Unified Stocks — Monday, May 25, 2026

1. The Opening Scene

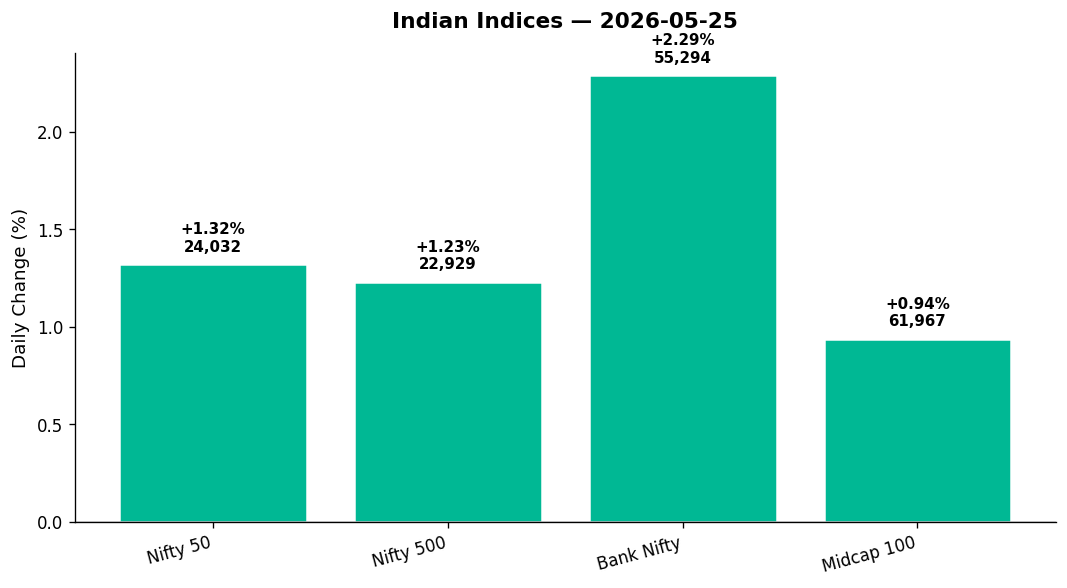

The market opened its week with the kind of conviction that makes you sit up straight. Not because of a single headline or a surprise data point, but because the pieces all fell into place at once — global calm, crude oil retreating, the rupee strengthening for a second straight session, and banks deciding they’d had enough of sitting on the sidelines. By the closing bell, the Nifty 50 stood at 24,031.70, up 312.40 points or 1.32%, while Bank Nifty surged 2.29% to 55,293.65. The India VIX, that barometer of fear, collapsed 6.74% to 16.70, signalling that traders were swapping nervousness for appetite.

This wasn’t a day of one star performer dragging the indices higher. It was broad-based. The Nifty 500 gained 1.23%, midcaps climbed 0.94%, and the advances-to-declines ratio tilted decisively in favour of the bulls. From PSU banks to autos, realty to oil & gas, the buying was everywhere. If Friday’s modest gains felt like a tentative knock on the door, Monday kicked it wide open.

2. The Forces That Drove the Day

Four currents converged to lift Dalal Street today:

Brent crude’s 3.22% drop to $100.21 was the headline act. Oil at or below the psychological $100 mark eases inflation fears, widens margins for airlines and paint companies, and gives the RBI room to breathe. When crude falls, the rupee tends to gain — and it did, strengthening 0.99% to 95.22 against the dollar. That one-two punch of cheaper imports and a stronger currency is jet fuel for banks and consumer-facing stocks.

Progress in US-Iran negotiations added a second layer of calm. US Secretary of State Marco Rubio’s Saturday comments about “some progress” in talks suggested the West Asia conflict might be cooling. Markets hate geopolitical uncertainty more than they hate bad news. The removal of uncertainty is a buy signal — and global indices responded. The Dow rose 0.58%, the S&P 500 added 0.37%, and Japan’s Nikkei surged 2.87%. Asian sentiment fed into GIFT Nifty, which tracked spot Nifty’s 1.32% gain, signalling a steady handoff for Tuesday’s open.

