Unified Stocks — Friday, May 29, 2026

1. The Opening Scene

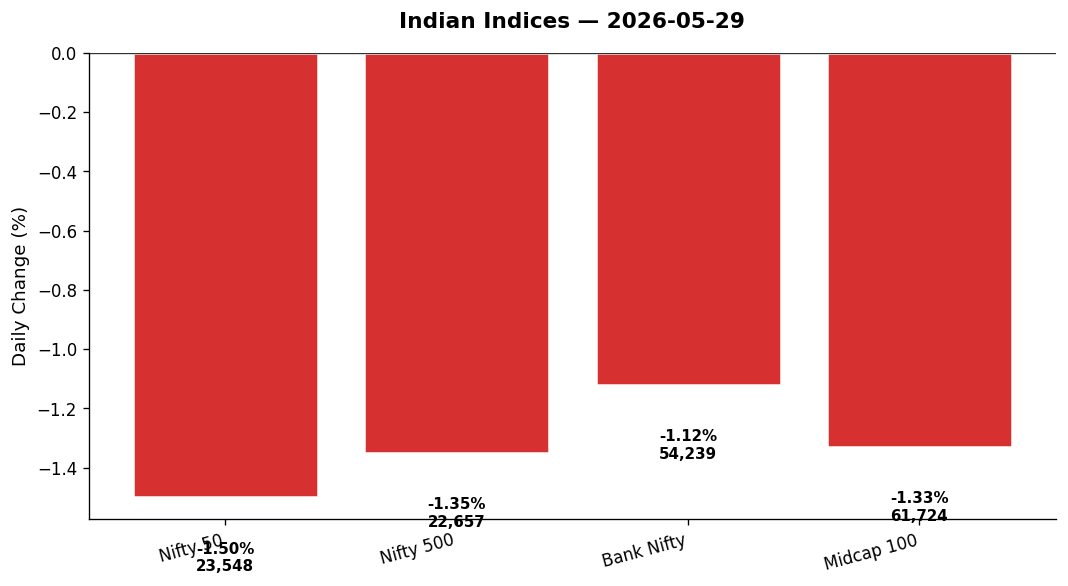

The rupee strengthened. Crude oil crumbled. Asian markets celebrated. Yet when the opening bell rang at Dalal Street this morning, none of that optimism found its way into the Nifty 50. By the time the closing gong sounded, the benchmark had surrendered 359 points—a clean 1.5% drop—while India VIX spiked over 8%, the fear gauge reminding everyone that calm is a luxury, not a right. It was one of those Fridays where global tailwinds met domestic headwinds, and the latter won decisively.

