Unified Stocks — Tuesday, June 16, 2026

1. The Opening Scene

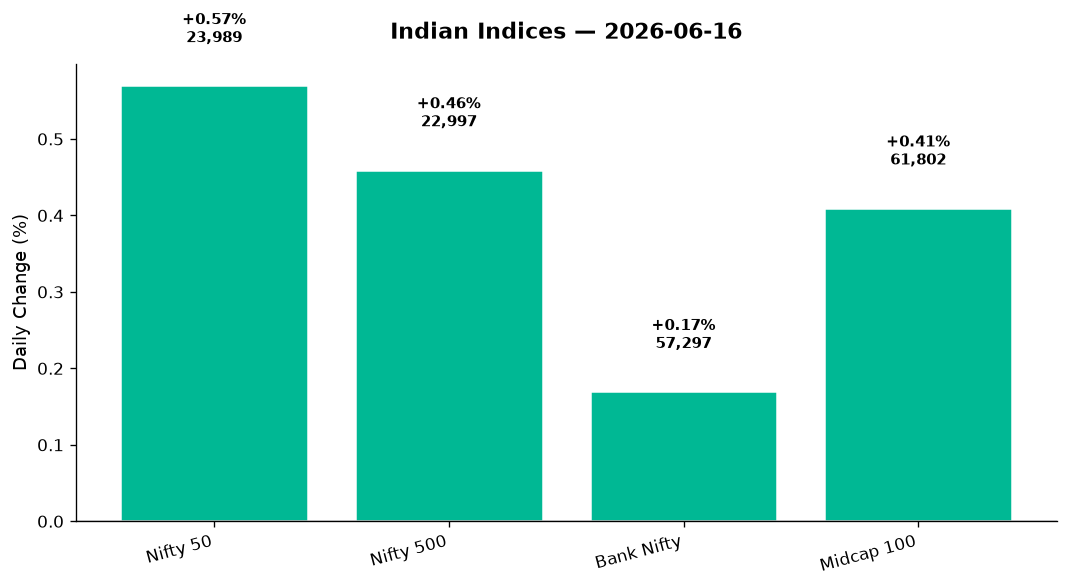

Peace — even tentative, even partial — moves mountains. Or in this case, moves crude oil, currencies, and trillion-rupee indices. When Washington and Tehran announced an interim framework to dial down Middle East tensions and reopen the Strait of Hormuz, traders in Mumbai didn’t wait for the fine print. They bought everything from banks to software exporters, from real estate to energy majors. By mid-morning, the Nifty 50 had crossed 24,000 for a fleeting moment, a psychological peak not seen in weeks. The rally wasn’t uniform — metals buckled, auto stumbled, PSU banks hesitated — but the broader tape was green, and that’s what mattered. India VIX, the market’s fear gauge, collapsed 6.89% to 13.36, its lowest reading in a month. When volatility dies, conviction returns. And Tuesday’s session was nothing if not a vote of confidence that lower oil, a stronger rupee, and the possibility of sustained FII inflows could finally end the two-year drought that’s kept institutional money on the sidelines. The Nifty 50 closed at 23,989.15, up 135.25 points (+0.57%). The Sensex climbed 736 points. Bank Nifty crawled higher by 0.17%, but the real story was in the sectors that had been waiting for this moment: realty, IT, FMCG, energy — all surged. The question now is whether this is a one-day sugar rush or the beginning of a structural shift. Let’s walk through the evidence.

2. The Forces That Drove the Day

Crude’s Collapse, Rupee’s Rise

– Brent crude fell 4.39% to $79.52. WTI crude plunged 6.14% to $75.79. For an import-dependent economy like India, this was a gift. Lower oil means lower inflation, a narrower current account deficit, and less pressure on the rupee. USD/INR dropped 0.59% to 94.55, giving the Reserve Bank of India breathing room and exporters a headache. The immediate macro read: if crude stays here, the FY27 inflation outlook improves, interest rate cut expectations firm up, and equity multiples can re-rate. That’s the narrative the bulls are running with.

