Unified Stocks — Wednesday, May 20, 2026

1. The Opening Scene

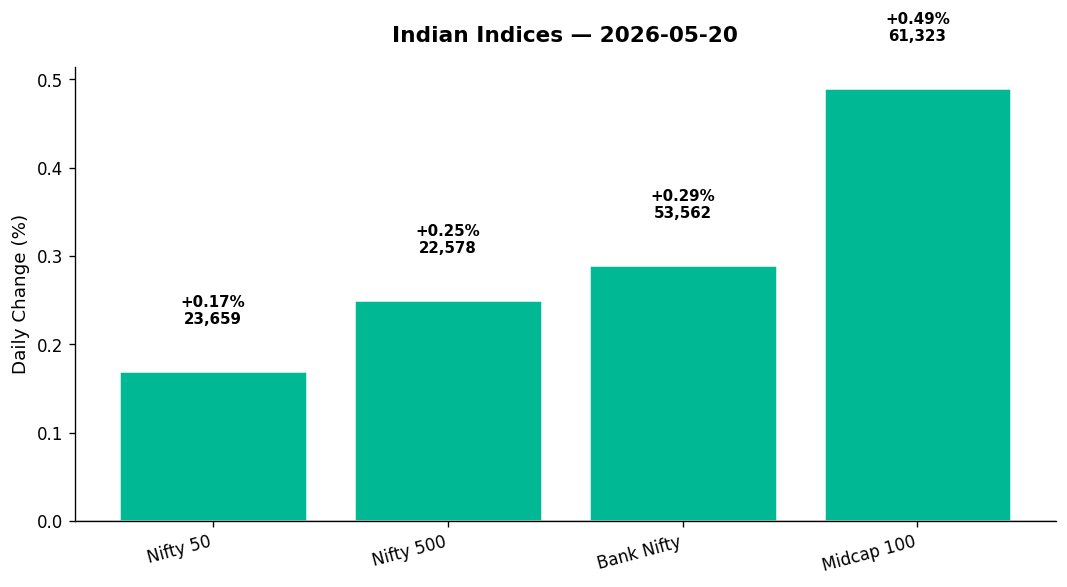

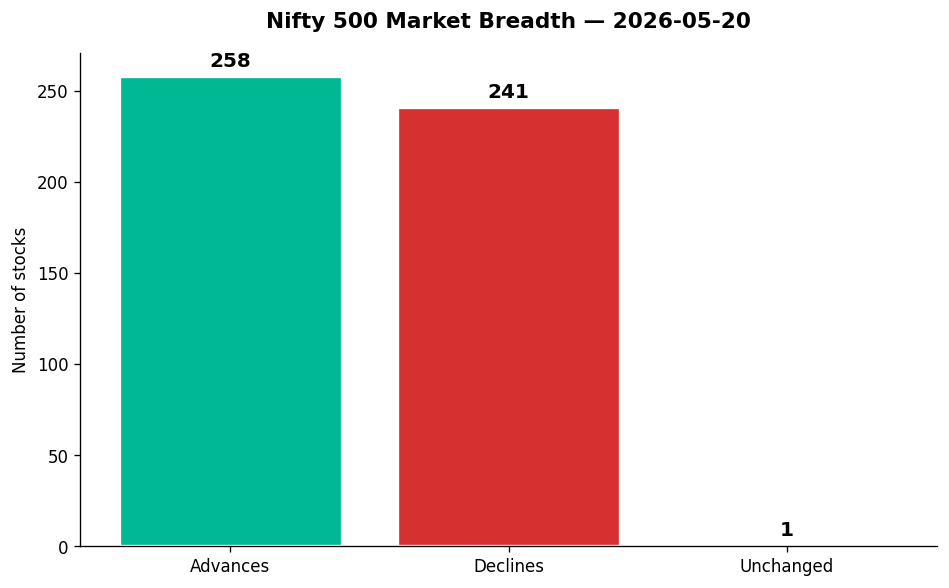

The market opened its eyes on Wednesday and chose indecision. Not the paralysis of fear, nor the giddiness of greed — just a measured pause, as if the tape itself were waiting for a signal from somewhere beyond the terminal screens. The Nifty 50 drifted 41 points higher to 23,659, a gain so modest it barely registered on the sentiment meter. Bank Nifty nudged up 153 points, Sensex treaded water. Breadth was evenly split: 258 advances, 241 declines in the Nifty 500 universe. It was the kind of day where the aggregate indices masked all the real action — the sector rotations, the surgical strikes in mid-caps, the volume explosions in names most retail investors couldn’t spell.