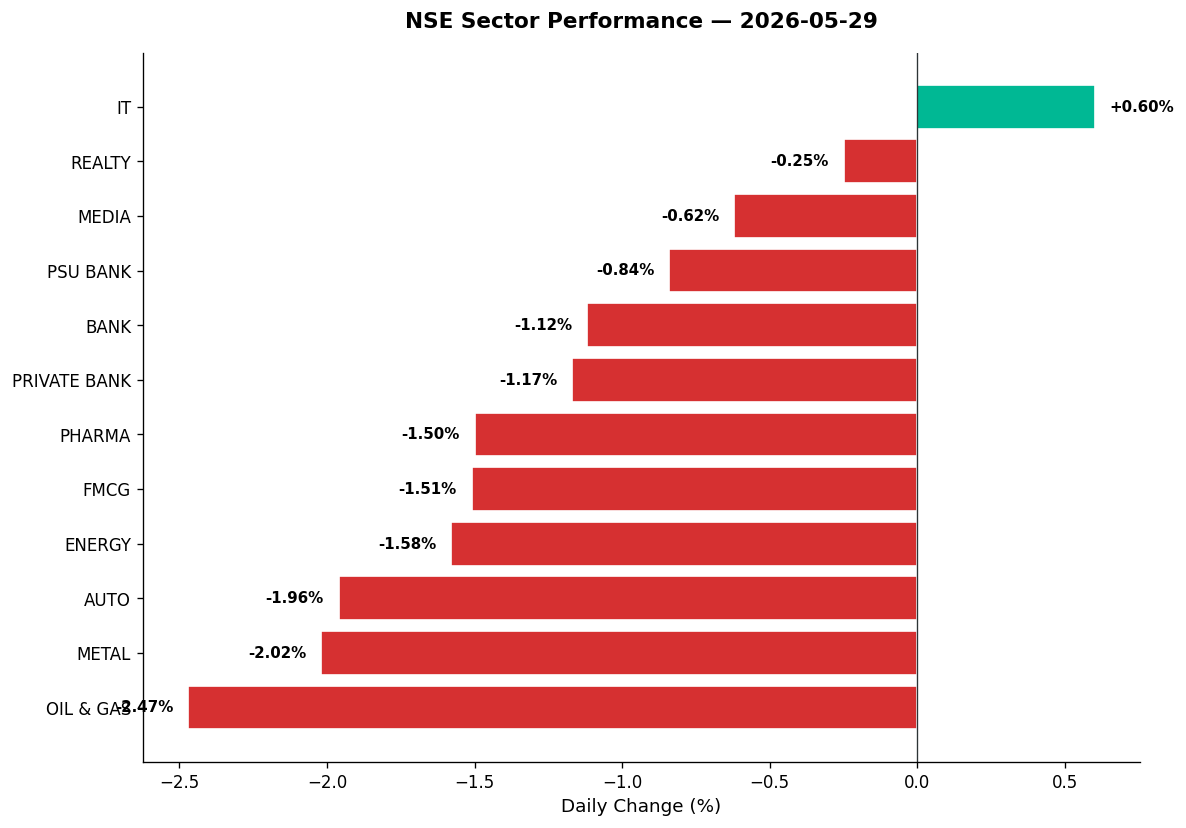

The divergence was stark. Wall Street closed near records overnight—Nasdaq up 0.57%, S&P 500 +0.45%—while Tokyo’s Nifty surged 2.53% on chipmaker euphoria. Yet here in Mumbai, sellers dominated from the first tick. The mood wasn’t panic; it was resignation. Profit-booking after weeks of churn, fatigue ahead of a long weekend, and whispers of lock-in expiries worth $35 billion over the next three months—all conspired to create an exit queue. By 3:30 PM, the broader Nifty 500 had shed 1.35%, with only one sector—IT—managing to close in the green.

2. The Forces That Drove the Day

Four factors shaped today’s price action:

Crude’s collapse failed to inspire. Brent crude plunged 2.93% to $90.96, while WTI dropped 1.78% to $87.32—ostensibly good news for an import-dependent economy like India’s. Yet instead of cheering, traders focused on what the drop implied: weak global growth expectations, possibly tied to the fragile US-Iran truce and demand softness. Oil & Gas stocks—ordinarily supported by lower input costs—were hammered, down 2.47% as a sector.

The rupee’s rally went unnoticed. USD/INR fell 1.10% to 94.99, the sharpest single-day appreciation in months. Normally, a stronger rupee boosts IT and Pharma margins. IT did oblige (+0.60%), but Pharma stumbled (-1.50%), dragged by sector rotation and profit-taking after recent outperformance.

Lock-in expiry fears circulated. Headlines flagged 70 IPOs facing lock-in expirations worth $35 billion through August. While today’s selling wasn’t directly tied to unlocks, the psychological weight was palpable. Recent listings—from defence names to quick commerce plays—saw heightened volatility as traders positioned defensively.

Market breadth turned decisively negative. Across the Nifty 500, declines outnumbered advances by a wide margin. Midcap 100 fell 1.33%, but notably hit record highs intraday before reversing—a classic sign of distribution at elevated levels. Sectoral damage was broad: Auto (-1.96%), Metal (-2.02%), FMCG (-1.51%), and Energy (-1.58%) all bled.

