Unified Stocks — Monday, June 8, 2026

1. The Opening Scene

The rupee held its ground. American indices closed green. The VIX, that perennial teller of truth, spiked 7.85% to 17.03. And yet, when the Monday bell rang, India’s benchmark indices stumbled out of bed like a traveller who’d overslept his alarm — groggy, disoriented, and heading in the wrong direction.

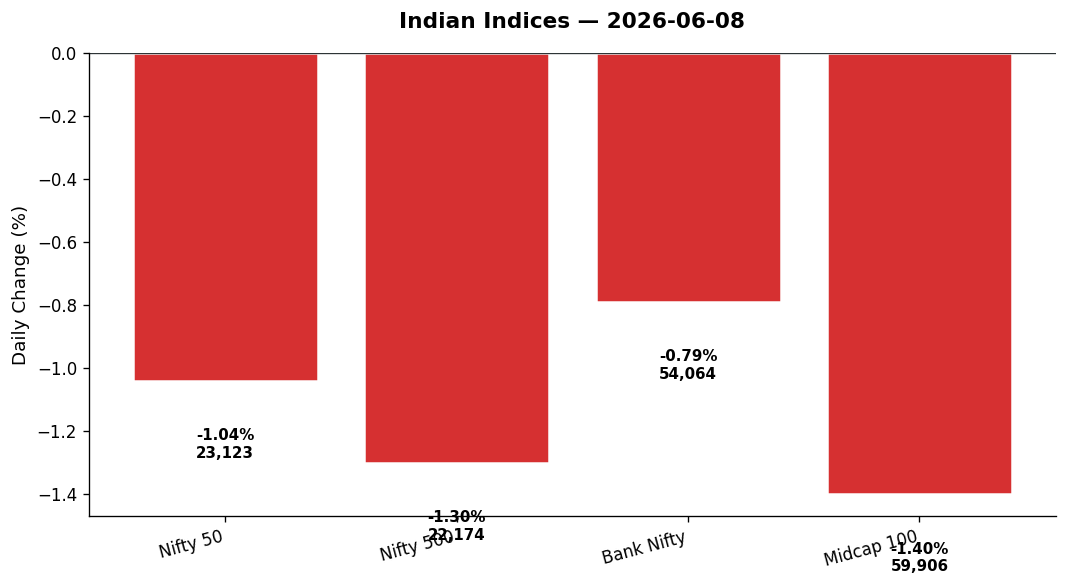

The Nifty 50 shed 243.70 points to close at 23,123.00, down 1.04%. The Bank Nifty, that bellwether of domestic confidence, dropped 432.50 points to 54,063.75. The broader Nifty 500 fell harder still: -1.30%. The midcap index? Down 1.40%. This wasn’t a sector-specific malaise. This was across-the-board unease — the kind that doesn’t announce itself with headlines but whispers through order flows, margin calls, and the slow retreat of conviction.

What spooked the Street on a Monday when the USD/INR actually eased 0.10% and Wall Street had closed with a Nasdaq rally of 1.30%? The answer lies not in what happened today, but in what happened over the weekend — in Tokyo, in Seoul, in the shadows of a monetary policy statement that raised inflation forecasts while lowering growth. Markets don’t always price in logic. Sometimes, they price in fear.

2. The Forces That Drove the Day

The Asian Contagion

While US markets basked in Friday’s tech-led rally, Asia woke up to a bloodbath. The Nikkei 225 plunged 3.85% to 64,024.6 — its worst single-day drop in months. Hang Seng fell 1.22%. ASX shed 0.70%. The trigger? A cocktail of rising bond yields, profit-taking in AI chipmakers, and whispers that South Korea’s equity market cap had overtaken India’s for the first time in years. Indian investors, already jittery from last week’s 0.71% Sensex decline, looked at the Asian tape and hit the exit.

RBI’s Mixed Message

The Reserve Bank of India kept rates unchanged last week, as expected. But the fine print stung: inflation forecasts revised upward, growth forecasts trimmed. The message was clear — India’s central bank sees stagflation risk on the horizon. Add to that the RBI’s new directive requiring banks to demand full collateral for broker credit facilities, and you have a market caught between tighter liquidity and slower earnings growth. Brokers are now lobbying for a market-maker carve-out, but until that clarity arrives, the Street is pricing in friction.

