Unified Stocks — Friday, May 22, 2026

1. The Opening Scene

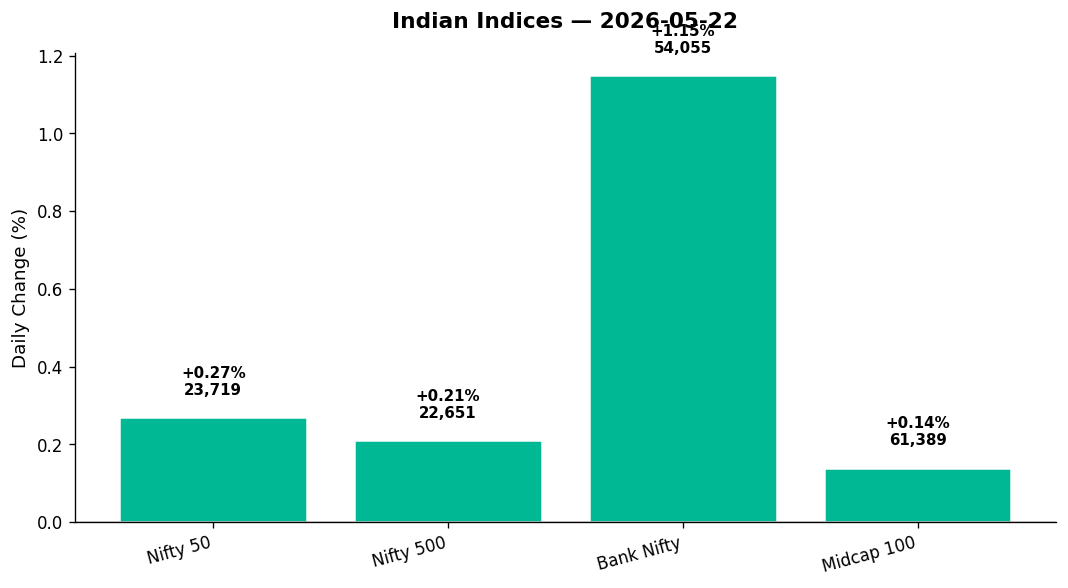

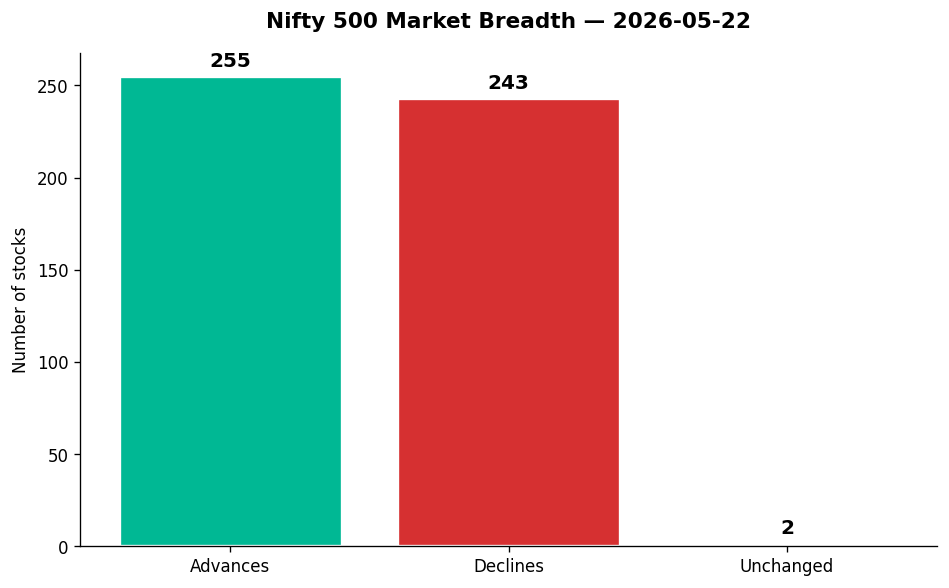

The rupee rallied. Oil climbed. Nikkei soared. The Sensex, by lunchtime, was touching 76,000. And then — as if remembering it was May 2026, a year of volatility and scepticism — the Indian market folded back into itself. By the final bell, the Nifty 50 stood at 23,719, up a modest 64 points. Sensex closed somewhere in the red, erasing a 400-point intraday gain. Bank Nifty? It had the most conviction, surging 615 points (+1.15%) on the back of private bank strength. But the broader market? It shrugged. The Nifty 500 advanced just 0.21%; midcaps barely budged (+0.14%). The breadth read 255 advances versus 243 declines — a market split down the middle, like a coin spinning in mid-air, refusing to land.

This was not a day of convictions. It was a day of skirmishes. Banks won. Pharma and media lost. The defence index stumbled. Cement flew. And beneath the surface, individual stocks performed operas — JSW Cement +7.3% on 13x volume, Honasa Consumer +5.4% on 17x volume, Central Bank of India -8% to a fresh 52-week low. This was the Indian market as jazz ensemble: improvised, dissonant, occasionally brilliant.

2. The Forces That Drove the Day

Four currents shaped Friday’s tape:

-