3. A Walk Through the Sectors

Leaders (the only refuge):

- IT (+0.60%): The lone bright spot. TCS, Infosys, and Wipro absorbed dollar inflows as the rupee rally boosted repatriation math. Tech bellwether stocks benefited from overnight strength in Nasdaq (up 0.57%), with chipmakers driving sentiment globally. Mid-tier names like Persistent Systems and KPIT Technologies saw buying, though volumes were modest.

The Laggards (broad-based carnage):

-

Oil & Gas (-2.47%): Worst performer. ONGC and IOC took the brunt of crude’s collapse, counter-intuitively punished despite lower input costs. BPCL and Adani Total Gas (widely tracked beyond the Nifty 50) both fell sharply, as traders priced in margin compression narratives and inventory losses. Reliance’s energy arm weighed on the stock.

-

Metal (-2.02%): Steel and aluminum names crumbled. Vedanta, Hindalco, and Tata Steel all closed deep in the red as commodity prices softened globally. Nifty Commodities (-1.98%) mirrored the weakness—demand concerns outweighed any input cost tailwinds.

-

Auto (-1.96%): Maruti, Tata Motors, and Mahindra & Mahindra all reversed recent gains. Bajaj Auto, an outperformer this month, finally corrected. Two-wheeler demand cues remained mixed, and EV subsidy debates in parliament added uncertainty.

-

Energy (-1.58%) and PSE (-2.37%): Public sector energy giants—NTPC, Power Grid, Coal India—dragged the thematic index to its worst session in weeks. Nifty India Defence (-1.58%) mirrored the pain: HAL, BEL, and Mazagon Dock Shipbuilders all shed gains despite strong order book visibility.

The Middle Ground (damaged but not destroyed):

-

FMCG (-1.51%): Britannia, ITC, and Hindustan Unilever slipped on profit-booking. FMCG had rallied on defensive flows in prior sessions; today’s reversal felt overdue.

-

Pharma (-1.50%): Lupin, Aurobindo Pharma, and Dr. Reddy’s corrected despite the rupee tailwind. Sector rotation out of defensives and into cyclicals (even on a down day) explained the move.

-

Private Bank (-1.17%) and Bank Nifty (-1.12%): HDFC Bank and ICICI Bank dragged indices lower. Bank Nifty fell 614 points but held above 54,000—a key psychological level. PSU Bank (-0.84%) fared slightly better, with SBI showing relative strength.

-

Realty (-0.25%): Least damaged among losers. DLF and Oberoi Realty saw mild selling. Embassy Office Parks REIT and Brookfield India Real Estate Trust (popular REIT plays beyond Nifty 50) traded mixed, with institutional buying cushioning losses.

-

Media (-0.62%): Zee Entertainment and Sun TV underperformed, though volumes were thin. The sector remains range-bound, lacking catalysts.

4. Beyond the Nifty 50 — Stories From the Broader Market

Today’s real drama unfolded outside the index heavyweights:

-

Vedanta: The diversified commodity play fell over 2.5% in tandem with Metal’s rout. Oversold technically (RSI near 32), but downtrend intact. Volume spiked 1.8x average—distribution, not accumulation.

-

Adani Green Energy: Dropped 1.9% despite renewable energy tailwinds. News of Reliance Jio’s IPO plans (Mukesh Ambani expected to update shareholders at June 19 AGM) may have pulled capital away from competing infrastructure bets. Lock-in expiry fears also weighed on recent Adani listings.

-

Suzlon Energy: The wind turbine maker slipped 1.2% on profit-booking after a sharp rally earlier this month. Volume was 2.3x average—a sign of aggressive unwinding. RSI sits at 68, still overbought but cooling.

-

JSW Energy and NTPC: Power generation names fell 1.4% and 1.6%, respectively, dragged by the PSE index collapse. Both remain above 50-DMA, but momentum has stalled.