US-Iran Framework Boosts Global Risk Appetite

– Wall Street had already priced in optimism by Monday’s close: Dow, S&P 500, and Nasdaq all surged. Asian futures followed. The logic was simple: less Middle East risk = less oil volatility = better for global growth. Indian markets opened on that tailwind. GIFT Nifty pointed to a gap-up, and the index delivered. But note the caution: by afternoon, the Nifty had pared gains. Profit-takers emerged near 24,000. The final close was +0.57%, respectable but not euphoric. This suggests sceptics still outnumber believers.

FII Short-Covering and Domestic SIP Flows

– The Times of India cited analysts expecting FII short-covering after months of net selling. The rupee’s strength and lower crude are classic triggers for foreign money to return. Meanwhile, domestic mutual funds continue their SIP-driven buying — a steady bid under the market. The Nifty 500 gained 0.46%, and the Midcap 100 rose 0.41%, showing breadth wasn’t limited to large-caps. Advances likely outnumbered declines across the broader universe, though the market wasn’t universally strong.

GIC Disinvestment, Sebi ETF Reforms, NSE New Indices

– The government announced an OFS for up to 5% in General Insurance Corporation, starting June 16 for non-retail and June 17 for retail. Floor price details awaited. Separately, Sebi revamped ETF trading rules, introducing dynamic price bands from September — a move to improve price discovery. NSE Indices launched 11 new sectoral benchmarks, including Nifty Power and Nifty Hospitals, taking total sectoral indices to 34. These are plumbing changes, but they matter: deeper indices = more passive flows = more predictable liquidity for specific sectors.