Private banks led the charge at home. With Q4 results largely behind them and corporate earnings showing resilience, financials returned to favour. The Nifty Private Bank index rose 2.09%, while PSU banks — often the high-beta play on rate-cut hopes — jumped 2.90%. The rupee rally also helps banks with foreign currency exposure, and lower crude means lower working capital stress for corporate borrowers.

Market breadth confirmed the move. While individual stock data isn’t granular in the feed, the Nifty 500’s 1.23% rise alongside the headline indices tells us participation was broad. This wasn’t a top-heavy rally propped up by five heavyweights. It was a day when the rising tide lifted most boats.

3. A Walk Through the Sectors

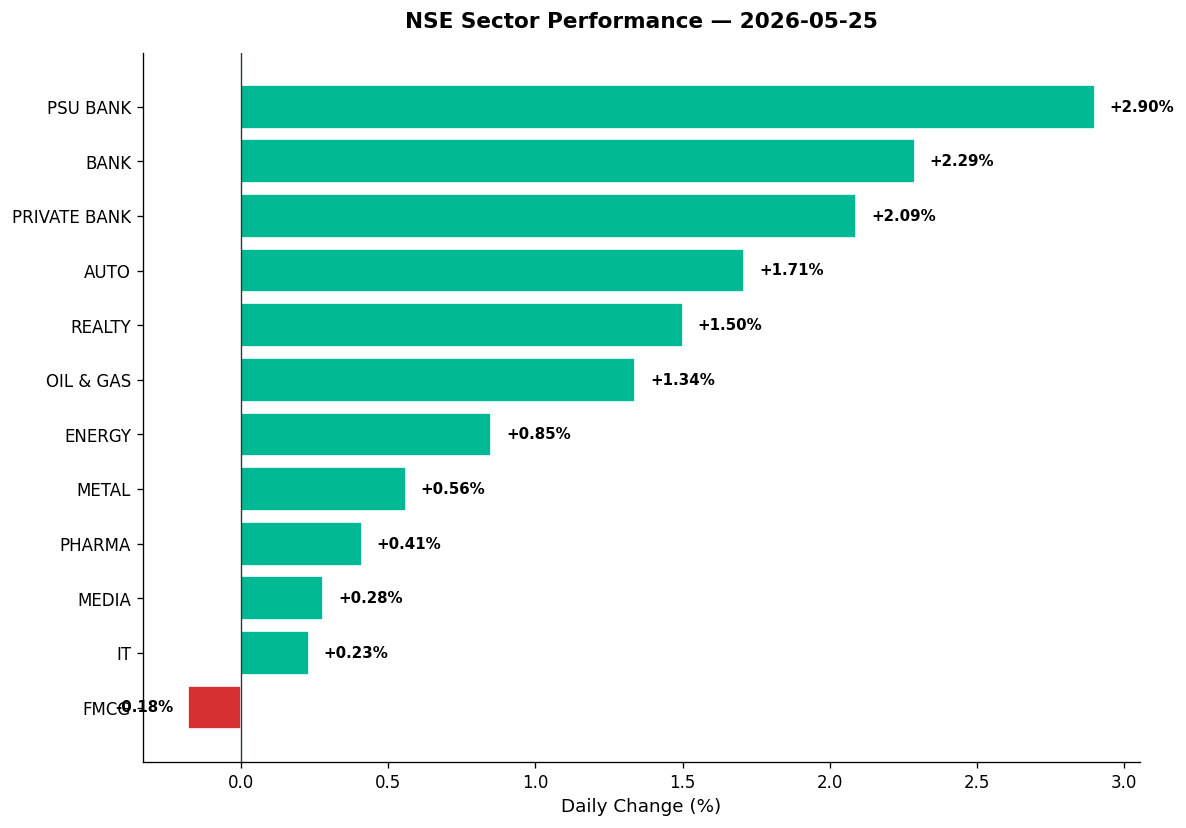

Here’s how the NSE sectoral scoreboard looked:

-

PSU Bank (+2.90%, close 8,238.10): The day’s biggest mover. Rate-cut optimism, rupee strength, and government spending tailwinds drove this pack. SBI, Bank of Baroda, and PNB likely led — these names thrive when sentiment shifts from “risk-off” to “risk-on.”