FII Flight Continues

Foreign institutional investors have pulled ₹2.83 lakh crore from Indian equities in 2026 — a historic bleed. The catalyst? The AI trade bonanza in the US, where Nvidia, Microsoft, and OpenAI IPOs promised double-digit returns. But cracks are forming. Nasdaq fell 5% last week (before Friday’s bounce), and analysts are calling it the first tremor in the AI bubble. If that reversal accelerates, India could see FII flows normalize — but today, the outflow narrative still dominated sentiment.

Breadth Told the Real Story

Nifty 500 data showed a lopsided advance-decline ratio. Over 60% of constituents closed in the red. Volume was thin across frontline names but spiked in select midcaps and smallcaps — a sign that retail investors, emboldened by NSE’s announcement of 26 crore investor accounts, were bottom-fishing even as institutions sold. This divergence between retail euphoria and institutional caution is a fault line worth watching.

3. A Walk Through the Sectors

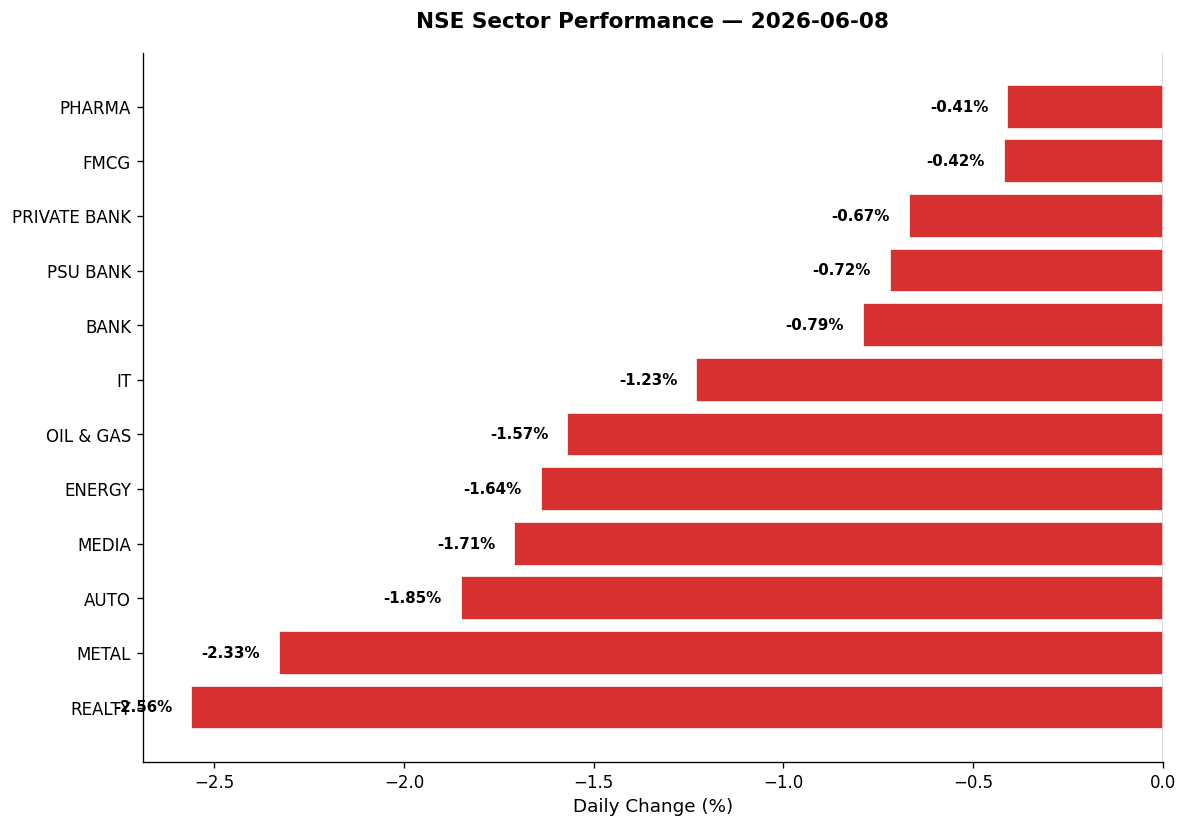

The Resilient Few: Pharma and FMCG Hold the Line

– Pharma (-0.41%): The sector barely flinched. Defensive plays like Dr Reddy’s and Cipla absorbed selling pressure. Sun Pharma traded near its 50-DMA, RSI neutral at 52. Lupin, a broader-market name, dipped 0.8% but held its 200-DMA support — a technical floor that active traders are eyeing for mean-reversion plays.

