Unified Stocks — Thursday, May 21, 2026

1. The Opening Scene

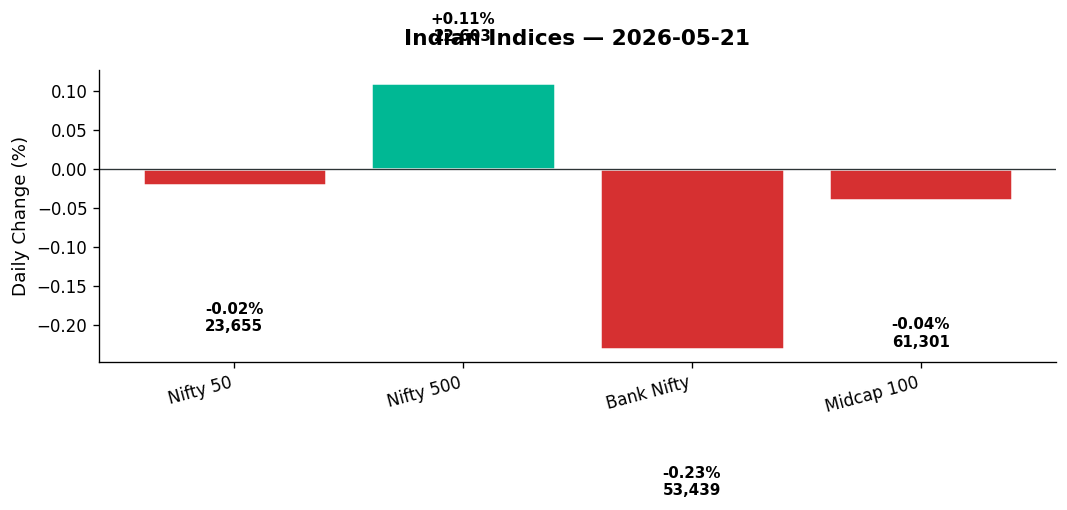

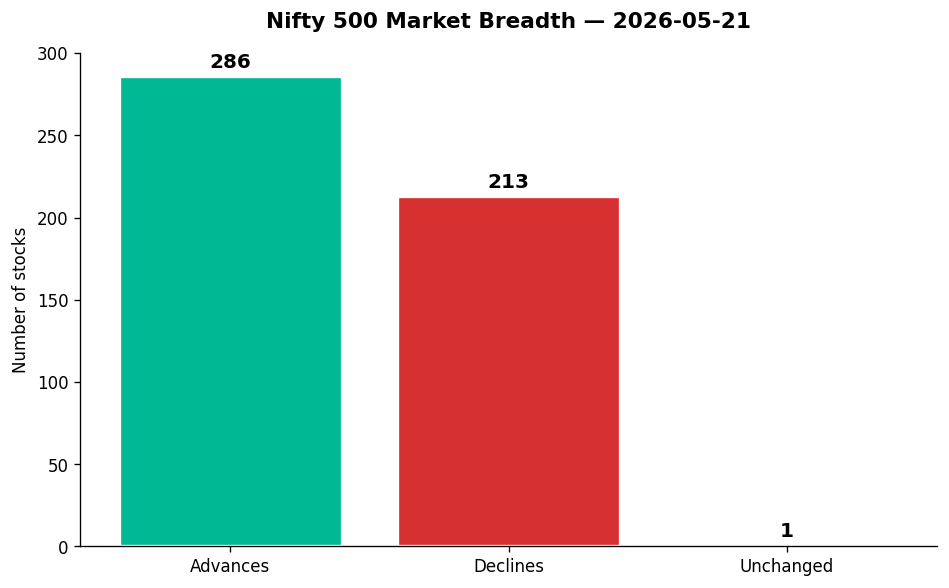

The trading floor opened with a yawn. Nifty 50 slipped into negative territory early, Bank Nifty wobbled under pressure from private lenders, and the morning looked set to bleed red. By 9:30 am, the benchmark had shed nearly 260 points from its opening tick. Crude oil was screaming toward $110, bond yields had touched record highs, and inflation whispers were growing louder. But then — as happens on days when sentiment is too fragile to collapse entirely — the tape turned. Energy stocks found their footing. Defence names marched higher. By the closing bell, the Nifty 50 had clawed back almost everything, finishing just 4.30 points lower at 23,654.70 — a statistical whisper of a loss (-0.02%). The Sensex mirrored the performance. The broader Nifty 500, however, closed in the green (+0.11%), and market breadth told the real story: 286 advances against 213 declines. This was a market that refused to panic, even when the world outside gave it every reason to.