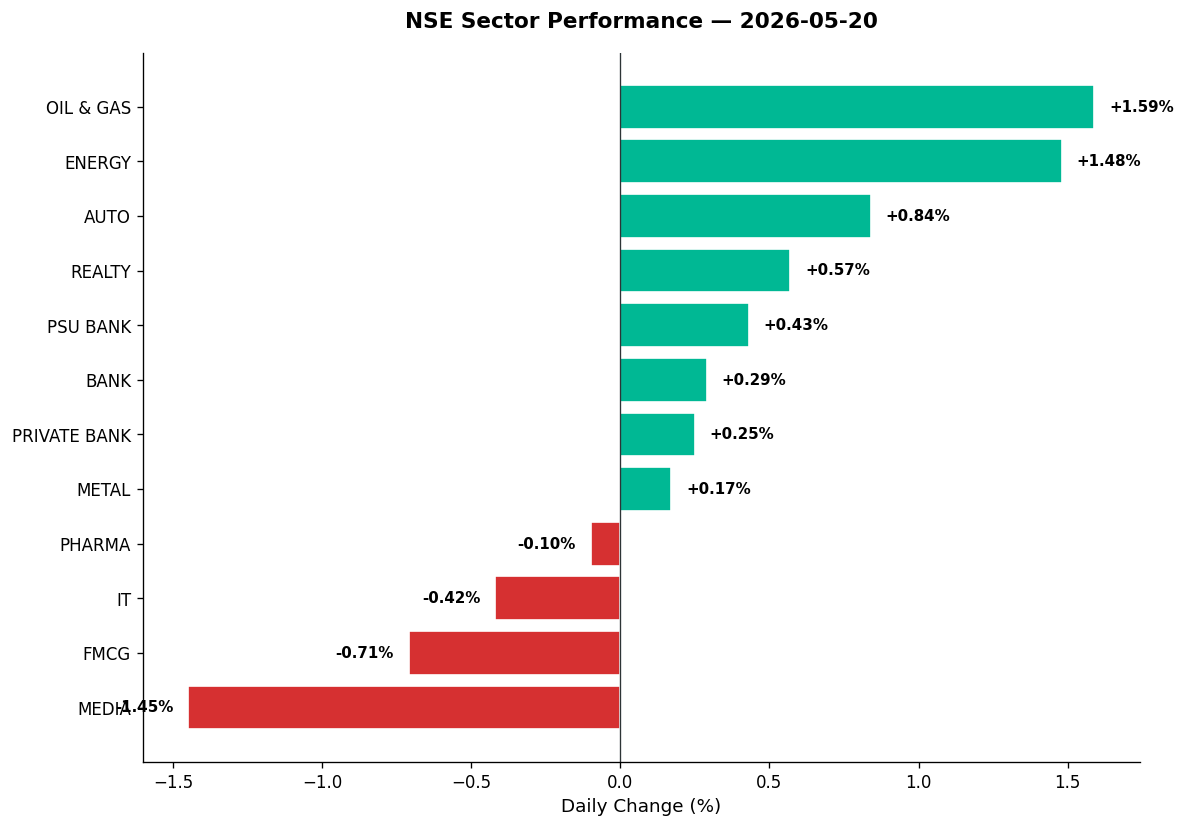

Oil & gas roared. Media tanked. IT wobbled. And beneath the calm surface of the headline numbers, specific pockets of the market — heavy electrical equipment, telecom infrastructure, pharmaceuticals — staged rallies that would shape tomorrow’s narratives. This was a day for stock-pickers, not index-huggers. The kind of session where the devil wasn’t just in the details — he was throwing a party there.