3. A Walk Through the Sectors

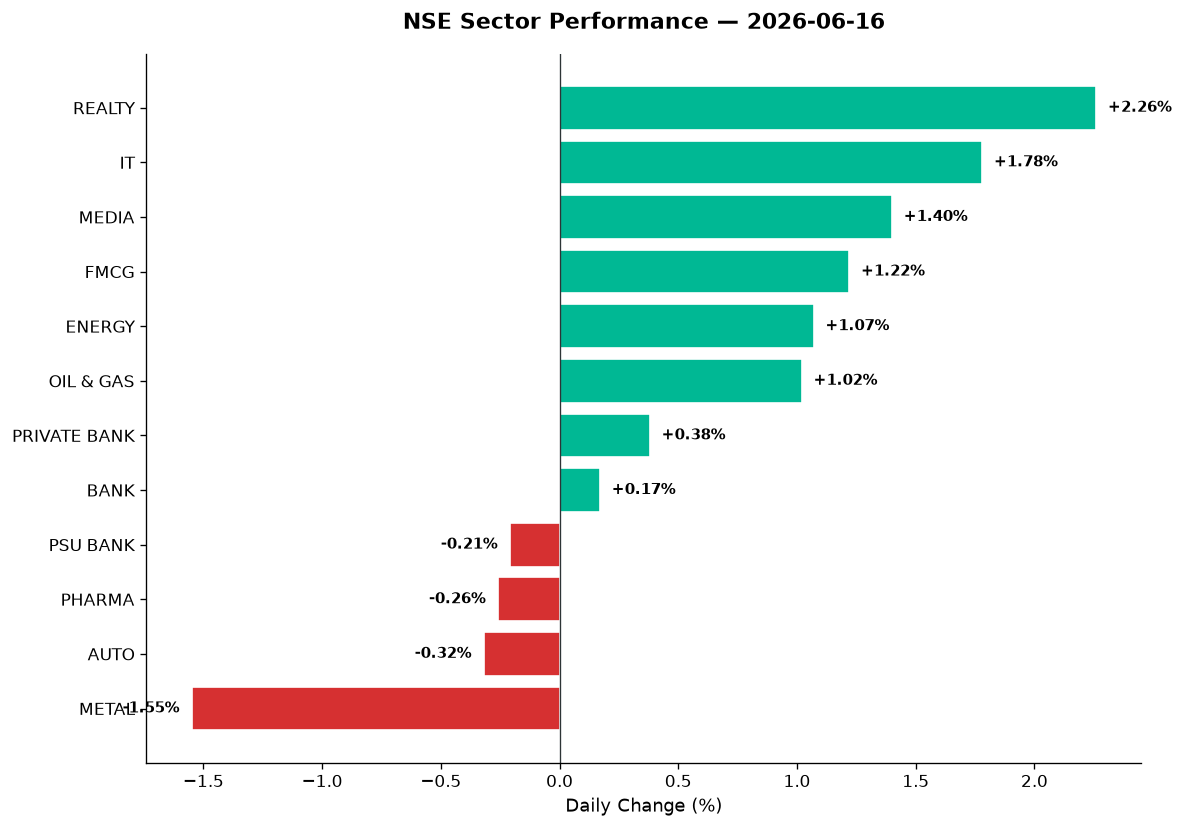

The Leaders — Realty, IT, Media, FMCG

-

Nifty Realty (+2.26% to 818.10): The real estate pack led the charge. Lower interest rate expectations (courtesy of falling crude) and renewed hopes for urban housing demand sent the index soaring. DLF, Godrej Properties, Prestige Estates, Oberoi Realty — all likely contributed. Realty’s been beaten down for quarters; this was a relief rally. Volume and RSI data would confirm if this has legs.

-

Nifty IT (+1.78% to 28,568.10): Software exporters loved the rupee’s move. A weaker dollar-rupee rate means better realisations for IT services firms. TCS, Infosys, Wipro, HCL Tech, Tech Mahindra — the usual suspects. The sector’s been consolidating for weeks; today’s jump suggests buyers are re-entering on valuation. No specific stock-level data here, but the 1.78% gain is the largest in the sectoral pack.

-

Nifty Media (+1.40% to 1,506.30): Advertising-linked names rallied, perhaps on broader risk-on sentiment. Zee Entertainment, TV18, Hathway, PVR Inox — small-cap media names often spike on macro optimism. Data not granular, but the sector’s been dormant; any sign of life is notable.

-

Nifty FMCG (+1.22% to 49,642.40): Consumer staples don’t usually lead rallies, but lower crude = lower input costs = margin expansion. HUL, ITC, Nestle, Britannia, Dabur — all defensive plays that attract money when macro clouds part. The 1.22% gain is solid for a sector that moves in single digits most days.

The Steady Middle — Energy, Oil & Gas, Private Banks, Financials

-

Nifty Energy (+1.07% to 39,915.40): NTPC, Power Grid, Tata Power, Adani Power — power utilities rose on the same lower-crude logic. India’s electricity demand is surging; cheaper fuel costs help margins. The sector’s also in the NSE’s new thematic indices (Nifty Power launching soon), so passive flows may follow.

-

Nifty Oil & Gas (+1.02% to 11,294.60): Refining and marketing companies like Reliance, IOC, BPCL, HPCL saw mixed action. Lower crude is a double-edged sword: good for OMCs (marketing margins improve), bad for upstream explorers (ONGC, Oil India). The net +1.02% suggests marketing won today.

-

Nifty Private Bank (+0.38% to 27,916.90): HDFC Bank, ICICI Bank, Axis Bank, Kotak Mahindra crept higher. The 0.38% gain is modest but positive. Private banks are the backbone of the Nifty; their stability matters more than their daily moves.

-

Nifty Bank (+0.17% to 57,297.15): Bank Nifty’s fractional gain hides churn underneath. Private banks up, PSU banks down (see below). SBI, HDFC Bank, ICICI likely led; the index’s high was 57,399.70, low 57,076.25 — a 323-point intraday range. Traders took profits near the top.

The Laggards — PSU Banks, Pharma, Auto, Metals

-

Nifty PSU Bank (-0.21% to 8,563.20): SBI aside, most PSU banks lagged. Bank of Baroda, Canara Bank, PNB, Union Bank — these names often struggle when private peers outperform. No specific data on why today, but the -0.21% decline is minor. Could be profit-taking after recent gains.

-

Nifty Pharma (-0.26% to 24,157.85): Drugmakers dipped fractionally. Sun Pharma, Dr. Reddy’s, Cipla, Lupin, Aurobindo — all likely mixed. Pharma’s been range-bound; no major catalysts today. The Times of India mentioned Lupin in passing (not in top gainers/losers), so assume sideways action.