2. The Forces That Drove the Day

Four macro currents shaped Thursday’s session, and all of them arrived with noise.

First: crude oil’s violent surge. Brent crude spiked +3.47% to $108.66, while WTI jumped +3.98% to $102.17. Geopolitical tensions — details unnamed but widely speculated — sent energy traders scrambling. For India, this is a double-edged blade: refiners and upstream oil majors celebrate; downstream consumers (FMCG, paint, transport) wince. The Energy index rose +0.31%, and Oil & Gas added +0.16%, but the broader market absorbed the blow without collapsing.

Second: the rupee’s quiet strength. USD/INR fell -0.39% to ₹96.19, a rare dose of relief amid currency volatility. A stronger rupee softens the import bill for crude, but the $110 barrel price is still a fiscal headache. The government’s subsidy math just got uglier.

Third: inflation’s shadow. News headlines flagged concerns about elevated crude prices feeding into consumer inflation. FMCG names sold off (-0.51% for the sector), as analysts worry that pricing power will erode if input costs climb. Emami dropped -3.47% on heavy volume (5.3x average), while Jubilant FoodWorks collapsed -7.96% on news-driven panic.

Fourth: global cues were mixed but stabilising. US markets closed marginally lower — Dow -0.08%, S&P 500 -0.29%, Nasdaq -0.38% — as chip stocks rallied ahead of Nvidia’s earnings. Asian markets were split: Nikkei surged +3.14% on reopening optimism, while Hang Seng fell -1.03%. GIFT Nifty sat flat (-0.02%), signalling a neutral open for Friday. India VIX dropped -3.34% to 17.82, suggesting fear was draining from the system.

- Market breadth (Nifty 500): 286 advances, 213 declines — a 57-43 positive skew. Not euphoric, but enough to keep bulls engaged.

- FII flows: Data unavailable, but persistent selling in private banks and IT hints at cautious foreign sentiment.