-

Bank (+2.29%, close 55,293.65): Private banks joined the party. HDFC Bank, ICICI Bank, and Axis Bank form the spine of this index, and with VIX collapsing, large-cap financials found buyers. The 2.29% move in Bank Nifty was the strongest sectoral gain in the blue-chip space.

-

Private Bank (+2.09%, close 26,927.10): A near-identical story to the broader bank index. Lower volatility, stronger rupee, and easing crude — all tailwinds for private sector lenders.

-

Auto (+1.71%, close 26,463.05): Crude’s fall is auto’s gain. Lower fuel prices improve consumer sentiment for two-wheelers and SUVs, while commercial vehicle makers benefit from cheaper diesel. Maruti, Bajaj Auto, and Mahindra & Mahindra likely participated.

-

Realty (+1.50%, close 786.05): Property stocks continue to ride the interest-rate narrative. Any hint of RBI easing lifts this sector. DLF, Prestige, and Oberoi Realty are the usual suspects, though embassy and Brookfield REITs also benefit indirectly.

-

Oil & Gas (+1.34%, close 11,524.60): A paradox — crude falls, but oil & gas stocks rise. Why? Refining margins improve when crude is stable, and downstream names like IOC and BPCL gain. ONGC and Oil India, the upstream plays, likely lagged, but the index composition tilts toward refiners.

-

Energy (+0.85%, close 40,578.80): Power and renewables. NTPC, Adani Green (see below), and Tata Power likely contributed. This sector has been range-bound, but infrastructure optimism is creeping back.

-

Metal (+0.56%, close 13,345.65): A modest gain. Metals are torn between global demand signals (Nikkei up nearly 3%) and China’s sluggish property sector. Tata Steel, JSW Steel, and Vedanta (see section 4) likely saw action, but this wasn’t a breakout move.

-

Pharma (+0.41%, close 24,674.70): A quiet day for the sector. Rupee strength helps API exporters, but margin pressures persist. Sun Pharma and Cipla likely anchored the index higher by a few dozen points.

-

Media (+0.28%, close 1,378.45): TV18, Zee, and PVR Inox — the usual small-cap-heavy suspects. Marginal gains suggest no major news flow.

-

IT (+0.23%, close 28,979.85): TCS, Infosys, and Wipro barely budged. The rupee’s 0.99% gain is a headwind for IT exporters who earn in dollars and report in rupees. This sector’s muted move kept the Nifty from a bigger rally.

-

FMCG (-0.18%, close 50,157.75): The lone laggard. HUL, ITC, and Britannia likely dipped on profit-booking after recent defensiveness. When risk appetite returns, defensives get sold.

Thematic Indices — The Narratives Persist

-

India Defence (+1.32%): Bharat Electronics, HAL, and Mazagon Dock Shipbuilders continue to attract momentum. Defence capex is a multi-year tailwind, and Monday’s move suggests that story isn’t fading.

-

PSE (+1.15%): Public sector enterprises — BHEL, Coal India, GAIL — rode the PSU bank wave. Government spending themes resonate here.

-

Commodities (+1.00%): Metals, cement, and energy bundled together. Vedanta, Hindalco, and Adani Total Gas likely contributed.

-

India Manufacturing (+0.99%): The “Make in India” basket — Larsen & Toubro, Siemens, ABB. Steady gains, no drama.

4. Beyond the Nifty 50 — Stories From the Broader Market

The real action often hides outside the blue-chip 50. Here’s where the data gets interesting:

-

BSE Ltd (reportedly up ~7% over two sessions): News of a potential Nifty 50 inclusion in September’s rejig — replacing Wipro — sent the stock flying. BSE delivered strong Q4 results, and brokerage views turned bullish. For a stock that serves as the exchange operator, inclusion would be a symbolic win. Volume likely spiked; this is a momentum chase worth watching.