Global tailwinds, partially digested. Wall Street closed green Thursday night — Dow +0.55%, S&P 500 +0.17%. Asian markets followed with enthusiasm: Nikkei +2.68%, Hang Seng +0.86%, ASX +0.41%. GIFT Nifty signalled a flat-to-positive open. India opened strong, then faded.

-

Rupee strength offered relief. The USD/INR fell 0.88% to ₹95.68, snapping a multi-session losing streak. This mattered for importers, FMCGs, and oil refiners. Yet Reliance, the largest refiner, stayed oversold (RSI 22.77) and gained only 0.62%. The rupee’s bounce was acknowledged, not celebrated.

-

Brent crude at $103 (+0.36%), WTI $96 (-0.19%). Oil remained stubbornly elevated. This weighed on OMCs and the broader Energy index (-0.10%). Gold fell 0.25% to $4,528 — a minor pullback, but still near record highs, signalling residual macro fear.

-

Earnings and corporate action noise. LIC reported Q4 profit up 23% YoY to ₹23,467 crore, declaring a ₹10/share dividend. The stock responded with +1.61% on 8.7x volume. Embassy Developments posted a ₹323 crore loss. WeWork India grew revenue to ₹715 crore, profit up 80%. These were micro signals in a market searching for macro clarity.

The real story: FIIs remain sellers (headlines noted foreign fund selling), domestic flows are cautious, and India VIX (+0.49% to 17.91) refuses to collapse. The market is holding levels — not breaking them.

