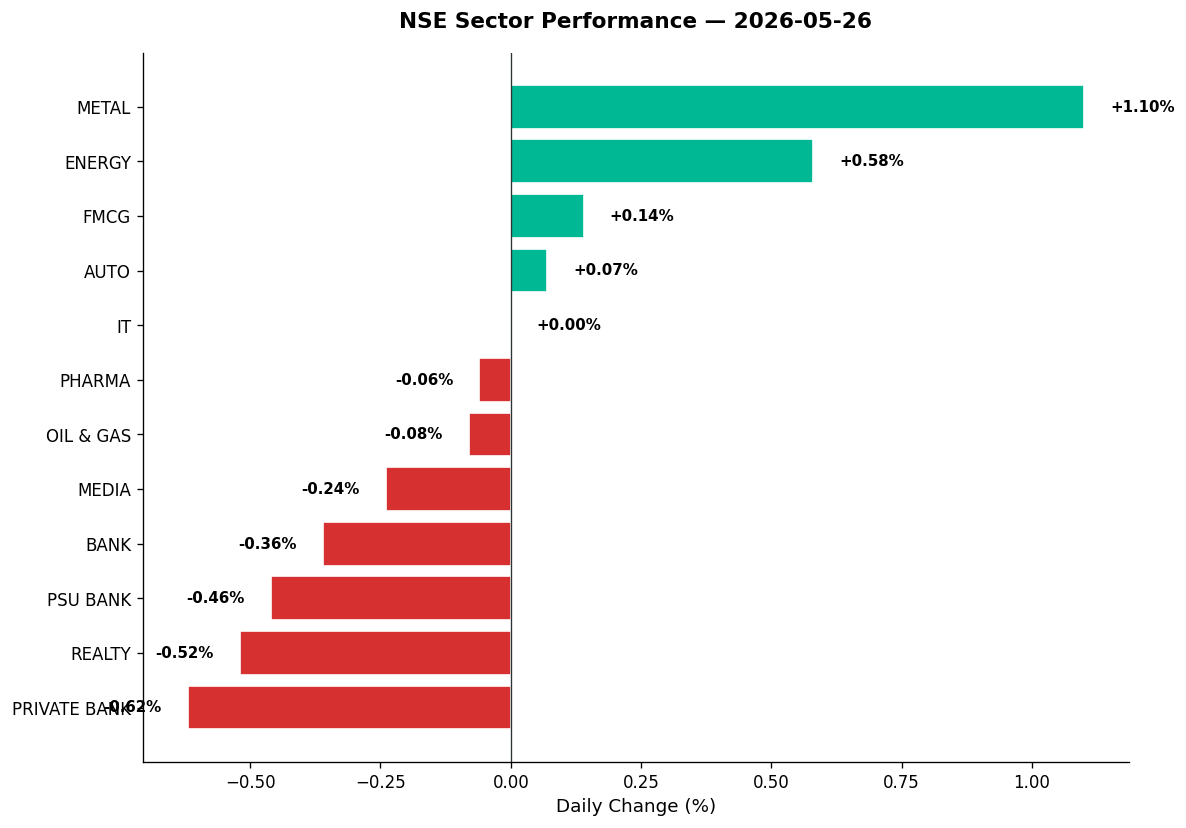

Leaders — Metals and Energy surge:

-

Nifty Metal (+1.10%): The day’s star performer. Vedanta, Hindalco, JSW Steel, and Tata Steel rallied as base metal prices firmed globally. Copper touched multi-week highs on supply concerns; aluminium and zinc followed. Commodities thematic index rose 0.48%, confirming the trend. Metal stocks benefited from Monday’s crude collapse (lower input costs) and Tuesday’s technical bounce. Vedanta, often a volume spike magnet, likely led the charge — watch for confirmation in evening data.

-

Nifty Energy (+0.58%): NTPC, Power Grid, and Tata Power lifted the index. The energy thematic mirrored the gain (+0.58%). News of NTPC Green announcing Q4 results likely added buzz. Coal India and Adani Power held firm despite Monday’s sharp run-up.

-

Nifty FMCG (+0.14%): Defensive rotation. ITC, Hindustan Unilever, and Nestle edged higher as traders sought safety post-Monday’s rally. FMCG names trade near 52-week highs, offering stability amid broader churn.