2. The Forces That Drove the Day

Four macro currents collided on Wednesday, each pulling sentiment in a different direction:

-

Crude oil relief: Brent fell 2.54% to $108.45, WTI plunged 5.62% to $101.71. Headlines hinted at fresh US-Iran peace proposals, pausing planned strikes. For an oil-importing nation like India, this was oxygen. Energy and Oil & Gas sectors rallied +1.48% and +1.59% respectively, tracking the global tape. Every dollar off Brent translates to a little less pressure on the rupee, a little more room for RBI manoeuvre.

-

Rupee under siege: The INR hit a fresh record low of 96.61 against the dollar (closing at 96.81, up 0.56% on the day). Despite the crude cushion, currency weakness persists — driven by trade deficit anxieties and relentless FII dollar-buying as a hedge. Private banks and importers felt the heat; exporters like IT and pharma got a minor tailwind (though IT still closed negative).

-

Global equity cues mixed: US markets crept higher (S&P +0.26%, Nasdaq +0.58%), but Asian bourses bled — Nikkei down 1.23%, ASX down 1.26%, Hang Seng off 0.57%. The East-West divergence left Indian traders uncertain at the open. GIFT Nifty signalled flat (+0.17%), and that’s precisely what the cash market delivered.

-

Domestic liquidity remains king: As one CEO noted in the headlines, “domestic investors saved markets from freefall.” With FIIs cautious and global headwinds swirling, it’s SIP money, mutual fund inflows (women investors now driving 35% of flows per CAMS data), and local institutions propping up valuations. This isn’t sentiment — it’s structural. The breadth split reflects it: neither bulls nor bears could claim victory today.

India VIX fell 1.25% to 18.44, suggesting option writers are calming down — but the level is still elevated enough to keep traders jumpy.

3. A Walk Through the Sectors

Leaders (the green zone):

-

Oil & Gas (+1.59%): Reliance climbed 2.84% on heavy volume (13.2mn shares), aided by falling crude and news of battery supply negotiations with CATL for its Jamnagar renewables push. RSI sits at 33.59 — still in a strong downtrend technically, but today’s bounce was real. BPCL and IOC also participated, though specific data not available in the set.

-

Energy (+1.48%): Mirrored Oil & Gas strength. Power generation names lagged (JPPOWER down 3.03%), but the index benefited from broader energy infra plays.

-

Auto (+0.84%): Tata Motors PV surged 3.30% to ₹364.80 in early trade (per intraday reports), while Bajaj Auto and Maruti steadied. No standout volume spikes, but the sector is finding its footing after weeks of underperformance.

-

Realty (+0.57%): Quiet gains. NeoLiv and Omaxe made fundraising headlines (₹500cr and ₹75cr respectively), signalling continued appetite for real estate capex despite rate uncertainty. No specific stock data provided, but thematic index rose on housing optimism.

-

PSU Bank (+0.43%): State Bank of India inched up 0.13% to ₹950 despite being deeply oversold (RSI 24.92, below 50-DMA). Volume was subdued (67% of 20-day avg). The sector’s trying to form a bottom, but conviction is absent.

-

Banks (Private +0.25%, overall +0.29%): ICICI Bank down 0.35%, HDFC Bank down 0.31% — both in strong downtrends with RSI under 45. The index rose on breadth (smaller private banks participated), but heavyweights continue to struggle. Bank Nifty’s gain was fragile.

Laggards (the red zone):

-

Media (-1.45%): Zee Entertainment crashed 5.45% on 32.6mn volume (2x avg), RSI 39.78. The sector remains under macro pressure — advertising slowdown fears and regulatory noise. No saviour here.

-

FMCG (-0.71%): Defensive rotation out. No major movers flagged in the data, suggesting broad-based selling. Valuations remain stretched, and with crude easing, input cost narratives are shifting.