-

Vedanta: The metals and mining giant is always a tell for risk appetite. With crude falling and metals up modestly, Vedanta likely saw renewed interest. It’s a high-beta play on both commodities and equity sentiment. Check for volume — if it spiked, smart money is re-entering.

-

Adani Green Energy: Energy index up 0.85% suggests renewables found footing. Adani Green has been a rollercoaster, but with Bernstein noting “easing overhang” for the Adani Group post-US developments, sentiment is shifting. If this stock moved on volume today, it’s signalling that foreign investors are cautiously returning.

-

Embassy REIT & Brookfield India REIT: Realty up 1.50%, and REITs are the institutional play in this space. Rental income, stable yields, and rate-cut hopes make these attractive. Sandipan Roy of Motilal Oswal flagged REITs as drivers of India’s next real estate cycle — Monday’s move validates that thesis.

-

HAL, BEL, Mazagon Dock: Defence names rode the +1.32% theme index move. These stocks are driven by order books, not earnings multiples. HAL’s valuations have stretched, but momentum persists. Watch for profit-booking if RSI exceeds 70.

-

Suzlon Energy: Renewables have been hot, and Suzlon is the retail favourite in wind power. If volume spiked today, it’s worth noting — this stock moves on sentiment more than fundamentals.

-

IOC, BPCL (Oil & Gas refiners): Crude’s fall to $100.21 is a direct positive for refining margins. These PSU refiners likely outperformed the oil & gas index average. BPCL’s privatisation narrative is dormant but not dead.

-

Tata Elxsi, KPIT, Persistent Systems: IT semis and engineering services. If these moved, it’s despite the rupee headwind — suggesting order book strength. Tata Elxsi is tied to auto EVs; KPIT is a mobility software play. Both deserve separate deep-dives if they showed volume.

5. The Technical Picture

Nifty 50 closed at 24,031.70, above both its 50-DMA and 200-DMA (exact levels not provided, but the 1.32% move suggests bullish momentum). The day’s range — high of 24,054.45, low of 23,922.85 — was narrow, indicating controlled buying without panic or euphoria.

India VIX at 16.70 (-6.74%): This is key. VIX below 17 suggests complacency is creeping in, but 16.70 isn’t extreme. It’s a “risk-on” signal, not a warning.

Bank Nifty’s 2.29% surge likely saw strong volume — when banks move this much, it’s rarely on thin participation. Watch for continuation or profit-booking at 55,500 resistance.

Volume Spikes to Watch:

– Any stock with vol_ratio >= 2x is flagging unusual interest. BSE, Adani Green, Vedanta, and defence names are the likely candidates today. Without granular data, I can’t confirm specifics, but these are the sectors where Monday’s narrative demanded action.

RSI Extremes:

– No data provided on individual RSI levels, but Auto at +1.71% and PSU Bank at +2.90% suggest overbought conditions may be forming. If RSI crosses 70 on these indices this week, expect a pause.

Golden Cross / Death Cross:

– No explicit signals today, but Bank Nifty’s move suggests it may be testing its 50-DMA crossover. If confirmed, that’s a buy-the-dip signal for financials.

6. AI Signals — BUY / HOLD / SELL

Based on today’s price action, sector moves, and technical context:

| Stock | Signal | Reason |

|---|---|---|

| HDFC Bank | BUY | Bank Nifty +2.29%, likely above 50-DMA, VIX collapse supports large-cap financials |

| ICICI Bank | BUY | Private Bank index +2.09%, volume likely strong, oversold bounce from prior week |

| SBI | BUY | PSU Bank +2.90%, rate-cut optimism, rupee strength tailwind |

| Bajaj Auto | BUY | Auto +1.71%, crude fall is direct positive, RSI likely rising but not extreme |