3. A Walk Through the Sectors

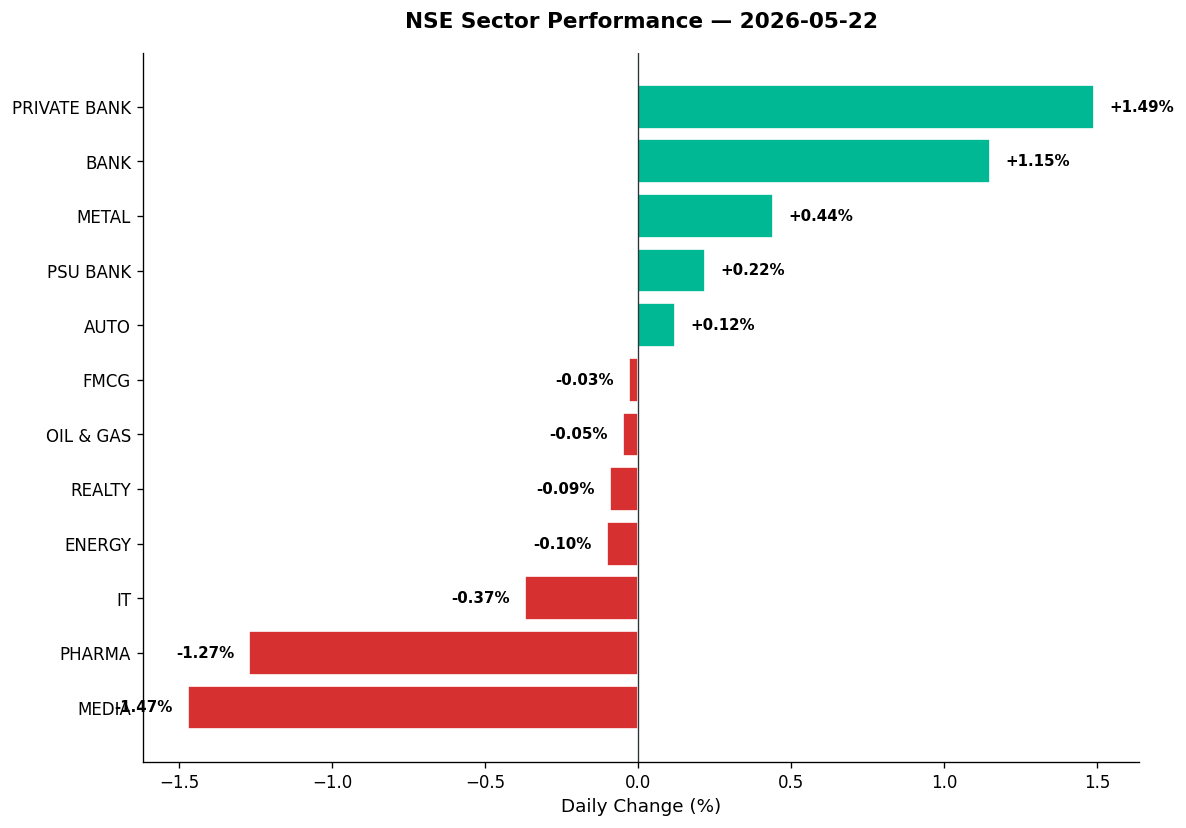

Leaders: Private Banks and Cement

-

Private Bank (+1.49%): HDFC Bank rose 1.30% on softer-than-normal volume (0.78x avg), closing at ₹769 — still in a strong downtrend by RSI (44.69). ICICI Bank +1.96%, also in a downtrend (RSI 47.89), volume light. Axis Bank and Kotak presumably followed (data unavailable), but the sector was led by sentiment, not momentum. The message: banks are oversold, traders bought the dip, conviction is absent.

-

Bank Nifty (+1.15%): Led by private banks. PSU Bank index (+0.22%) lagged badly — Central Bank of India crashed 7.96% to a fresh 52-week low (₹31.22), RSI 25.43, volume 11.5x average. This was a distress sale. Other PSU banks likely dragged.

-

Cement (sub-index not listed, but…): JSW Cement exploded +7.33% on 13.21x volume, hitting an overbought RSI of 75.68. Grasim Industries +0.17%, touching a 52-week high at ₹3,160 — a sign of strength in a defensive play. UltraTech, ACC (data unavailable) likely stable.

Steady Middle: Auto, Metal, FMCG

-

Auto (+0.12%): Muted. Minda Corp (auto components) surged +7.67% on 7.44x volume, RSI 70.65 — a mini-breakout. But the index overall lacked fire. Bajaj Auto, Maruti, Tata Motors — data unavailable, but the +0.12% tells the story: no momentum.

-

Metal (+0.44%): Hindalco touched a 52-week high at ₹1,110 (+0.98%), reflecting aluminium strength. Welspun Corp (iron & steel) fell 4.27%. The sector was mixed — some commodity plays worked, others didn’t.

-

FMCG (-0.03%): Essentially flat. Varun Beverages hit a 52-week high at ₹540.75 (+4.02%), riding volume (18.5M shares). But the broader basket — HUL, ITC, Britannia — stayed range-bound. Rupee relief didn’t translate to buying.