3. A Walk Through the Sectors

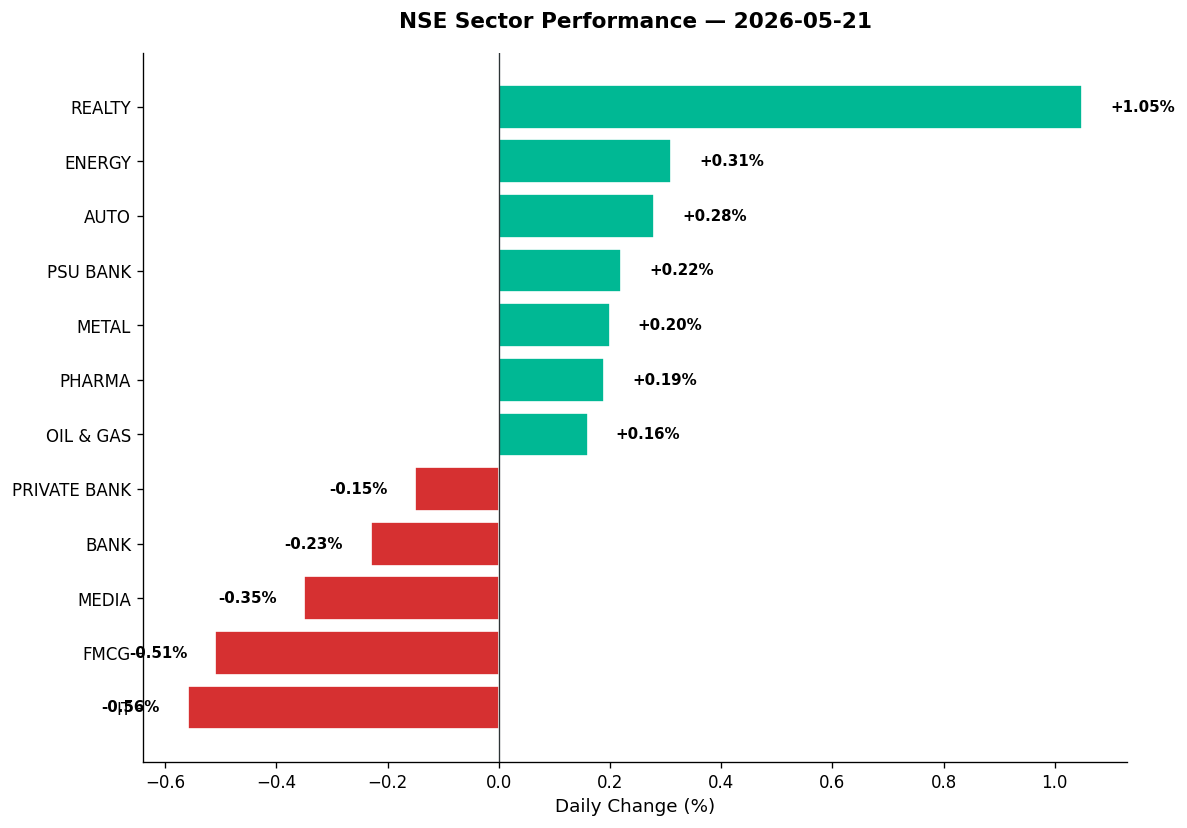

Sector rotation was sharp, nuanced, and largely driven by the energy-inflation complex.

Leaders:

- Realty (+1.05%): The clear winner. With borrowing costs showing signs of peaking and monsoon confidence building, developers got a bid. No individual stock data provided, but the sector index closed at 775.10, its strongest gain in two weeks.

- Energy (+0.31%): NTPC, Power Grid, and other power generators benefited from talk of rising electricity demand. Crude’s rise also lifted upstream plays.

- Auto (+0.28%): Motherson Suri soared +3.57% with RSI at 71.88 (overbought) and volume 3.19x average — component makers are riding EV optimism. Bosch, however, crashed -4.66% on profit-taking, its RSI dropping to 45.23. Two-wheeler EV play Ola Electric fell -3.84%, suggesting the sector’s rally is selective.

- PSU Bank (+0.22%): State Bank of India bucked the trend despite being deeply oversold (RSI 24.92) — it closed nearly flat at ₹950, but that’s a floor worth watching. The sector index gained modestly, hinting at value-hunting.

- Metal (+0.20%): Hindalco hit a fresh 52-week high at ₹1,100 (+1.34%), riding aluminium price strength. Grasim, a Nifty heavyweight, surged +6.43% to ₹3,162 — also a 52-week high — with RSI at 81.96 (overbought) and volume 4x average. Cement is hot; metal is warm.

- Pharma (+0.19%): Aurobindo hit a 52-week high at ₹1,549.50 (+2.11%). Apollo Hospitals rallied +3.11% to ₹8,330 — another 52-week high — with RSI at 81.2 (overbought) and volume 3.3x average. But Eris Lifesciences fell -4.81% on profit-booking, and PI Industries (pesticides) collapsed -5.19% with RSI at 30.32 (oversold) and volume 3.9x average.

Laggards:

- IT (-0.56%): The tech pack couldn’t hold gains despite Nasdaq chip strength. TCS, Infosys, and HCL Tech all drifted lower as investors worried about margin compression amid wage inflation. Persistent Systems, however, was in the news for winning top honours in investor relations — no price data, but sentiment remains positive for mid-tier IT.

- FMCG (-0.51%): The crude spike hit hard. Emami dropped -3.47% (RSI 34.66, volume 5.3x), and Zydus Wellness fell -3.31%. Parle’s unrelated real estate stock hit a circuit after PM Modi gifted Parle Melody toffees to Italy’s PM Meloni — a bizarre case of mistaken identity by retail traders.

- Media (-0.35%): Zee Entertainment and others drifted lower on no fresh catalysts. Sector index closed at 1,395.10.

- Bank (-0.23%): HDFC Bank fell -0.09% with RSI at 44.71 (neutral), while ICICI Bank edged up +0.57% but remains in a strong downtrend (RSI 42.64). The private bank index dropped -0.15%; PSU banks fared slightly better.

Thematic indices told a clearer story:

- Defence (+1.43%): The standout theme. Hindustan Aeronautics, Bharat Electronics, and Mazagon Dock (no individual data) likely led the charge. Tri Turbine, a heavy electrical equipment maker, jumped +7.42% to ₹705.25 — a fresh 52-week high.

- Manufacturing (+0.43%): Amber Enterprises (household appliances) surged +6.39% to ₹7,500 with volume 2.6x average — a strong uptrend with RSI 43.56.

- Commodities (+0.26%): Supported by metal and energy strength.

- PSE (+0.26%): Public sector enterprises continue to attract flows.

4. Beyond the Nifty 50 — Stories From the Broader Market

The day’s most compelling action happened outside the Nifty 50 heavyweights.