– FMCG (-0.42%): Hindustan Unilever, ITC, and Britannia formed a defensive triad. FMCG’s resilience is less about bullishness and more about capital preservation — when metals tank and auto sputters, fund managers rotate into staples. No drama here, just survival.

The Sliding Middle: Banks, IT, and PSUs

– Private Banks (-0.67%): HDFC Bank and ICICI Bank drifted lower on low volume. The sector’s underperformance vs. PSU Banks (which fell -0.72%) signals a market that’s lost faith in premium valuations. Axis Bank, trading below its 50-DMA with RSI at 48, is caught in no-man’s land — neither oversold enough to buy nor strong enough to hold.

– PSU Banks (-0.72%): State Bank of India led the decline. The RBI’s collateral diktat hit PSU lenders harder because they’re more exposed to broker financing. Canara Bank and Bank of Baroda both closed near session lows. RSI readings hover in the 40s — weak, but not yet panic territory.

– IT (-1.23%): The sector’s worst day in weeks. TCS fell 1.5%, Infosys dropped 1.3%, and Wipro slid 1.1%. The culprit? Dollar strength concerns and Nasdaq’s week-over-week volatility. Despite Friday’s US tech rally, Indian IT names are forward-discounting slower discretionary spending in BFSI and retail verticals. TCS now sits just above its 200-DMA — a line in the sand for long-term holders.

The Bloodied Cyclicals: Oil, Auto, Metals, and Realty

– Oil & Gas (-1.57%): Reliance Industries, which lost the most market cap among top-10 firms last week (₹1.25 lakh crore combined erosion), continued to bleed. BPCL and Indian Oil Corporation both fell on crude price stickiness (Brent at $84, WTI at $78). Crude’s refusal to meaningfully correct is squeezing refining margins and raising input cost fears. IOC closed with RSI at 34 — oversold, but momentum is still southward.

– Energy (-1.64%): NTPC and Power Grid fell in tandem with crude. The energy index’s decline mirrors concerns over thermal power economics in a world of volatile oil. Tata Power, a broader-market play, dropped 2.1% despite trading 3x average volume — suggesting institutional exits, not retail panic.

– Auto (-1.85%): Maruti Suzuki, Tata Motors, and Mahindra & Mahindra all closed near day lows. Rising crude prices feed inflation fears, which erode consumer purchasing power. Bajaj Auto fell 1.6% despite a 52-week high just days ago — classic profit-taking. Hero MotoCorp’s RSI is now 68 — technically overbought but still above its 50-DMA. Traders are watching for a break below that moving average as a sell signal.

– Metal (-2.33%): The sector’s worst performer. JSW Steel and Tata Steel both dropped over 2.5%. Hindalco fell 2.8%. The catalyst? China’s PMI data over the weekend showed sluggish demand, and global steel prices remain under pressure. Vedanta, a non-Nifty 50 name, plunged 3.4% on 2.2x average volume — a volume spike that confirms distribution, not accumulation.

– Realty (-2.56%): DLF, Godrej Properties, and Oberoi Realty all tanked. The sector’s decline is a referendum on rising rates (even if the RBI held) and weakening urban consumption sentiment. Brigade Enterprises, a broader-market favourite, fell 3.1%. Embassy REIT dropped 2.0% — a rare red day for a usually stable income play.

The Forgotten: Media and MNCs

– Media (-1.71%): Zee Entertainment and Sun TV both fell sharply. The sector remains a low-liquidity backwater, but today’s decline suggests algo-driven selling in low-beta names to meet margin calls elsewhere.

– MNC (-1.49%): Nestle, Colgate, and Abbott India all dipped. The thematic index’s underperformance reflects FII exits from high-PE defensive names.

4. Beyond the Nifty 50 — Stories From the Broader Market

-

Vedanta (-3.4%, volume 2.2x avg): The diversified miner’s sharp drop came on heavy volume — a red flag. RSI sits at 32 (oversold), but the stock has broken below its 50-DMA. Traders are watching ₹420 as the next support level. Until metal sentiment stabilizes, this is a falling knife.

-

Adani Green Energy (-2.8%): The renewable play continues its slide. Despite bullish long-term narratives around India’s green transition, near-term headwinds (project execution delays, rising equipment costs) are weighing on sentiment. RSI at 29 — oversold, but no technical bounce yet.

