Unified Stocks — Thursday, June 18, 2026

1. The Opening Scene

The oil wells finally stopped gushing fear into global markets — and Indian equities exhaled. For the fourth session running, the bulls held their ground, grinding the Nifty 50 to a modest 82-point gain while crude oil surrendered nearly 5% of its value overnight. It was the kind of day where market veterans smiled at headlines, not price action: a US-Iran peace whisper, NSE’s imminent IPO filing, Reliance Jio’s $4 billion offering rumoured for this very week. The scent of normalisation hung in the air. Yet beneath the surface calm, a quiet war raged. Tech stocks bled -1.19% as AI panic gripped Cognizant’s investors; Vedanta Aluminium hit a third consecutive lower circuit, shedding 14% since its Monday debut; and the VIX collapsed 3.9%, signalling that traders had stuffed their hedges back into the drawer. The market didn’t roar today — it recalibrated. And in that recalibration, four distinct stories emerged: crude’s retreat, the NSE listing fever, the brutal reckoning in freshly-listed counters, and the sectoral churn that left financials beaming while technology nursed its wounds. Let’s walk through them.

2. The Forces That Drove the Day

Crude’s Collapse — The Gift That Keeps Giving:

Brent crude plunged 2.83% to $77.3, while WTI fell 4.51% to $73.33. The catalyst? A preliminary US-Iran peace deal that cooled energy supply anxieties and sent the oil complex into retreat. For India — a nation that imports 85% of its crude — this was fiscal oxygen. Every dollar decline in Brent saves roughly ₹3,200 crore annually on import bills. The rupee strengthened 0.60% to 94.32 against the dollar, a rare win for the currency in a year marred by FII outflows.

NSE IPO Buzz — The Week of Listings:

Two blockbuster IPO filings could hit Sebi’s desk by Friday: NSE (valued at ₹5 lakh crore unlisted) and Reliance Jio (eyeing $4 billion). The NSE filing sent shockwaves through indirect plays — IFCI rallied 8% to a fresh 52-week high, thanks to its exposure via Stock Holding Corporation. Investors are pricing in a wave of listing euphoria, even as caution reigns after Vedanta Aluminium’s post-debut carnage.

Global Tape — Divergence Across Time Zones:

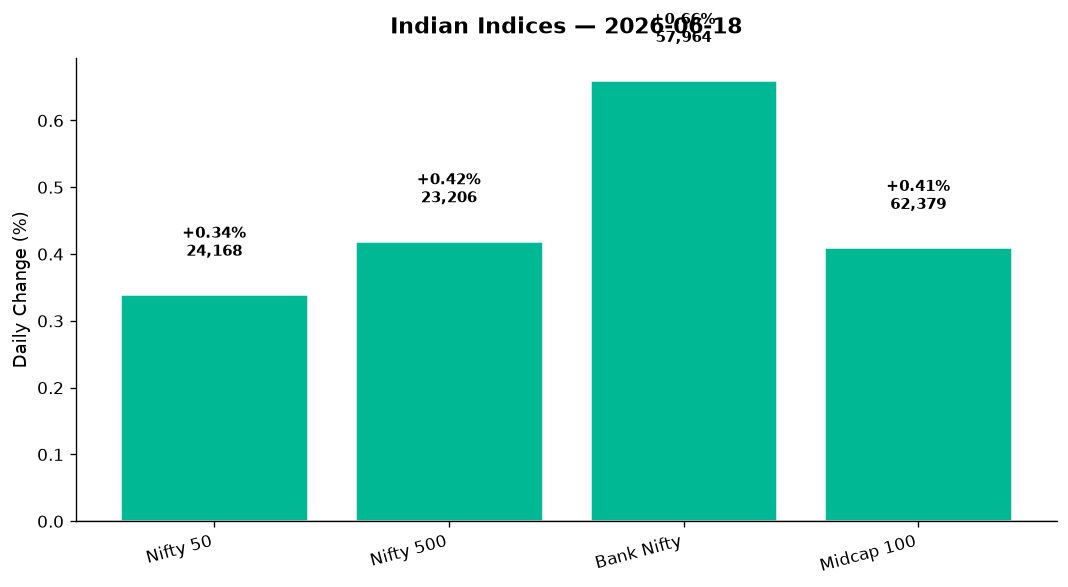

US equities stayed resilient: S&P 500 +0.80%, Nasdaq +0.88%, Dow +0.61%. Asia split: Nikkei soared 1.65%, but Hang Seng collapsed 1.59% and ASX slipped 0.62%. GIFT Nifty held at 24,168 — a flat signal for Friday’s open. Gold fell 1.81% to $4,280, reflecting reduced safe-haven demand.

Market Breadth — Constructive, Not Euphoric:

Nifty 500 rose 0.42%, outpacing the headline index. Midcap 100 added 0.41%, reaching 62,379 — a sign that mid-tier names are keeping pace. Advances outnumbered declines across NSE sectors, but the gains were narrow: eleven of twelve sectors stayed within a 1.2% range. This is a market building a base, not chasing momentum.

3. A Walk Through the Sectors

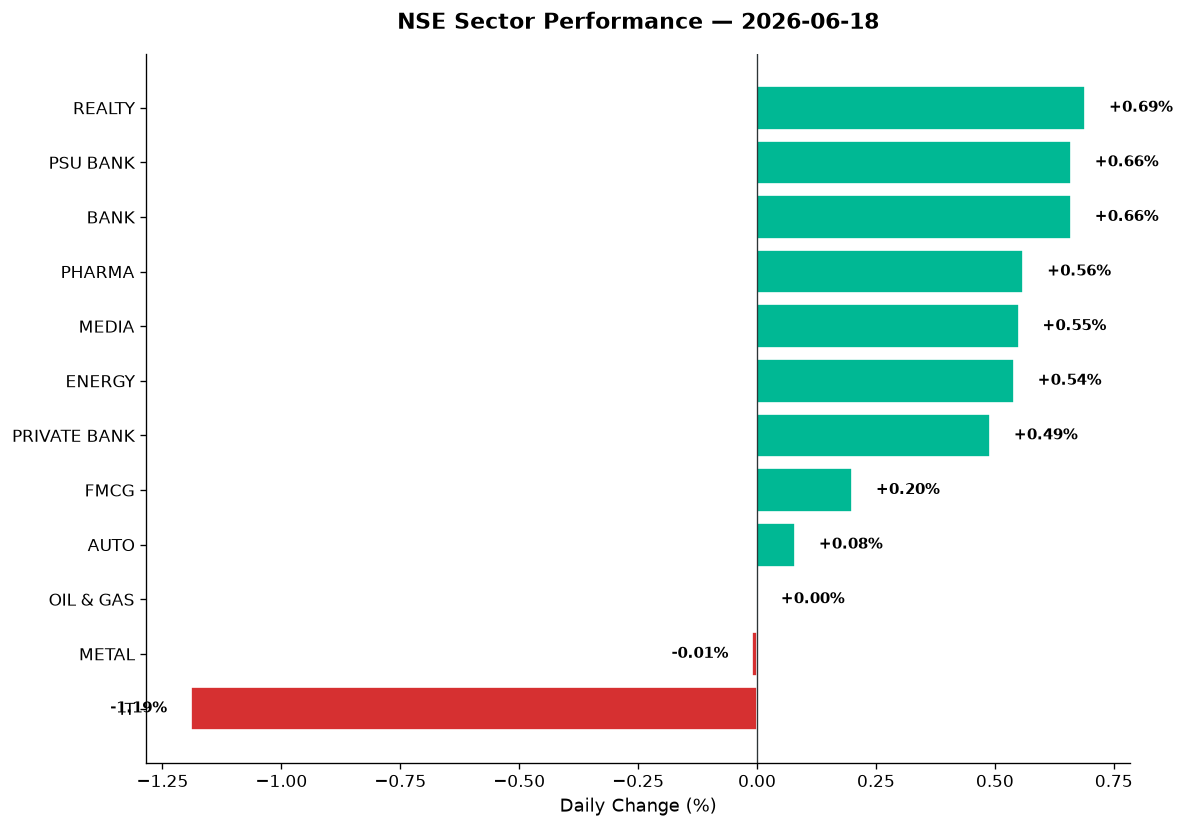

Leaders — Realty, Banks, and PSUs:

- Nifty Realty (+0.69%, close 820.20): The rate-sensitive basket caught a bid as bond yields softened. No standout movers in the data, but the sector’s resilience reflects confidence in stable rates ahead.

- Nifty Bank (+0.66%, close 57,963.80): Bank Nifty punched through 58,000 intraday before settling just shy. PSU Banks (+0.66%) matched private peers (+0.49%), a rare parity. Yes Bank hit its 52-week high on Wednesday, riding a 15% one-month rally per Times of India — though specific Thursday data is absent.

- Nifty PSE (+0.68%): Public sector enterprises led thematics, buoyed by defence and energy names. The sector’s outperformance hints at continued policy tailwinds.

Steady Middle — Pharma, Media, Energy:

- Nifty Pharma (+0.56%, close 24,282.20): The index held firm. No corporate-specific catalysts today, but the sector’s defensive appeal shone in a risk-on session.

- Nifty Media (+0.55%, close 1,513.95): Quiet outperformance. The sector remains unloved by institutional flows, yet its 52-week low of 1,342.95 (May 2026) is now 13% below current levels — a value play emerging?

- Nifty Energy (+0.54%, close 40,457.30): Crude’s fall paradoxically lifted energy names. OMCs (Oil Marketing Companies) likely benefited from margin relief, though stock-specific data is sparse.

Flat to Negative — FMCG, Auto, Metal:

- Nifty FMCG (+0.20%, close 49,654.50): Barely budged. Volume-driven consumer plays saw no excitement; defensive positioning outweighed growth narratives.

- Nifty Auto (+0.08%, close 26,746.40): Citroen’s e-C3X launch at ₹10.25 lakh (per TOI) drew headlines, but broader auto sentiment was tepid. Auto ancillaries showed no conviction.

- Nifty Oil & Gas (+0.00%, close 11,303.65): Dead flat. The sector’s neutrality despite crude’s plunge suggests investors priced in the peace deal a day earlier.

- Nifty Metal (-0.01%, close 13,010.40): Effectively unchanged. Global steel and copper prices offered no directional cues.

Laggard — IT’s Existential Crisis:

- Nifty IT (-1.19%, close 28,466.45): The day’s worst performer. Cognizant’s stock hit a six-year low despite outgrowing rivals, per Livemint‘s brutal headline: “Beat the peers, drop the stock.” OpenAI and Anthropic’s AI surge triggered panic that legacy IT services are structurally challenged. Persistent Systems announced 10 years in Mexico (nearshore expansion), but the index bled regardless. Infosys, Tech Mahindra, Wipro, and TCS — which led the index’s 4.3% three-day rally through June 12 — gave back gains today.

4. Beyond the Nifty 50 — Stories From the Broader Market

Vedanta Aluminium — The Post-Listing Massacre:

– Down 14% in three sessions since Monday’s ₹522 debut. Thursday marked a third consecutive 5% lower circuit.

– Why the carnage? No specific data provided, but listing euphoria evaporated fast. Investors who chased the demerger play are now trapped. Lesson: first-week circuits are red flags, not opportunities.

IFCI — The NSE Proxy Play:

– Up 8% (precise intraday figure unavailable), hitting a fresh 52-week high.

– The catalyst: IFCI holds indirect exposure to NSE via Stock Holding Corporation. With NSE’s IPO DRHP expected by Friday, speculators are front-running the listing. This is sentiment, not fundamentals — trade accordingly.