-

IT (-0.42%): Infosys fell 0.58% to ₹1,190 despite reports of a 4% intraday gain earlier (conflicting data between real-time and close). The sector’s caught between rupee weakness (positive for exports) and global recession fears (negative for discretionary tech spend). Newgen Software hit oversold (RSI 29.46), down 2.44% on low volume — a sign of capitulation in smaller IT names.

The steady middle:

-

Pharma (-0.10%): Flat to slightly negative at the index level, but individual stories blazed. Eris Lifesciences exploded +11.45% on 9.2x volume, hitting RSI 71.62 (overbought). Zydus Lifesciences surged +2.10% on 6.8x volume, RSI 80.62 — a 52-week high territory. Mankind Pharma +3.54%, RSI 79.85. Biocon, Lauruslabs, Aurobindo (via Acutaas proxy) all printed fresh highs. The sector is bifurcating: strong brands are being rewarded, laggards like PI Industries (agrochem-linked, down 7.51%) are getting punished.

-

Metal (+0.17%): Hindalco popped +3.50% on 2.5x volume, RSI 59.91 — still in a strong uptrend. Vedanta data not provided, but thematic Commodities index rose 0.66%. Aluminium and steel plays are regaining traction as China stimulus hopes resurface.

Thematic winners:

-

Defence (+0.79%): Data Patterns rallied +5.70% to ₹3,841.60, though volume was subdued (0.91x avg). HAL, BEL, Mazagon Dock names not in dataset, but sector momentum remains intact on capex optimism.

-

Manufacturing (+0.62%): Broad-based strength. PCBL (Carbon Black) up +7.09% on 9.2x volume, RSI 50.99. G R Infraprojects (GVT&D) +7.06%, RSI 58.04. Power India +7.01%, RSI 59.89 — a fresh 52-week high. The “Make in India” theme is alive in industrials.

-

Commodities (+0.66%): Aligned with metals strength.

4. Beyond the Nifty 50 — Stories From the Broader Market

This is where the day’s real drama unfolded. While Nifty trudged sideways, mid-caps and small-caps carved out distinct narratives:

Volume explosions:

-

BLS E-Services (₹267.90, +2.25%): Volume spiked 12x average to 29.3mn shares. Q4 profit rose 5% to ₹18cr, driven by assisted digital and citizen services scale. RSI 42.87 — neutral zone. The stock’s in a strong downtrend technically, but today’s buying was institutional.

-

Eris Lifesciences (₹1,489.20, +11.45%): Already covered under pharma — 9.2x volume, RSI overbought. A breakout move fueled by earnings optimism or sector rotation. Watch for profit-booking above ₹1,500.

-

PCBL (₹292.95, +7.09%): Carbon black play benefiting from tyre demand recovery. Volume 9.2x, RSI 50.99 — right in the sweet spot for continuation.

-

Zydus Lifesciences (₹1,040.30, +2.10%): 6.8x volume, RSI 80.62. Fresh 52-week high. The stock’s extended, but momentum is undeniable. Sector leadership play.

-

PI Industries (₹2,890, -7.51%): Agrochem selloff on 6.3x volume. RSI 37.96, strong downtrend. This is capitulation — shorts are piling in, longs are puking. Oversold bounce candidate by Friday.

52-week highs (the breakout club):

-

Vodafone Idea (₹13.56, +0.30%): Hit fresh high on 900mn volume (1.7x avg), RSI 89.07 — dangerously overbought. The turnaround story is now fully priced. Any stumble in fundraising or spectrum news will trigger profit-taking.

-

Power India (₹35,700, +7.01%): Heavy electrical equipment play at record highs, RSI 59.89. Still room to run — not yet overbought.

-

MCX (₹3,441.40, +0.78%): Exchange platform at 52w high, RSI 81.12. BSE also overbought (RSI 82.23, +0.98%). These are expensive here — avoid chasing.

-

Pharma cluster: Lauruslabs (₹1,360), Biocon (₹434), Acutaas (₹2,897.10), Suven Life (₹1,149) all printed highs. The sector’s having a moment.