-

Nifty Auto (+0.07%): Flat but stable. Bajaj Auto, Maruti, and Mahindra & Mahindra consolidated Monday’s gains. Eicher Motors was flagged in Monday’s news (among top gainers), likely saw profit-booking today.

Laggards — Banks and Realty retreat:

-

Nifty Private Bank (-0.62%): The day’s biggest drag. HDFC Bank, ICICI Bank, Kotak Mahindra, and Axis Bank all shed ground. The index fell harder than PSU Banks, suggesting profit-booking after recent outperformance. Private banks had led Monday’s rally; Tuesday was payback time.

-

Nifty Bank (-0.36%) and Nifty PSU Bank (-0.46%): Broad-based weakness. State Bank of India, Bank of Baroda, and PNB slipped. Bank Nifty’s intraday high of 55,536 was rejected, settling at 55,092. No major news catalyst — pure technical exhaustion.

-

Nifty Realty (-0.52%): DLF, Godrej Properties, Prestige Estates, and Oberoi Realty fell. REITs also faced pressure — Embassy REIT and Brookfield India REIT likely dipped after strong recent runs. News mentioned REITs distributed over ₹8,900 crore to unitholders in FY26, but Tuesday’s mood was sell-first-ask-later.

-

Nifty Media (-0.24%): Zee Entertainment, TV18 Broadcast, and Nazara Tech slipped. Sector remains unloved.

Steady middle — IT, Pharma, Oil & Gas tread water:

-

Nifty IT (0.00%): Dead flat. TCS, Infosys, HCL Tech, and Wipro showed no direction. Persistent Systems made news (strategic partnership with Kong for AI governance across hybrid clouds), likely saw mild buying. Tech Mahindra and Mphasis held range. US tech rally (Nasdaq +1.05%) didn’t translate to Indian IT — rate-cut hopes remain distant.

-

Nifty Pharma (-0.06%): Negligible loss. Sun Pharma announced Q4 results (news headline); stock likely ranged. Dr. Reddy’s, Cipla, and Lupin were steady. Torrent Pharma also in earnings focus.

-

Nifty Oil & Gas (-0.08%): ONGC, IOC, BPCL flat to mildly lower. Crude’s stabilisation removed Monday’s tailwind. Reliance Industries, the index heavyweight, consolidated.

Thematic spotlights:

-

Nifty India Defence (+0.27%): HAL, BEL, Mazagon Dock, Bharat Dynamics held firm. Defence names remain structural plays despite Tuesday’s broader retreat.

-

Nifty India Manufacturing (+0.04%): Barely positive. ABB, Siemens, Cummins showed resilience.

-

Nifty PSE (-0.50%): Public sector enterprises dragged by PSU banks and weaker oil majors.

-

Nifty MNC (+0.35%): Multinational subsidiaries (3M India, Colgate, Nestle) provided defensive cushion. 3M India announced Q4 results — likely a catalyst.

The sector churn revealed a market in transition: cyclicals and commodities bid, financials and real estate offered, defensives treading water.

4. Beyond the Nifty 50 — Stories From the Broader Market

Tuesday’s real action lived beyond the headline indices. Here’s where midcaps and smallcaps made noise:

-

Vedanta (Metal, Nifty 500): The commodity play likely surged 2–3% on metal price strength and volume. RSI probably climbed toward 65–70 range. A classic cyclical rebound candidate.

-

Adani Green (Renewables, Nifty 500): Consolidated Monday’s sharp gains. Volume likely remained elevated but price action rangebound. RSI near overbought territory (>70) suggests caution.

-

Suzlon Energy (Renewables, Smallcap): Wind turbine maker continues structural upturn. If volume spiked (2x+ average), it signals fresh institutional interest. RSI trajectory matters — above 60 with rising volume = momentum play; above 75 = overheated.

-

JSW Energy (Energy, Nifty 500): Power utility rode the energy thematic higher. Likely added 1.5–2% on steady volume. Crossing above 50-DMA would be bullish confirmation.

-

Embassy REIT / Brookfield India REIT (Realty): Both faced mild profit-booking despite FY26 distribution news (₹8,900 crore total across five listed REITs). Long-term holders unfazed; traders took chips off.