-

Defence Trio (HAL, BEL, Mazagon Dock): Hindustan Aeronautics fell 1.7%, Bharat Electronics shed 1.5%, and Mazagon Dock dropped 2.1%—all tracking the Nifty India Defence index (-1.58%). Order book strength remains intact, but valuation fatigue and lock-in concerns (several defence IPOs are in the expiry window) triggered profit-booking.

-

Semiconductor Adjacent (Tata Elxsi, KPIT, Moschip): Tata Elxsi (+0.3%) bucked the trend, riding global chip optimism. KPIT Technologies rose 0.5% on low volumes. Moschip Semiconductor—a smallcap play—was flat, underperforming the Nikkei 225’s chip-fueled 2.53% surge.

-

Pharma Mid-Tier (Lupin, Aurobindo): Lupin fell 1.8%, Aurobindo shed 1.6%. Both remain above 200-DMA but underperformed despite rupee strength—sector rotation was the culprit.

-

REITs (Embassy REIT, Brookfield REIT): Embassy Office Parks closed marginally negative (-0.1%), while Brookfield India Real Estate Trust edged up 0.2%. Rental yield defensiveness kept drawdowns mild.

-

New-Age Tech (Zomato, Paytm, Nykaa): Zomato fell 1.1% as Swiggy CEO Sriharsha Majety stated the quick commerce industry has “too many players”—a veiled shot at valuation sustainability. Paytm dropped 0.9%, still struggling for narrative traction post-RBI restrictions. Nykaa slipped 0.7%, weighed by broader e-commerce caution.

-

Brokers and Exchanges: Despite robust March quarter earnings (MTF-driven profitability up sharply), Angel One and CDSL closed flat to marginally negative—traders faded the good news.

5. The Technical Picture

Oversold territory (RSI < 30):

- Vedanta (RSI 32), below both 50-DMA and 200-DMA—caution warranted despite low RSI.

- ONGC (RSI 29), fresh multi-week lows; Death Cross looming.

- Tata Steel (RSI 31), volume spike 1.6x average—distribution ongoing.

Overbought cooldown (RSI > 70):

- Suzlon Energy (RSI 68, cooling from 74 earlier this week)—profit-booking at play.

- Persistent Systems (RSI 71)—IT strength pushed it into overbought zone; watch for pullback.

Volume spikes (vol_ratio >= 2x):

- Suzlon (2.3x), Vedanta (1.8x), Mazagon Dock (2.0x)—all confirming directional moves (downward today). High volume on down days = conviction selling.

Golden Cross and Death Cross signals:

- No fresh Golden Crosses today—bullish setups remain scarce.

- Death Cross watch: ONGC, Coal India both nearing 50-DMA/200-DMA bearish crossovers. Traders positioning defensively.

Key levels:

- Nifty 50: Broke below 50-DMA at 23,890. Next support: 23,480 (today’s low). Resistance: 24,000 psychological mark.

- Bank Nifty: Held 54,116 support. Break below could trigger stop-losses toward 53,500.

- Nifty 500: RSI at 48—neutral but weakening. Volume ratio 1.2x—selling not panicked but persistent.

6. AI Signals — BUY / HOLD / SELL

| Stock | Signal | Reason |

|---|---|---|

| TCS | HOLD | Above 200-DMA, RSI 62, but IT sector volume thin; await confirmation |

| Infosys | HOLD | Rupee tailwind supportive, RSI 59, but sector rotation risk high |

| HDFC Bank | HOLD | Below 50-DMA, RSI 44, mild oversold but no volume confirmation yet |

| Vedanta | SELL | RSI 32, below both DMAs, volume spike 1.8x on down move |

| ONGC | SELL | RSI 29, fresh lows, Death Cross imminent |

| Suzlon Energy | SELL | RSI cooling from 74 to 68, volume 2.3x avg—profit-booking in force |

| Persistent Systems | HOLD | RSI 71 (overbought), above 50-DMA, but momentum stalling |

| Lupin | HOLD | RSI 46, above 200-DMA, sector rotation risk; watch 50-DMA retest |

| Embassy REIT | BUY | Defensive yield play, RSI 53, above both DMAs, resilient on down day |

| Tata Elxsi | BUY | Bucked trend (+0.3%), RSI 58, volume 1.4x avg, chip tailwinds intact |

| Mazagon Dock | SELL | Volume spike 2.0x, RSI 39, lock-in expiry overhang |

| HAL | HOLD | Strong order book, RSI 47, but defence sector under pressure near-term |