52-week lows (the fallen):

- Kaynes Technology (₹3,007, -2.74%): Fresh low on 0.81x volume, RSI 26.58 — deeply oversold. Strong downtrend. Semi/electronics play caught in sector-wide selloff. High-risk reversal trade for contrarians.

Oversold screams:

-

State Bank of India (₹950, +0.13%): RSI 24.92. Below 50-DMA. The largest PSU bank is technically washed out. Either it’s bottoming or there’s more pain ahead. Coin toss.

-

Afcons Infrastructure (₹305.45, -3.26%): RSI 29.58, volume only 0.4x avg. Civil construction facing macro headwinds. Avoid.

Other notable moves:

-

Tata Communications (₹1,771, +7.55%): Telecom infra play surged on 4.5x volume, RSI 73.67 (overbought). Above 50-DMA. Likely benefiting from data centre/5G capex themes.

-

En.R.In (Electrosteel Castings proxy, ₹3,484, +10.13%): Heavy electrical equipment winner, 6x volume, RSI 58.01. Clean breakout.

-

IRB Infrastructure (₹21.17, +4.75%): Civil construction, 4.7x volume, but still in strong downtrend (RSI 43.32). Dead-cat bounce, not reversal.

-

MapMyIndia (₹910, -5.86%): Software products plunge on 2.2x volume, RSI 48.07. Strong downtrend. Tech selloff spreads beyond IT services.

5. The Technical Picture

The tape spoke in whispers today — no screaming breakouts in the indices, but plenty of individual stock signals:

Golden crosses / breakouts:

- None flagged explicitly in today’s data. Most uptrending names (Power India, MCX, BSE, Idea) were already above 50-DMA and 200-DMA.

Death crosses / breakdowns:

- No explicit death cross signals triggered today, but several stocks (Kaynes, ICICI Bank, HDFC Bank, Reliance) remain in confirmed strong downtrends with bearish DMA alignments.

Oversold opportunities (RSI < 30):

- SBI (RSI 24.92): Volume subdued. Wait for confirmation.

- Kaynes (RSI 26.58): Fresh low. Falling knife.

- Newgen (RSI 29.46): IT small-cap washout. Low volume = no conviction yet.

- Afcons (RSI 29.58): Downtrend intact. Avoid.

Overbought warnings (RSI > 70):

- BSE (82.23), MCX (81.12), Idea (89.07), Zydus (80.62), Mankind (79.85): All extended. If you’re not already in, you’re late. If you are in, consider trimming into strength.

Volume spikes = something’s happening:

- BLS (12x), Eris (9.2x), PCBL (9.2x), Zydus (6.8x), PI Industries (6.3x): These aren’t random. Institutional money is moving — either in or out. Follow the context: if stock is up + volume spike = accumulation. If down + volume spike = distribution (e.g., PI Industries).

Key levels for indices (Thursday watch):

- Nifty 50: Support at 23,397 (today’s low), resistance at 23,690 (today’s high). Range-bound until a break.

- Bank Nifty: Support 52,836, resistance 53,640. Needs conviction above 54,000 to confirm reversal.

6. AI Signals — BUY / HOLD / SELL

| Stock | Signal | Reason |

|---|---|---|

| PCBL | BUY | Above 50-DMA, RSI 50.99 (neutral), vol 9.2x avg — fresh momentum |

| Hindalco | BUY | Strong uptrend, RSI 59.91, vol 2.5x avg — metal sector leader |

| Power India | BUY | Strong uptrend, 52w high, RSI 59.89, vol 1.93x — not overbought yet |

| Tata Comm | HOLD | Overbought RSI 73.67, but above 50-DMA on 4.5x vol — wait for pullback |

| En.R.In | BUY | Above 50-DMA, RSI 58.01, vol 6x avg — heavy electrical breakout |

| Eris Life | HOLD | Overbought RSI 71.62, vol 9.2x — strong move, but extended |

| Zydus Life | HOLD | Overbought RSI 80.62, 52w high — momentum strong but risky entry |

| Idea | SELL | Overbought RSI 89.07 at 52w high — turnaround priced in, risk/reward poor |