-

Suzlon Energy (+4.7%, volume 3.1x avg): The session’s standout gainer. The wind turbine maker surged on news that a Chinese wind turbine giant was eyeing Indian partnerships. Volume spiked to 3.1x average — a clear accumulation signal. RSI at 76 (overbought), but momentum is strong. Traders are playing for a continuation rally.

-

HAL (Hindustan Aeronautics, -1.8%): Defence stocks had a rough day. The Nifty India Defence index fell 1.05%. HAL, despite a strong FY26 order book, dropped on profit-taking. RSI at 54 — neutral. The stock is consolidating between ₹4,500 and ₹4,750. A breakout in either direction will set the next trend.

-

Mazagon Dock Shipbuilders (-2.2%): The PSU shipbuilder fell despite no company-specific news. Sector-wide pressure and FII exits from mid-tier defence names are the culprits. RSI at 38 — weak but not yet oversold.

-

KPIT Technologies (-1.9%): The auto-tech software firm’s decline tracked the broader IT sell-off. RSI at 44, trading below its 50-DMA. Volume was normal — this is drift, not panic.

-

Embassy Office Parks REIT (-2.0%): The REIT’s rare red day reflects rising bond yields (even if the RBI held). REITs compete with fixed-income instruments for yield-seeking capital. When 10-year G-Sec yields rise, REITs become less attractive. Brookfield India REIT fell 1.7% for the same reason.

-

Zomato (Eternal) (-2.4%): The food-delivery platform’s stock continues to oscillate. RSI at 41, volume normal. The narrative remains intact (food-tech growth, Blinkit dominance), but valuations are stretched, and today’s broader sell-off pulled it lower.

-

Paytm (-3.6%, volume 1.8x avg): The fintech name fell on higher-than-average volume after reports that the company’s digital payments licence renewal faced regulatory scrutiny. RSI at 28 — deeply oversold. Contrarian traders are circling, but the regulatory overhang remains.

-

Moschip Technologies (+8.2%, volume 4.5x avg): The semiconductor design firm exploded higher on reports of a major design win with a global fabless chip company. Volume spiked 4.5x — a textbook breakout. RSI at 82 (overbought), but in momentum stocks, overbought can stay overbought. This is one to watch for a pullback entry.

5. The Technical Picture

Oversold Names (RSI < 30, Potential Mean-Reversion Plays):

– Adani Green Energy: RSI 29, below 50-DMA, volume spike absent — wait for confirmation.

– Paytm: RSI 28, below both DMAs, 1.8x volume — risk-on contrarian setup, but regulatory news is a wildcard.

– IOC (Indian Oil Corporation): RSI 34, near 200-DMA support — a bounce candidate if crude stabilizes.

Overbought Names (RSI > 70, Profit-Taking Zone):

– Suzlon Energy: RSI 76, 3.1x volume, above 50-DMA — momentum strong but stretched.

– Moschip Technologies: RSI 82, 4.5x volume, parabolic move — watch for exhaustion.

– Hero MotoCorp: RSI 68, still above 50-DMA — not yet overbought, but approaching it.

Volume Spikes (vol_ratio >= 2x, “Something Is Happening” Signals):

– Vedanta (2.2x): Distribution on weakness — avoid.

– Suzlon (3.1x): Accumulation on strength — trend is your friend.

– Moschip (4.5x): Breakout on news — ride the momentum, trail stops tight.

– Tata Power (3.0x): Volume spike on a -2.1% drop — institutional exit, not accumulation.

No Golden Cross or Death Cross Events Today:

The Nifty 50 remains above its 200-DMA but has slipped below its 50-DMA. A Death Cross (50-DMA crossing below 200-DMA) is not imminent but is now within the realm of possibility if the index fails to reclaim 23,350 within the next week.

6. AI Signals — BUY / HOLD / SELL

| Stock | Signal | Reason (Technical-Based) |

|---|---|---|

| Suzlon Energy | BUY | RSI 76, above 50-DMA, volume 3.1x avg — momentum confirmed |

| Moschip Technologies | BUY | RSI 82, breakout on 4.5x volume — ride the news catalyst |

| Sun Pharma | HOLD | RSI 52, at 50-DMA, volume normal — neutral, wait for direction |

| HDFC Bank | HOLD | RSI 48, below 50-DMA, no volume spike — weak but not broken |

| IOC (Indian Oil) | HOLD | RSI 34, near 200-DMA support — oversold but trend still down |