Laggards: Pharma, Media, IT

-

Pharma (-1.27%): Glenmark -5.94%, RSI 37.49, below 50-DMA. Aurobindo Pharma -5.09%, RSI 65.16, still in an uptrend but profit-booked hard. Max Healthcare -6.24% on 5.3x volume — oversold intraday. Narayana Health -4.28%. The sector sold off despite being defensive. Reason? Overvaluation fatigue. Coromandel Fertilizers (agro-pharma adjacent) fell 3.17%, RSI 23.55 — deeply oversold.

-

Media (-1.47%): Sun TV crashed 6.41% on 2.82x volume, RSI plummeting to 17.64 — extreme oversold. The media space remains unloved, lacking catalysts.

-

IT (-0.37%): Soft. Infosys, TCS (data unavailable) likely range-bound. FSL (BPO/KPO) bucked the trend with +6.43% — a niche play, not index-moving.

Also noteworthy:

- Realty (-0.09%): Embassy REIT didn’t feature in today’s data; Brookfield REIT absent. The sector stayed quiet. DLF, Prestige (data unavailable) — no standout moves.

- Defence (-0.22%): Weak. HAL, BEL, Mazagon Dock (data not detailed today) presumably consolidating after recent runs.

- PSE (Public Sector Enterprises, -0.48%): Broad weakness. BPCL, IOC, Coal India (data unavailable) — likely dragged by oil price concerns and lack of reform news.

4. Beyond the Nifty 50 — Stories From the Broader Market

This is where Friday’s real action lived:

Volume Explosions

-

Honasa Consumer (Mamaearth parent, ₹379.90, +5.38%): 68.9M shares traded — 17.23x average volume. RSI 77.48 (overbought). Strong uptrend. This is momentum chasing momentum. The personal care play is hot; traders are piling in. Risk: overbought levels suggest a pullback is near.

-

JSW Cement (₹136.80, +7.33%): 108.5M shares, 13.21x volume. RSI 75.68. Another cement name flying on infrastructure optimism. Watch for profit-taking Monday.

-

Central Bank of India (₹31.22, -7.96%): 117.5M shares, 11.48x volume. Fresh 52-week low. RSI 25.43. This is capitulation. The PSU bank space is being re-rated downward. Avoid until stabilisation.

-

LIC (₹813.05, +1.61%): 18.8M shares, 8.69x volume. Strong Q4 results drove volume. RSI 54.93 — neutral. Above 50-DMA. A rare quality play in the insurer space.

-

3M India (₹33,185, +3.06%): Only 49k shares traded, but that’s 8.82x normal for this illiquid giant. Above 50-DMA, RSI 51.9. Diversified play; likely institutional buying.

-

Nykaa (₹276.50, +0.73%): 31.7M shares, 6.91x volume. RSI 63.66, strong uptrend. E-commerce plays are getting attention as domestic consumption hopes rise.

Midcap & Smallcap Standouts

-

Dixon Technologies (₹11,720, +4.10%): Consumer electronics manufacturing — riding the PLI wave. Volume: 1.36M shares. One of the most actively traded by value today.

-

Deepak Fertilisers (₹1,473, +6.45%): Above 50-DMA, RSI 66.71, volume 4.59x. Fertilizer demand + commodity play. Strong technical setup.

-

Elecon Engineering (₹533.95, +5.91%): Heavy electrical equipment. Above 50-DMA, RSI 52.21, volume 3.76x. Infrastructure beneficiary.

-

Travel Food Services (₹1,124, +5.90%): Restaurants on trains/airports — volume 4.91x. But note: strong downtrend, RSI 23.53 (oversold). This is a relief bounce, not a reversal.

-

Kaynes Technology (₹3,325.80, +4.75%): Industrial products / electronics. Strong downtrend (RSI 34.41), but volume normal. Risky.

-

Pine Labs (₹141.99, -4.27%): Fintech play, RSI 11.46 — the most oversold stock on our radar. Volume 4.46x. Extreme fear. Contrarians might nibble; traders should wait for stabilisation.