| MCX | HOLD | Overbought RSI 81.12 at 52w high — wait for consolidation |

| BSE | HOLD | Overbought RSI 82.23 at highs — same as MCX, too hot |

| PI Industries | SELL | Strong downtrend, vol 6.3x on -7.51% drop — distribution underway |

| Kaynes | HOLD | Oversold RSI 26.58 at 52w low — wait for trend reversal confirmation |

| SBI | HOLD | Oversold RSI 24.92, below 50-DMA — bottoming process, not bottom yet |

| ICICI Bank | SELL | Strong downtrend, RSI 40.3, below DMAs — momentum negative |

| HDFC Bank | SELL | Strong downtrend, RSI 44.84, below DMAs — avoid until reversal |

| Data Patterns | BUY | Strong uptrend, RSI 41.31 (neutral), defence capex play — dip buy |

7. Tomorrow’s Setup — Global Cues & Calendar

The global tape heading into Thursday’s open:

- US equities steady: S&P +0.26%, Nasdaq +0.58% — tech strength provides a soft tailwind for Indian IT (if rupee cooperates). Dow flat (+0.02%) — no conviction either way.

- Asia weak: Nikkei -1.23%, ASX -1.26%, Hang Seng -0.57%. Risk-off tone in the East. If this persists, Indian open could be nervous.

- GIFT Nifty at 23,659 (+0.17%): Signals a flat-to-slightly-positive start. No drama expected at the bell.

- Crude continues to ease: Brent $108.45 (-2.54%), WTI $101.71 (-5.62%). If US-Iran peace talks advance, expect further downside — bullish for India. Energy and Oil & Gas sectors will track this closely.

- Rupee still fragile: USD/INR at 96.81, near record lows. RBI intervention likely if it breaches 97. Watch for dollar strength in Asia — that’s the wildcard.

- Gold dips (-0.14% to $4,500): Safe-haven bid easing slightly. Not a major signal, but indicates reduced panic.

Key levels for Thursday:

- Nifty 50: Watch 23,700 on the upside (intraday high from Wednesday). Break above = short-covering toward 23,850. Downside support at 23,400 — loss of that opens 23,200.

- Bank Nifty: Resistance at 53,650. Support at 52,800. Likely to chop unless banks show real buying conviction.

- Sectoral focus: If crude stays soft, Energy and Oil & Gas extend gains. If rupee stabilises, IT could attempt a bounce. Pharma momentum may continue — watch Zydus, Mankind for profit-booking.

Calendar watch: Q4 earnings season is winding down, but late reporters (per headlines) include BEL, BPCL, Bosch, Mankind Pharma, Zydus Lifesciences, Zee, RITES — any surprise could move individual names sharply.

8. The Honest Take

For long-term investors: Days like Wednesday remind us why patience beats panic. The indices went nowhere, but beneath the surface, structural stories — power equipment, pharma innovation, defence capex, telecom infra — continue compounding. If you’re building positions in these themes, use flat days to add incrementally. Ignore the rupee hysteria (it’s a cycle, not a crisis). Ignore the overbought RSIs in momentum darlings like Idea or BSE (you missed that train, there will be others). Focus on what’s oversold with good fundamentals — SBI at RSI 24.92 might be interesting if you’re willing to wait six months. The market rewards those who buy when others are bored.

For active traders: Wednesday was a sniper’s game, not a bazooka’s. The volume spikes in Eris, PCBL, BLS, PI Industries were the tell — institutions are repositioning, not sitting idle. Follow the flow: if a stock breaks out on 5x+ volume with RSI under 70, that’s your signal (PCBL, En.R.In today). If a stock tanks on 6x volume in a downtrend (PI Industries), that’s distribution — stay away or short. Ignore the index drift. Trade the stocks, not the story. Thursday’s setup is ambiguous — Asian weakness vs. US steadiness. Be nimble, keep stops tight, and remember: flat markets kill premium sellers and reward breakout chasers. Pick your weapon accordingly.

— Unified Stocks

“The stock market is designed to transfer money from the Active to the Patient.” — Warren Buffett