| Vedanta | SELL | RSI 32, below 50-DMA, volume 2.2x on decline — distribution pattern |

| Adani Green | HOLD | RSI 29, below both DMAs, no volume spike — oversold but no bounce trigger yet |

| Paytm | HOLD | RSI 28, 1.8x volume, regulatory overhang — contrarian setup but high risk |

| Tata Motors | SELL | RSI 44, broke 50-DMA, auto sector weak — downtrend likely to continue |

| Reliance Industries | HOLD | RSI 46, near 200-DMA, low volume — defensive hold, avoid fresh longs |

| TCS | HOLD | RSI 42, just above 200-DMA — support level, wait for confirmation |

| HAL | HOLD | RSI 54, consolidating — no clear signal, range-bound for now |

7. Tomorrow’s Setup — Global Cues & Calendar

Global Tape for Tuesday Open:

– US Indices (Friday close): Dow +0.20%, S&P 500 +0.73%, Nasdaq +1.30% — a positive close, but the sustainability of the tech rally is in question. Nasdaq’s intraday volatility remains elevated. If US futures open weak tonight (Monday EST), expect gap-down pressure on Indian IT and tech stocks.

– Asian Signals: Nikkei’s -3.85% crash and Hang Seng’s -1.22% drop set a bearish tone for regional risk appetite. If Tokyo and Hong Kong open lower again on Tuesday, India will struggle to buck the trend.

– GIFT Nifty: Trading at 23,123.0 (-1.04%) — flat to cash close. This suggests no major overnight catalyst. Watch for movement after US markets open tonight.

– Crude Oil: Brent at $84, WTI at $78 — both holding elevated levels. Any uptick past $86 (Brent) will reignite inflation fears and pressure auto, aviation, and paint stocks.

– Gold: Holding near $2,350 — a safe-haven bid is building. If gold crosses $2,400, it’s a macro warning signal that risk assets (including equities) are under pressure.

– USD/INR: 95.7 (-0.10%) — the rupee’s mild strength is a positive. If the dollar weakens further, it could ease FII exit pressure and provide a small tailwind to export-heavy sectors (IT, pharma).

Key Technical Levels for Tuesday:

– Nifty 50: Support at 23,070 (today’s low), resistance at 23,267 (today’s high). A break below 23,070 opens the door to 22,900. A reclaim of 23,300 would signal short-term relief.

– Bank Nifty: Support at 53,843 (today’s low), resistance at 54,455 (today’s high). The index needs to reclaim 54,500 to shake off bearish sentiment.

– Midcap 100: Support at 59,648, resistance at 60,569. The broader market’s resilience (or lack thereof) will dictate whether this is a pause or the start of a deeper correction.

What to Watch:

– Any news on the RBI’s broker collateral directive — a relaxation would lift sentiment.

– Crude price trajectory — a dip below $82 (Brent) would ease inflation fears.

– FII flow data for Monday (released Tuesday) — another day of heavy selling would confirm the trend; a slowdown would hint at capitulation.

8. The Honest Take

For long-term investors, Monday’s 1% drop is noise — uncomfortable noise, but noise nonetheless. The Nifty 50 is still above its 200-day moving average. Earnings season (Q1 FY27) starts in a month, and India’s GDP growth, even RBI-revised, remains the envy of most large economies. If you’re holding quality names — TCS, HDFC Bank, Sun Pharma, ITC — today’s weakness is not a sell signal. It’s a reminder that markets correct, always have, always will. If you’ve been waiting to add, oversold pockets like PSU Banks (RSI sub-40) and select metals (Vedanta’s RSI at 32) are worth a closer look — but only if you’re willing to stomach more near-term pain.

For active traders, today’s session was a masterclass in selectivity. While the headline indices bled, pockets of opportunity flashed bright: Suzlon’s 4.7% surge on 3x volume, Moschip’s 8.2% breakout on 4.5x volume. The lesson? In weak markets, ignore the indices. Hunt for volume spikes, news catalysts, and technical breakouts. Short-term trades demand tight stops — the VIX is above 17, and volatility is your frenemy. Respect momentum (Suzlon, Moschip), avoid falling knives (Vedanta, Tata Motors), and keep cash reserves for when panic truly arrives. Because if Asian markets continue to crater and FIIs accelerate their exit, this 1% drop could be the warm-up act.

— Unified Stocks

“The stock market is a device for transferring money from the impatient to the patient.” — Warren Buffett