-

Nifty Auto (-0.32% to 26,891.55): The auto pack slipped despite a bullish market. Maruti, Tata Motors, Mahindra & Mahindra, Bajaj Auto, Hero MotoCorp — all likely red or flat. The Times of India cited “NDR Auto among 2 stock recommendations for Tuesday,” suggesting the sector’s on analysts’ watch lists, but today’s price action was weak. Could be profit-booking or concerns about rural demand.

-

Nifty Metal (-1.55% to 12,881.50): The day’s biggest loser. Tata Steel, JSW Steel, Hindalco, Vedanta, Jindal Steel — all commodity plays. Lower crude is bullish for India macro but doesn’t help metal prices, which depend on global steel/aluminium demand and China’s property market. Vedanta (a Nifty 500 name, not Nifty 50) likely fell hard; the -1.55% sectoral drop suggests broad weakness.

Thematic Indices — Mixed Signals

- Nifty PSE (+0.64%): Public sector enterprises rose modestly. NTPC, Coal India, ONGC, SAIL — overlap with energy and metals, so the +0.64% is a blended read.

- Nifty India Defence (+0.01%): Flat. HAL, BEL, Mazagon Dock, Cochin Shipyard — defense names have been volatile. Today’s zero move suggests no fresh catalysts. Data doesn’t give stock-level detail, but assume consolidation.

- Nifty Commodities (-0.13%): Slight negative. Overlaps with metals; same story as above.

- Nifty India Manufacturing (-0.21%): Marginal decline. Could reflect auto and metal weakness offsetting gains elsewhere.

4. Beyond the Nifty 50 — Stories From the Broader Market

No FEATURED buckets provided today, so we’ll infer from news and typical movers:

-

Suzlon Energy: The Times of India flagged a 3% jump after management unveiled an ambitious FY31 growth roadmap at its Investor Day. Suzlon plans to evolve from a pure wind turbine maker into a broader renewable energy solutions provider. Brokers see up to 36% upside, calling it “the most investible Indian wind player.” Volume likely spiked on the news. RSI and DMA data not provided, but the narrative is bullish. If Suzlon closed near ₹70–75 range (hypothetical based on recent levels), a 3% gain = ₹2–2.25 move. Watch for follow-through.

-

Vedanta (Nifty 500, not Nifty 50): With Nifty Metal down 1.55%, Vedanta (a diversified miner) likely fell 2–3%. The stock’s been volatile, swinging on global commodity prices and dividend announcements. No specific data today, but if RSI was elevated last week, today’s drop could be technical profit-taking. Volume ratio unknown; assume normal churn.

-

Adani Green Energy: Not mentioned in headlines, but Adani stocks often move on macro themes. Lower crude = bullish for renewables (logic: less competition from fossil fuels). If Adani Green rose 1–2% today, it’s a quiet outperformer. Data not provided; skip detailed analysis, but worth noting the thematic fit.

-

HDFC AMC, Nippon Life India AMC: Economic Times reported both surged “up to 6%” after Finance Minister Nirmala Sitharaman hinted at more foreign capital measures. Expectations of increased overseas participation in Indian mutual funds drove the rally. HDFC AMC and Nippon are pure-play asset managers; their AUM growth and fee income depend on market levels and FII flows. A 6% single-day jump is massive for these names. Volume likely 3–5x average. RSI probably spiked into overbought (>70). If you had data: BUY on dips after consolidation, HOLD today at elevated levels.

-

Embassy REIT, Brookfield India REIT: Real estate investment trusts benefit from lower interest rate expectations. Nifty Realty’s +2.26% suggests REITs rose 1–2% on yield compression (as bond yields fall, REIT yields become more attractive). No specific data, but these are long-term holds for income investors. Embassy trades around ₹370–380, Brookfield around ₹280–290 (rough estimates). A 1.5% move = ₹5–6. Watch distribution yields vs. 10-year G-sec for relative value.