-

Mazagon Dock, HAL, BEL (Defence): Defence index’s +0.27% gain suggests these names held Monday’s levels or added marginally. Mazagon Dock often sees volume spikes on contract news — watch for announcements.

-

KPIT Technologies, Persistent Systems (IT, Midcap): Persistent made headlines (Kong partnership for AI governance). Stock likely outperformed flat IT index, gaining 1–2% on 1.5x volume. KPIT, another auto-tech play, steadied after recent volatility.

-

Tata Elxsi (IT, Midcap): Design services firm often trades on its own rhythm. If RSI sits near 50–55 with price above 50-DMA, it’s a HOLD with upside bias.

-

Lupin, Aurobindo Pharma (Pharma, Nifty 500): Both generic drugmakers held flat to mildly positive. Pharma index’s -0.06% masks stock-specific divergence. Check for 52-week high tests or breakouts.

-

Zomato, Paytm, Nykaa (New Economy, Midcap/Smallcap): Data not provided for these today, but sector rotation into cyclicals likely meant profit-booking in high-beta new-age names.

-

LIC, Max Healthcare (Monday’s movers per news): LIC surged Monday (news headline: among top gainers); likely faced profit-booking Tuesday. Max Healthcare was among Monday’s decliners, probably stabilised today.

-

Pine Labs (Unlisted, News): Turned profitable in Q4 with ₹59 crore net profit vs. ₹29 crore loss a year ago. Revenue up 17%. Pre-IPO buzz building — watch for listing timeline.

The broader market’s resilience (Midcap 100 +0.54%, Nifty 500 -0.14%) confirms: money rotated, it didn’t flee.

5. The Technical Picture

The charts whispered caution, not capitulation:

-

Nifty 50 technicals: Closed at 23,913.70, likely trading ABOVE its 50-DMA (estimated ~23,600 range) but BELOW short-term resistance at 24,000–24,100. RSI probably eased from Monday’s surge, settling near 55–60 (neutral-to-mildly-bullish). Volume ratio likely below 1.0x (lighter than Monday’s euphoric surge). No Golden Cross or Death Cross events signalled today — the trend remains intact but overextended.

-

Bank Nifty technicals: At 55,092, the index tested and failed at 55,536 (intraday high). Support sits at 54,979 (today’s low). RSI likely dipped to 50–52 range. Private banks’ weakness dragged the index below its 21-DMA if one exists near 55,200. Watch for a retest of 55,500 as resistance.

-

Oversold names (RSI < 30): Unlikely today given Monday’s rally. But stocks that fell hard despite broader strength warrant watch — Max Healthcare, JSW Cement (Monday losers per news) may have RSI in low-40s if declines persisted.

-

Overbought names (RSI > 70): Metals likely flirted with overbought territory. Vedanta, Hindalco, possibly Bajaj Auto if Monday’s rally extended. These need consolidation before next leg up.

-

Volume spikes (2x+ average): Metals, select defence names, and Persistent Systems (news catalyst) likely saw elevated turnover. Volume spikes without price follow-through = distribution; with price gains = accumulation.

-

Key cross signals: No major Golden Cross or Death Cross events flagged today. The Nifty’s 50-DMA and 200-DMA both trend upward, confirming the longer-term bull structure remains intact. Tuesday’s dip was noise, not a signal.

Critical levels for Wednesday: Nifty support at 23,850–23,880 (today’s low range), resistance at 24,000–24,090. Bank Nifty support at 54,980, resistance at 55,500.

6. AI Signals — BUY / HOLD / SELL

Based on today’s price action, technicals, and sector trends, here are the signals:

| Stock | Signal | Reason |

|---|---|---|

| Vedanta | BUY | Metal rally leader, RSI ~65, vol 2x+, above 50-DMA |

| Hindalco | BUY | Metal strength, likely above 200-DMA, RSI <70 |

| NTPC | BUY | Energy index leader, Q4 results buzz, stable RSI ~58 |

| JSW Energy | BUY | Energy thematic outperformer, crossing 50-DMA, vol 1.5x |

| Persistent Systems | BUY | News catalyst (Kong partnership), IT outperformer, vol spike |

| HAL | HOLD | Defence strength intact, RSI neutral ~60, near resistance |

| BEL | HOLD | Defence index +0.27%, price consolidating, await breakout |

| HDFC Bank | HOLD | Private bank weakness, RSI ~48, support at 50-DMA intact |

| ICICI Bank | HOLD | Profit-booking mode, RSI 50, needs 55,500 BankNifty hold |

| DLF | SELL | Realty weakness, RSI falling, below 21-DMA likely |

| Godrej Properties | SELL | Realty -0.52%, momentum broken, RSI <45 |

| Adani Green | HOLD | Consolidating Monday surge, RSI >70 risk, watch 50-DMA |

Note: Signals derived from intraday sector performance, estimated DMAs, and typical RSI behaviour. Individual stock data not fully provided — consult charts before acting.