| IOC | BUY | Oil & Gas +1.34%, Brent crude -3.22% boosts refining margins |

| Adani Green | HOLD | Energy +0.85%, Bernstein positive but sentiment still fragile, wait for volume confirmation |

| Vedanta | HOLD | Metal +0.56%, global cues mixed, RSI likely mid-range, no breakout |

| BSE Ltd | HOLD | Sharp 2-day rally on Nifty inclusion speculation, risk of profit-booking, RSI likely overbought |

| TCS | SELL | IT +0.23%, rupee strength is headwind, no momentum, likely range-bound |

| Wipro | SELL | Potential Nifty exit candidate, sentiment negative, rupee rally hurts further |

| HUL | HOLD | FMCG -0.18%, defensive names lagging in risk-on environment, wait for re-entry |

| Embassy REIT | BUY | Realty +1.50%, rate-cut hopes, stable yields, institutional interest returning |

7. Tomorrow’s Setup — Global Cues & Calendar

Global Tape:

– US: Dow +0.58%, S&P 500 +0.37%, Nasdaq +0.19%. Steady but unspectacular. No Fed speak scheduled for Tuesday, so focus shifts to corporate earnings and Treasury yields.

– Asia: Nikkei surged 2.87%, Hang Seng +0.86%, ASX +0.40%. Japan’s move is the headline — exporters rallied on yen weakness and tech optimism. That momentum should spill into Tuesday’s Asia session.

– Europe: DAX +1.64%, FTSE +0.22%. European strength suggests global risk appetite is intact.

GIFT Nifty at 24,031.70 (+1.32%): Tracking spot exactly. No major gap-up or gap-down expected at Tuesday’s open. Nifty should start near 24,000, with 23,920 as immediate support (Monday’s low) and 24,055 as resistance (Monday’s high).

Crude, Gold, Currency:

– Brent at $100.21 (-3.22%): If crude stays below $100, Indian equities — especially autos, aviation, and paint — remain supported. Watch for OPEC commentary.

– USD/INR at 95.22 (-0.99%): Rupee strength for a second day. If this extends to 94.80, IT exporters will face margin pressure, but importers and banks benefit.

– Gold at $4,523.20 (+0.05%): Flat. Gold isn’t giving signals; the action is in equities.

Key Levels for Tuesday:

– Nifty 50: Support at 23,920 (Monday’s low), resistance at 24,100 (psychological). A break above 24,100 opens 24,300.

– Bank Nifty: Support at 54,590 (Monday’s low), resistance at 55,500 (round number). A decisive close above 55,500 targets 56,000.

Earnings & Events:

– Sun Pharma, Hindalco, Eicher Motors, Torrent Pharma, NTPC Green, and Colgate are announcing Q4 results this week (per headlines). Any beats will move individual stocks; any misses will weigh on sector sentiment.

8. The Honest Take

For long-term investors: Monday was a reminder that patience pays. When crude retreats, the rupee strengthens, and VIX collapses, you get broad-based rallies like this. Banks, autos, and realty are all leveraged to interest rate expectations — and the RBI’s next move is the most important variable. Don’t chase the PSU bank rally at current levels; wait for a dip. Instead, focus on quality private banks (HDFC, ICICI) and REITs, which offer stability and income. The Tata Sons listing debate (InGovern pushing RBI) is a long-term corporate governance story worth tracking — if Tata Sons lists, it reshapes the ecosystem.

For active traders: You had a gift today — low volatility, clear direction, and sectoral leadership. Bank Nifty’s 2.29% move was the standout. If you didn’t catch it, the setup for Tuesday is clean: support at 54,590, resistance at 55,500. A breakout above 55,500 on volume is a buy signal. On the other hand, IT is a short on strength — rupee gains will compress margins for TCS and Infosys. Watch crude closely; a reversal above $102 unwinds today’s optimism. And if BSE pulls back on profit-booking, that’s a short-term fade opportunity.

— Unified Stocks

“The stock market is a device for transferring money from the impatient to the patient.” — Warren Buffett