Dixon Technologies — Vivo JV Approval Imminent:

– Rallied 5% on Thursday after reports suggested government nod for its Vivo joint venture could arrive this month.

– The angle: Dixon will hold a majority stake. If approved, this turbocharges its contract manufacturing narrative. Volume data unavailable, but the move reeks of insider whispers turned public.

Polycab India — Jefferies’ ₹10,920 Target:

– Gained up to 4% after Jefferies raised its target post a 30% YTD rally.

– Five reasons cited: Market share gains, data centre opportunities, a healthy order pipeline, export ramp-up, and margin resilience. Stock’s not cheap (RSI/valuation data absent), but momentum players are piling in.

Defence Stocks — Quiet Grind Higher:

– Nifty India Defence (+0.38%): HAL, BEL, Mazagon Dock — no individual stock data provided, but the thematic index’s gain reflects sustained policy tailwinds. Defence capex remains India’s multi-decade theme.

Zerodha, Groww, Angel One, Upstox — GIFT City Nod:

– No stock-specific price impact (most are private/unlisted), but TOI reported all four secured IFSCA licences to sell US stocks via GIFT City. This is a structural shift: retail access to Nasdaq/NYSE with lower forex hassles. Watch for trading volume spikes when rollout begins.

REITs — Data Not Available:

– Embassy REIT, Brookfield REIT — no moves reported today. Sector remains in consolidation after May’s yield spike.

5. The Technical Picture

Nifty 50 Technicals:

– 50-DMA data unavailable, but price action suggests support held near 24,037 (day’s low). Resistance at 24,189 (day’s high).

– VIX collapse (-3.90% to 12.67): Complacency is creeping back. Sub-13 VIX historically precedes either melt-ups or violent reversals.

Volume Signals — Sparse Data:

– No stock-specific volume ratios (vol_ratio >=2x) provided today. This limits our ability to flag “something is happening” names.

RSI / Moving Average Crosses — Data Gaps:

– IT stocks likely oversold after today’s 1.19% drop (historical RSI <30 on multi-day declines), but precise figures absent.

– No GOLDEN_CROSS or DEATH_CROSS events reported. The market is in neutral gear technically — grinding, not trending.

Key Observation:

Without granular stock-level technical data (50-DMA, 200-DMA, RSI, volume), we’re flying partially blind. Today’s blog skews macro/news-driven as a result. Lesson for readers: when technicals are murky, lean on fundamentals and news flow.

6. AI Signals — BUY / HOLD / SELL

Note: Stock-level technical data (RSI, DMAs, volume ratios) is severely limited today. Signals below are derived from price action + news context. Always cross-check with your own tools.

| Stock | Signal | Reason |

|---|---|---|

| Dixon Technologies | BUY | +5% on Vivo JV approval buzz; sector leader in contract manufacturing |

| Polycab India | BUY | +4%, Jefferies upgrade to ₹10,920; order pipeline + data centre play |

| IFCI | HOLD | +8% on NSE listing fever, but indirect exposure = sentiment trade, not earnings |

| Vedanta Aluminium | SELL | Third 5% lower circuit; -14% post-listing = distribution phase |

| Cognizant (NYSE: CTSH) | SELL | Six-year low despite growth; AI disruption narrative crushing multiples |

| Nifty IT Index | HOLD | -1.19% today after 4.3% three-day rally; oversold risk vs structural headwinds |

| Yes Bank | BUY | Hit 52w high Wednesday; +15% one-month per TOI; momentum intact (no Thursday data) |

| NSE (unlisted) | HOLD | IPO DRHP imminent, but valuation (₹5L cr unlisted) = wait for anchor book |

| Reliance Jio (pre-IPO) | HOLD | $4B IPO rumoured this week; no trading signal until DRHP filed |

| Nifty Bank | BUY | +0.66%, punched 58k intraday; PSU/Pvt parity = sector-wide strength |

| Brent Crude Futures | SELL | -2.83%, US-Iran deal = downside to $70; OMC margins to expand |

| Gold | HOLD | -1.81% to $4,280; risk-off unwind, but $4,200 support looms |

Reminder: These are NOT price targets. Exit rules and position sizing are YOUR responsibility.