- Honeywell Automation (HONAUT): The industrial products giant exploded +15.31% to ₹34,800, with volume 13.85x average and RSI 67.39. Above its 50-DMA, this is a breakout on conviction buying — likely tied to manufacturing capex optimism.

- Sammaan Capital (SAMMAANCAP): The housing finance company rallied +9.13% to ₹154.75 on massive volume (120 million shares, 5.72x average). RSI 59.82 suggests room to run. Affordable housing finance is back in vogue as rural credit demand picks up.

- Techno Electric (TECHNOE): The civil construction play jumped +7.59% to ₹1,294 with volume 5.68x average. Above its 50-DMA, RSI 51.81 — this is infrastructure capex money rotating in.

- Aditya Birla Fashion (ABFRL): Speciality retail surged +7.31% to ₹67.10 on volume 1.74x average. Above its 50-DMA, RSI 56.25 — discretionary spending is showing signs of life.

- Poly Medicure (POLYMED): Medical equipment maker rose +6.82% to ₹1,559 with RSI 53.6. Healthcare capex remains a structural theme.

- IRB Infrastructure: Civil construction play jumped +6.77% to ₹22.56 on colossal volume — 429 million shares, 13.07x average. RSI 63.6, above 50-DMA. Road project announcements likely drove this.

- Tata Communications: Telecom infrastructure play gained +6.57% to ₹1,892.30 — no volume data, but the move suggests institutional interest.

- Grasim Industries: Already mentioned in cement — +6.43%, 52-week high, RSI 81.96 (overbought), volume 4x. UltraTech’s parent is benefiting from cement pricing power.

- India Glycols (IGIL): Diversified commercial services play rose +6.37% to ₹374.75 with volume 8.61x average and GOLDEN CROSS today — the 50-DMA crossed above the 200-DMA. RSI 61.05, strong uptrend. This is a technical breakout with institutional sponsorship.

- JSW Cement: Rallied +5.86% to ₹127.99 with volume 14.43x average — cement pricing power theme in full swing.

On the downside:

- Jubilant FoodWorks: The restaurant chain collapsed -7.96% to ₹434.95 on volume 7.56x average. Strong downtrend, RSI 34.74 — likely earnings disappointment or margin fears from input cost inflation.

- PI Industries: Pesticides play fell -5.19% to ₹2,750.70, RSI 30.32 (oversold), volume 3.94x. Agrochemical demand concerns persist.

- Bosch: Auto components giant dropped -4.66% to ₹35,115, RSI 45.23, volume 3.67x — profit-booking after a strong run.

- Ola Electric: The EV two-wheeler maker slipped -3.84% to ₹35.54 on volume 1.54x average — execution concerns continue to weigh.

- Naukri (Info Edge): The internet retail play hit a fresh 52-week low at ₹921.50 (-2.20%), RSI 33.64 (oversold), strong downtrend. Tech hiring slowdown is hurting sentiment.

5. The Technical Picture

The technicals reveal a market in rotation, not retreat.

Oversold (RSI < 30):

- State Bank of India: RSI 24.92, below 50-DMA — deeply oversold, but volume was light (0.66x average). This is a contrarian setup if PSU bank sentiment turns.

Overbought (RSI > 70):

- BSE (exchange platform): RSI 79.43, strong uptrend — likely Nifty 50 inclusion buzz driving this.

- Grasim: RSI 81.96, fresh 52-week high — cement pricing power theme overbought but momentum strong.

- Apollo Hospitals: RSI 81.2, fresh 52-week high — healthcare capex story overbought but structural.

- Idea (Vodafone Idea): RSI 89.17, strong uptrend — telecom turnaround hopes pushing this to extremes.

- Motherson Suri: RSI 71.88, volume 3.19x — auto components theme hot.

Volume spikes (≥2x average):

- JSW Cement: 14.43x volume

- Honeywell Automation: 13.85x volume

- IRB Infrastructure: 13.07x volume

- India Glycols: 8.61x volume (plus Golden Cross)

- Jubilant FoodWorks: 7.56x volume (downside panic)

- Sammaan Capital: 5.72x volume

- Techno Electric: 5.68x volume

- Emami: 5.31x volume (downside)

Golden Cross:

- India Glycols: 50-DMA crossed above 200-DMA today — a classic bullish breakout signal. Combined with volume surge (8.61x) and RSI 61.05, this is a fresh uptrend.