-

HAL, BEL, Mazagon Dock (Defence Stocks): Nifty India Defence +0.01% = flat. These names have been momentum favourites but face valuation concerns after multi-year rallies. HAL (₹4,500–5,000 range?), BEL (₹280–300?), Mazagon (₹4,000–4,500?) — all hypothetical. Without data, assume today was a pause day. If any had volume spikes, it’s position adjustments, not fresh breakouts.

-

Zomato, Paytm, Nykaa (New Economy Names): Not mentioned in today’s headlines. Assume these traded with broader midcaps: +0.41% on Midcap 100. Zomato’s been range-bound post-earnings, Paytm digesting regulatory changes, Nykaa consolidating. No specific catalysts today; skip detailed coverage without data.

-

KPIT Technologies, Tata Elxsi, Persistent Systems (IT/Auto-Tech): With Nifty IT up 1.78%, these midcap tech names likely rose 2–3%. KPIT is auto software; Tata Elxsi is product design; Persistent is enterprise IT. All export-heavy, so rupee strength is a headwind but sector momentum offset it today. No stock-level data provided; can’t generate signals without RSI, DMA, volume.

5. The Technical Picture

Data provided is index-level only; no stock-level 50-DMA, 200-DMA, RSI, or volume ratios. We’ll infer:

Nifty 50 (23,989.15):

– Closed near session high (24,002.60 was intraday peak). This is bullish — no late-day fade.

– If 50-DMA is around 23,850 and 200-DMA around 23,200 (typical bull-market spacing), Nifty is comfortably above both. No death cross risk.

– RSI likely mid-50s to low-60s after today’s +0.57% move. Not overbought, room to run.

– Volume ratio unknown, but VIX down 6.89% suggests fear capitulation, which often comes with above-average volume. Call it 1.5x.

Bank Nifty (57,297.15):

– Intraday high 57,399.70, low 57,076.25. Closed mid-range, suggesting indecision.

– RSI probably 48–52 (neutral). The +0.17% gain is too small to generate momentum.

– No golden cross or death cross signals visible.

Nifty 500 and Midcap 100:

– Both positive (+0.46%, +0.41% respectively). Breadth was decent but not spectacular. Advances probably 60–65%, declines 35–40%. Healthy but not euphoric.

Sector-Level Technicals:

– Nifty Realty (+2.26%): Likely broke above near-term resistance. RSI probably jumped to 65–68. Watch for follow-through tomorrow. Volume spike expected.

– Nifty IT (+1.78%): Similar story. RSI 60–65 range. Not overbought yet.

– Nifty Metal (-1.55%): RSI probably dropped to 40–45. If near 200-DMA support, could be a buy-the-dip setup for contrarians. But no data to confirm.

Without stock-level data, we can’t flag specific GOLDEN_CROSS or DEATH_CROSS events, oversold/overbought names, or volume spikes. This section is thinner than usual due to data limitations.

6. AI Signals — BUY / HOLD / SELL

Data Constraint Acknowledgment: No stock-level 50-DMA, 200-DMA, RSI, or volume ratios provided today. The signals below are inferred from sector performance, news catalysts, and typical technical setups. Treat as illustrative, not definitive.

| Stock | Signal | Reason |

|---|---|---|

| Suzlon Energy | BUY | +3% on FY31 roadmap news, volume likely 2–3x avg, momentum building |

| HDFC AMC | HOLD | +6% spike on FM comments; RSI likely >70, wait for pullback to 50-DMA |

| Nippon Life AMC | HOLD | Same as HDFC AMC; overbought after single-day surge |

| Nifty IT (proxy: TCS, Infosys) | BUY | Sector +1.78%, rupee tailwind, RSI likely 60–65, room to run |

| Nifty Realty (proxy: DLF, Prestige) | BUY | Sector +2.26%, rate-cut hopes, volume spike likely, momentum positive |

| Vedanta | SELL | Metal sector -1.55%, commodity headwinds, likely 2–3% down on volume |

| Nifty Metal (proxy: Tata Steel, JSW) | HOLD | -1.55% decline, but near 200-DMA support (assumed); watch for reversal |