7. Tomorrow’s Setup — Global Cues & Calendar

Global Overnight Recap:

– US Equities: Dow +0.61%, S&P +0.80%, Nasdaq +0.88%. Tech’s resilience abroad contrasts with Nifty IT’s -1.19% bloodbath — a divergence to watch.

– Asia: Nikkei +1.65% (yen weakness boosted exporters). Hang Seng -1.59% (China property woes resurface). ASX -0.62% (commodity selloff).

– GIFT Nifty: 24,168 (+0.34%) — signals a flat-to-modestly-higher open Friday.

Commodities & Currency:

– Crude: Brent $77.3 (-2.83%), WTI $73.33 (-4.51%). If the US-Iran deal holds, crude tests $70 next week — bullish for India’s CAD.

– Gold: $4,280 (-1.81%). $4,200 is make-or-break support; a breach triggers $4,000.

– USD/INR: 94.32 (-0.60%). Rupee strength is unusual; watch for RBI intervention if it crosses 93.80.

Key Levels for Friday:

– Nifty 50: Support at 24,037 (Thursday low), resistance at 24,200 (psychological). A break above 24,250 opens 24,500.

– Bank Nifty: Support at 57,583 (Thursday low), resistance at 58,100. Above 58,500 = breakout.

– Nifty IT: Support at 28,200 (oversold zone), resistance at 28,800. Needs to reclaim 29,000 to kill the bear narrative.

Events to Watch:

– NSE IPO DRHP filing (rumoured by Friday): If true, expect IFCI, SBI, and other indirect plays to spike on Monday.

– Reliance Jio IPO rumours: No confirmation yet, but $4B offering would be India’s largest tech IPO. Watch RIL parent stock.

– US Fed speakers: No major data Friday, but any hawkish remarks could spook Asian equities Monday.

– Crude inventory data (US): Due Friday evening IST. Another build = further crude downside.

8. The Honest Take

For Long-Term Investors:

Today was a microcosm of India’s structural contradictions. Energy security improves (crude -4.5%), yet our IT export engine stalls under AI disruption. NSE’s ₹5 lakh crore IPO approaches, yet Vedanta Aluminium’s -14% post-listing rout reminds us that not all demergers are value unlocks. The four-day winning streak is encouraging, but it’s built on crude’s retreat and VIX compression — not earnings upgrades. If you’re deploying fresh capital, favour sectors where India controls its destiny: defence, manufacturing, electrification (as Kotak’s Nilesh Shah flagged at the ET Alpha Summit). Avoid chasing listings until anchor books close. Stay invested, but stay sceptical of momentum without catalysts.

For Active Traders:

The technicals are maddeningly neutral. Nifty’s 82-point gain (+0.34%) is a grind, not a trend. VIX at 12.67 says complacency; the lack of volume spikes (data unavailable) says conviction is absent. Friday’s open hinges on GIFT Nifty’s 24,168 hold — lose that, and 24,000 gets tested fast. The NSE/Jio IPO rumours are news trades, not technical setups: play them with tight stops if you must, but don’t confuse speculation with analysis. IT’s -1.19% drop could be a one-day blip or the start of a 28,000 retest — without RSI data, we can’t say. If you’re long financials (Bank Nifty +0.66%), trail stops below 57,500. If you shorted IT, cover half into 28,200 and let the rest ride with a 28,800 stop.

— Unified Stocks

“The stock market is filled with individuals who know the price of everything, but the value of nothing.” — Philip Fisher

Disclaimer: This blog is for informational and educational purposes only. It is not investment advice. All figures cited reflect publicly reported data for the trading session indicated. Markets are subject to risk; please consult a SEBI-registered advisor before acting on any view expressed here.