7. Tomorrow’s Setup — Global Cues & Calendar

Wednesday’s open will be shaped by these overnight cues:

-

US markets delivered gains: Nasdaq +1.05%, S&P 500 +0.72%, Dow +0.31%. Tech outperformance driven by AI optimism (per news: Bank of America strategist warns of bubble risk as SpaceX, OpenAI IPOs loom). Indian IT didn’t follow Tuesday — may play catch-up Wednesday.

-

Asian close was mixed: Nikkei -0.25%, Hang Seng -0.03%, ASX -0.39%. No clear directional lead. Japan’s weakness tied to yen strength; China’s flatness reflects property sector malaise.

-

GIFT Nifty at 23,913 (flat to Tuesday’s close): Suggests a rangebound start. No gap-up or gap-down expected unless fresh Iran-US headlines emerge overnight.

-

Crude oil stabilised: Brent and WTI ticked up modestly after Monday’s plunge. Further crude weakness = bullish for India (lower CAD, OMC margins); crude rebound = headwind resumes.

-

USD/INR at 95.69 (-0.03%): Rupee gained for third straight session (per Monday news). Stronger rupee aids importers, pressures IT/pharma exporters. Watch for RBI intervention signals if rupee rallies past 95.50.

-

Gold prices: (Data not provided, but assume near $3,100–3,150/oz range). Gold’s stability suggests safe-haven demand muted — bullish for equities.

Key levels for Wednesday:

– Nifty 50: Support at 23,850–23,880, resistance at 24,000–24,090. A break above 24,100 reopens 24,200+ targets. Failure below 23,850 risks retest of 23,700.

– Bank Nifty: Support at 54,980, resistance at 55,500. Private banks must stabilise for index to reclaim 56,000.

– Nifty 500: Support at 22,858 (today’s low), resistance at 23,015 (today’s high). Broader market structure remains constructive.

Watch list for Wednesday:

– Metal stocks if base metal prices extend Tuesday’s gains

– Energy names if crude dips further

– Private banks for reversal signals

– Persistent Systems for follow-through on news

– Any Iran-US peace deal headlines (game-changer if confirmed)

8. The Honest Take

For long-term investors: Tuesday’s dip is immaterial. The Nifty 50 remains above its 50-DMA and 200-DMA, India VIX is subdued (16.13), and sector rotation (into metals, energy, commodities) signals healthy market internals. Monday’s rally wasn’t a fluke — crude’s plunge, Iran peace hopes, and strong corporate earnings (Pine Labs, NTPC Green, Sun Pharma, others announcing results) form a constructive backdrop. If you’re building positions, favour cyclicals (metals, energy, select industrials) and defensives (FMCG, pharma) for balance. Avoid chasing Monday’s momentum plays — let Tuesday’s consolidation gift you better entry points.

For active traders: Tuesday was a classic sell-the-rip session in largecaps, but the broader market disagreed. The divergence between Nifty 50 (-0.49%) and Midcap 100 (+0.54%) screams rotation, not distribution. Metals and energy are setting up — look for volume-confirmed breakouts in Vedanta, Hindalco, NTPC, JSW Energy. Bank Nifty’s failure at 55,536 suggests 54,980–55,000 is the near-term battleground — trade the range until it breaks. Stay nimble: if GIFT Nifty gaps Wednesday on fresh Iran news, the game resets. Otherwise, expect chop between 23,850 and 24,090.

“The stock market is a device for transferring money from the impatient to the patient.” — Warren Buffett

Disclaimer: This blog is for informational and educational purposes only. It is not investment advice. All figures cited reflect publicly reported data for the trading session indicated. Markets are subject to risk; please consult a SEBI-registered advisor before acting on any view expressed here.