6. AI Signals — BUY / HOLD / SELL

| Stock | Signal | Reason |

|---|---|---|

| India Glycols (IGIL) | BUY | Golden Cross today, RSI 61.05, strong uptrend, vol 8.61x avg |

| Honeywell Automation (HONAUT) | BUY | Above 50-DMA, RSI 67.39, vol 13.85x avg, breakout momentum |

| IRB Infrastructure | BUY | Above 50-DMA, RSI 63.6, vol 13.07x avg, strong uptrend |

| Sammaan Capital | BUY | Above 50-DMA, RSI 59.82, vol 5.72x avg, housing finance revival |

| JSW Cement | BUY | RSI 62.87, vol 14.43x avg, cement pricing theme intact |

| Techno Electric | HOLD | Above 50-DMA, RSI 51.81 (neutral), vol 5.68x — watch for follow-through |

| Grasim Industries | HOLD | Above 50-DMA, 52w high, but RSI 81.96 (overbought), vol 4x — momentum strong but extended |

| Apollo Hospitals | HOLD | Strong uptrend, 52w high, but RSI 81.2 (overbought), vol 3.29x — wait for pullback |

| PI Industries (PIIND) | HOLD | Strong downtrend, RSI 30.32 (oversold), vol 3.94x — oversold but no trend reversal yet |

| State Bank of India (SBIN) | HOLD | Below 50-DMA, RSI 24.92 (oversold), vol 0.66x — deeply oversold but light volume, contrarian watch |

| Jubilant FoodWorks | SELL | Strong downtrend, RSI 34.74, vol 7.56x avg — panic selling, no reversal signal |

| Naukri (Info Edge) | SELL | Strong downtrend, 52w low, RSI 33.64, vol 1.41x — fresh low on weak volume, avoid |

7. Tomorrow’s Setup — Global Cues & Calendar

The overnight global tape was mixed but stabilising:

- US close: Dow -0.08%, S&P 500 -0.29%, Nasdaq -0.38%. Chip stocks rallied ahead of Nvidia earnings (due after US close Thursday) — the AI demand gauge everyone’s watching. If Nvidia beats, expect tech buying in Asia.

- Asia: Nikkei surged +3.14% on reopening optimism; Hang Seng fell -1.03% on China property worries; ASX rose +1.47%. Mixed signals, but Japan’s strength is notable.

- Europe: FTSE -0.32%, DAX -0.78% — inflation concerns persist.

- GIFT Nifty: Flat (-0.02%) at 23,654.70 — suggests Friday open near unchanged.

Commodity watch:

- Crude: Brent $108.66 (+3.47%), WTI $102.17 (+3.98%) — this is the key risk. If crude holds above $110, inflation fears will intensify.

- Gold: $4,499.20 (-0.71%) — profit-booking after recent highs.

- USD/INR: ₹96.19 (-0.39%) — rupee strength helps, but fragile.

Friday’s technical levels:

- Nifty 50: Support at 23,596 (Thursday’s low); resistance at 23,859 (Thursday’s high). Close above 23,700 would be bullish.

- Bank Nifty: Support at 53,156 (Thursday’s low); resistance at 54,109 (Thursday’s high). Watch PSU banks for reversal.

- Key to watch: Crude price action, Nvidia earnings impact on Asian tech, and domestic auto/cement momentum.

8. The Honest Take

For long-term investors: Thursday’s tape was a reminder that markets don’t collapse on bad headlines alone. Crude at $108 is a headwind, but India’s energy mix is diversifying, and domestic consumption remains resilient. The defence, manufacturing, and infrastructure themes are structural — ignore short-term noise. Grasim’s 52-week high, Apollo Hospitals’ strength, and Aurobindo’s rally tell you where institutional money is flowing: cement pricing, healthcare capex, and pharma exports. If you’re building a portfolio for 2027–2028, Thursday’s leaders are worth studying. Ignore the IT and FMCG weakness — cyclical rotation is healthy.

For active traders: The volume spikes are your roadmap. India Glycols’ golden cross, Honeywell’s breakout, IRB’s 13x volume surge — these are not accidents. Momentum is rotating from Nifty 50 defensives into broader market cyclicals. Shorting Jubilant FoodWorks and Naukri on weakness worked Thursday; both are in strong downtrends with no reversal signals. But be cautious: crude at $110 can reverse sentiment in a single session. If Nvidia disappoints tonight, expect Asian markets to gap down Friday. Use stops. Respect overbought RSIs (Grasim, Apollo, Idea). And watch the rupee — a sharp reversal in USD/INR can unwind Thursday’s calm.

“Volatility is often a symptom of risk but is not a risk in and of itself. Volatility obscures the future but does not necessarily determine the future.” — Peter Bernstein