New Highs (Quality Signals)

- Polycab (₹9,289.50, +1.04%): Cables/electricals, fresh 52w high. Volume light (177k). Quality play on infra/housing.

- KEI Industries (₹5,285, +0.92%): Same sector, same signal.

- Manappuram Finance (₹324.45, +0.64%): Gold loan NBFC, 52w high. Volume 5M. Defensive play.

- Timken India (₹3,751, +1.04%): Bearings, niche industrial. 52w high, volume 74k.

New Lows (Caution Flags)

- Central Bank (covered above)

- Tata Capital (₹299.70, +0.64%): Fresh 52w low despite positive close. Volume 3.1M. NBFC weakness.

- United Breweries (₹1,313, -1.35%): 52w low, volume 152k. Liquor play under pressure.

5. The Technical Picture

Oversold Names (RSI < 30) — Value Traps or Bounce Plays?

- Reliance Industries (₹1,358, +0.62%): RSI 22.77, strong downtrend. Volume light (0.37x). The heavyweight is oversold, but no catalyst yet. Traders await ₹1,320 support test.

- Pine Labs (₹141.99, -4.27%): RSI 11.46. Extremely oversold. Volume 4.46x. High risk, high reward.

- Sun TV (₹485.50, -6.41%): RSI 17.64. Below 50-DMA. Volume 2.82x. Media space unloved.

- Central Bank (₹31.22, -7.96%): RSI 25.43. Death spiral. Avoid.

- Engineers India (₹215.40, -9.19%): RSI 26.9, below 50-DMA. Volume 3.58x. Infra consultancy hit by project delays?

Overbought Names (RSI > 70) — Profit-Taking Zones

- Honasa Consumer (₹379.90, +5.38%): RSI 77.48. Overbought + 17x volume = pause likely.

- JSW Cement (₹136.80, +7.33%): RSI 75.68. Overbought on massive volume.

- BSE (₹4,194.10, +0.17%): RSI 77.91. Exchange stock in strong uptrend. Likely Nifty 50 inclusion soon (replacing Wipro per headlines). Volume 0.62x — low, but trend is clear.

- Vodafone Idea (₹13.71, +0.66%): RSI 88.67 — the most overbought stock today. Volume 756M shares, 1.34x. Telecom turnaround or speculative frenzy? Likely the latter.

- Triveni Turbine (₹698.90, -0.95%): RSI 76.43. Strong uptrend, but profit-taking started. Volume 3.64x.

Volume Spikes Without Obvious Catalysts

- Minda Corp (₹578, +7.67%): Volume 7.44x. Auto components — likely order wins or broker upgrade.

- Premier Energies (₹972.10, -4.24%): Solar play. Volume 5.44x, RSI 34.93. Strong uptrend but correcting. Watch ₹950 support.

Moving Average Signals

- No fresh Golden Crosses or Death Crosses flagged today — most trends are entrenched.

- Stocks above 50-DMA with neutral RSI (40–60) include: LICI, Grasim, Manappuram. These are stable holds.

- Stocks below 50-DMA with falling RSI (HDFC Bank, Reliance, Sun TV) — downtrends intact.

6. AI Signals — BUY / HOLD / SELL

| Stock | Signal | Reason |

|---|---|---|

| LIC | BUY | Above 50-DMA, RSI 54.93, volume 8.7x avg — strong post-earnings momentum |

| Varun Beverages | BUY | Fresh 52w high, +4.02%, volume 18.5M — consumer staples strength |

| Deepak Fertilisers | BUY | Above 50-DMA, RSI 66.71, volume 4.6x — commodity uptrend intact |

| Polycab | BUY | Fresh 52w high, RSI neutral, quality cable play on infra demand |

| Honasa Consumer | HOLD | Strong uptrend but RSI 77.48 overbought, volume 17x — pause due |