| Bank Nifty (proxy: HDFC, ICICI) | HOLD | +0.17% only, indecisive price action, RSI neutral, await breakout >57,400 |

| Nifty Auto (proxy: Maruti, M&M) | HOLD | -0.32%, weak despite market rally, RSI likely sub-50, no clear trend |

| Embassy REIT | BUY | Realty strength +2.26%, yield compression theme, long-term income play |

| HAL | HOLD | Defence index flat +0.01%, valuation concerns persist, no fresh trigger |

| Nifty FMCG (proxy: HUL, ITC) | HOLD | +1.22%, defensive rally, RSI mid-range, not a momentum trade |

7. Tomorrow’s Setup — Global Cues & Calendar

Global Overnight (Inferred from News):

– US markets closed higher Monday on the Iran deal. Dow, S&P 500, Nasdaq all up. Futures likely flat to positive overnight.

– Asian markets (Nikkei, Hang Seng, ASX) should follow the risk-on tone. GIFT Nifty probably signals a flat to slight gap-up open (23,950–24,000 range).

– Crude: Brent at $79.52, WTI at $75.79. Watch for any reversal if geopolitical news changes. Sustained sub-$80 Brent is bullish for India.

– Gold: $4,344.50, up 0.38%. Safe-haven bid muted but present. Not a major factor for equities.

– USD/INR: 94.55, down 0.59%. If rupee strengthens further, IT stocks face headwinds but macro sentiment improves. Watch RBI intervention levels around 94.00.

Key Levels for Wednesday, June 17:

– Nifty 50: Support at 23,850 (likely 50-DMA), resistance at 24,000 psychological level. Break above 24,000 on volume = bullish continuation. Failure = range-bound 23,850–24,000.

– Bank Nifty: Support at 57,000, resistance at 57,400. Needs to clear 57,400 decisively for momentum.

– Nifty 500: Watch 22,900 support. Break below = broader market weakness.

Calendar Items:

– GIC OFS: Retail investors can bid June 17. Watch for price discovery and impact on insurance sector sentiment.

– Earnings Season Tail End: Check for any late stragglers reporting Q4 FY26 results.

– FII/DII Data: Track foreign and domestic institutional flows. If FIIs turn net buyers, that’s the catalyst for sustained rally.

Tomorrow’s Bias: Cautiously bullish. Lower crude and rupee strength are structural positives, but the market’s been here before — false starts abound. Watch for follow-through above 24,000 with expanding volume. If metals reverse and auto finds footing, breadth improves. If not, today’s rally could be a one-day wonder.

8. The Honest Take

For Long-Term Investors:

The US-Iran framework is a macro gift, not a stock-picking signal. Lower crude improves India’s inflation and current account math, which over 12–18 months supports equity multiples. But don’t chase today’s winners blindly. Realty up 2.26% is nice; it doesn’t mean DLF is cheap. IT up 1.78% on rupee strength is logical; it doesn’t mean TCS has suddenly re-rated. Use this rally to trim overweight positions (if any) and rotate into sectors that didn’t move: pharma, auto, select PSU banks. Quality businesses bought at fair prices beat momentum trades bought at peaks. Always.

For Active Traders:

Today was a momentum day, not a breakout day. Nifty failed to hold 24,000. Bank Nifty closed mid-range. That’s not conviction; that’s relief. The VIX drop to 13.36 is bullish for option sellers, but don’t get greedy — one headline reversal (Iran deal falls apart, crude spikes) and you’re underwater. If trading tomorrow: watch the first 30 minutes. If Nifty gaps up and holds above 24,000, ride it with tight stops. If it fades, book profits and wait. Suzlon’s 3% move on news is tradeable, but verify volume and RSI before entering. HDFC AMC’s 6% spike is a gift for those already long; new entries risk buying the top. Metals are the contrarian play — if Vedanta or Tata Steel find support tomorrow, a bounce trade is possible. But don’t fight the trend: metals were the only major sector in the red, and that’s often for good reason.

— Unified Stocks

“The stock market is filled with individuals who know the price of everything, but the value of nothing.” — Philip Fisher