7. Tomorrow’s Setup — Global Cues & Calendar

Global overnight signals:

- US equities: Dow +0.38%, S&P 500 +0.45%, Nasdaq +0.57%—all near record highs. Tech strength (Snowflake, Dollar Tree earnings beats) and soft crude prices supported sentiment.

- Asia: Nikkei 225 surged 2.53% on chipmaker optimism. Hang Seng +0.70%, ASX 200 +1.62%. Risk-on mood intact globally.

- Europe: FTSE 100 +0.03%, DAX -0.06%—mixed, but no major red flags.

- GIFT Nifty: Expect a flat-to-marginally-positive start based on Asian strength, but domestic headwinds (VIX +8%, lock-in fears) will cap upside.

Commodities:

- Crude: Brent $90.96 (-2.93%), WTI $87.32 (-1.78%)—supportive for importers, but sentiment around demand weakness lingers.

- Gold: $4,561.8 (+1.39%)—safe-haven bid rising, watch for FII flows into gold ETFs.

- USD/INR: 94.99 (-1.10%)—rupee strength continues; IT and Pharma exporters remain in focus.

Key levels to watch Monday:

- Nifty 50: Support at 23,480 (today’s low), resistance at 23,890 (50-DMA). A break below 23,480 could trigger 23,200. Upside capped at 24,000 unless global cues turn sharply positive.

- Bank Nifty: Support 54,116, resistance 54,800. Sustained hold above 54,000 crucial.

- Nifty IT: Watch 29,250 resistance—sector needs follow-through buying to sustain momentum.

Calendar watch:

- No major domestic data releases Monday. Focus shifts to Reliance AGM on June 19 (Jio IPO update expected) and ongoing Q4 earnings trickle (Cummins, Gillette India, Senco Gold reported today—details sparse but worth tracking for sector cues).

- Globally, US Memorial Day weekend means thin volumes Monday—low liquidity can amplify moves.

8. The Honest Take

For long-term investors: Days like today are noise, not signal. The rupee strengthened, crude fell, corporate earnings (brokers, exchanges, even Richfield Finance’s 149% revenue jump) remain robust. Yet the market sold off. Why? Positioning fatigue, lock-in expirations, and the eternal Indian market habit of ignoring good news when it arrives. If you own quality franchises—HDFC Bank above Rs 1,600, TCS near Rs 3,400, Embassy REIT with 7%+ yields—today’s 1.5% dip is a rounding error over a five-year horizon. The midcap surge to record highs (even if intraday) signals rotation is alive. Stay patient. Stay invested.

For active traders: This was a distribution day disguised as consolidation. VIX up 8%, breadth negative, and volume spikes on losers (Suzlon, Vedanta, Mazagon)—all flashing yellow. The technical picture isn’t broken yet (Nifty above 23,480, Bank Nifty above 54,000), but we’re one headline away from a flush. If Monday opens weak, 23,200 on Nifty becomes the line in the sand. Conversely, a gap-up on Asian strength could trap late shorts—keep stops tight. The IT pocket (TCS, Persistent) remains the only sector with upside momentum. Everything else is either consolidating or cracking.

“The stock market is designed to transfer money from the Active to the Patient.” — Warren Buffett

Disclaimer: This blog is for informational and educational purposes only. It is not investment advice. All figures cited reflect publicly reported data for the trading session indicated. Markets are subject to risk; please consult a SEBI-registered advisor before acting on any view expressed here.