| JSW Cement | HOLD | RSI 75.68 overbought, volume 13x — wait for pullback to ₹130 |

| BSE | HOLD | RSI 77.91 overbought, but Nifty inclusion imminent — mixed signals |

| HDFC Bank | HOLD | Downtrend (RSI 44.69), but near support — not a sell yet |

| Pine Labs | HOLD | RSI 11.46 extremely oversold, but no trend reversal yet — risky |

| Central Bank | SELL | Death trend, RSI 25.43, fresh 52w low on 11x volume — avoid |

| Sun TV | SELL | RSI 17.64 oversold, below 50-DMA, volume 2.8x — downtrend active |

| Reliance Industries | SELL | RSI 22.77, strong downtrend, volume weak — no catalyst visible |

7. Tomorrow’s Setup — Global Cues & Calendar

Global Tape into Monday (India is closed Saturday)

- US equities steady: Dow +0.55%, S&P +0.17%, Nasdaq +0.09%. Tech held up; no major rotation. This keeps sentiment neutral-to-positive.

- Asian strength: Nikkei +2.68% was the standout. Japan rode yen weakness and tech optimism. Hang Seng +0.86%, ASX +0.41%. China stable.

- European gains: FTSE +0.35%, DAX +1.21%. Global risk appetite is recovering post-Iran war fears.

- Crude: Brent $102.95 (+0.36%), WTI $96.17 (-0.19%). Elevated but not spiking. OMCs will stay under pressure.

- Gold $4,528 (-0.25%): Minor pullback. Still near highs. Macro fear hasn’t left.

- USD/INR ₹95.68 (-0.88%): Big rupee gain. If sustained, FMCG and importers get relief. FIIs may slow selling.

- GIFT Nifty 23,719 (+0.27%): Flat signal. Expect Monday open near 23,700.

Key Levels for Monday

- Nifty 50: Resistance at 23,835 (Friday’s high). Support at 23,650 (last week’s pivot). A break above 23,850 opens 24,000. Below 23,600, expect 23,400 retest.

- Bank Nifty: Resistance at 54,200 (Friday’s high). Support at 53,500. Strong close Friday suggests buyers are back.

- Nifty 500: Watch 22,730 resistance. Support at 22,600.

What to Watch Monday

- Any RBI commentary on rupee intervention (headlines noted RBI pre-market actions).

- FII flow data (if negative again, indices stay capped).

- Global crude — if Brent holds $103+, OMCs and Energy stocks stay weak.

- Earnings season winds down, but any late surprises from midcaps could move individual names.

8. The Honest Take

For long-term investors: This is a market stuck in a 23,500–24,000 range, waiting for a catalyst. FIIs are selling, DII flows are absorbing, and earnings haven’t delivered a breakout narrative. Quality names like LIC, Polycab, and Manappuram Finance are forming bases — these are the ones to accumulate on dips. Avoid the extremes: oversold PSU banks (Central Bank) and overbought momentum plays (Honasa, Vodafone Idea). The rupee’s bounce is positive, but one session doesn’t make a trend. Stay invested, stay selective, stay patient.

For active traders: Friday was a stock-picker’s paradise. Volume spikes in Honasa, JSW Cement, and Central Bank offered clear trades — some bullish, some bearish. The Nifty’s 0.27% gain was noise; the real action was in midcaps and sectoral divergences. Monday’s setup is neutral. If GIFT Nifty holds 23,700+, expect a test of 23,850. Bank Nifty’s +1.15% suggests financials have near-term momentum — HDFC Bank and ICICI Bank are tradeable on dips. Watch for profit-taking in overbought cement and consumer names. Stop-losses are your best friend in this chop.

— Unified Stocks

“The stock market is filled with individuals who know the price of everything, but the value of nothing.” — Philip Fisher

Disclaimer: This blog is for informational and educational purposes only. It is not investment advice. All figures cited reflect publicly reported data for the trading session indicated. Markets are subject to risk; please consult a SEBI-registered advisor before acting on any view expressed here.