Unified Stocks — Monday, May 18, 2026

1. The Opening Scene

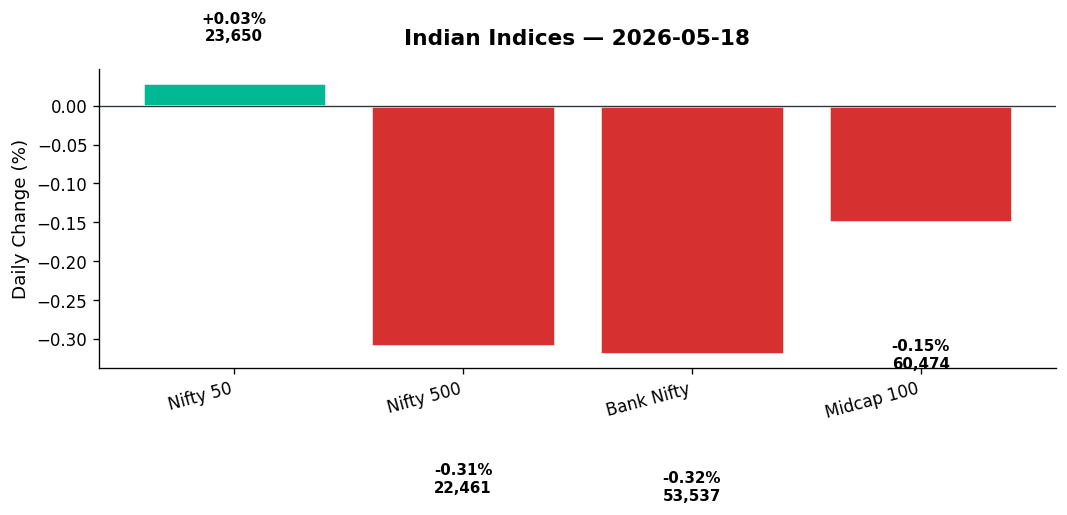

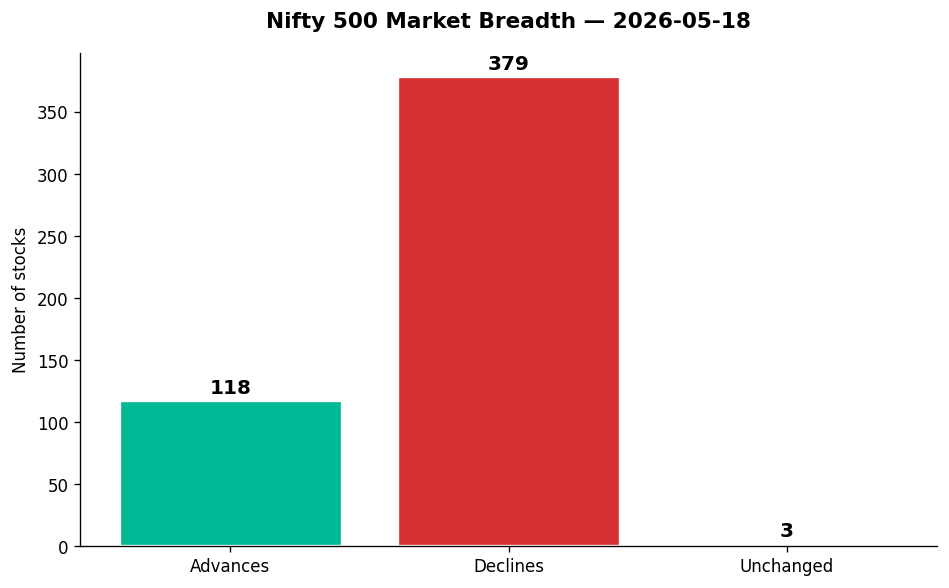

The market opened its week like a man waking from a fevered dream — disoriented, cautious, unsure whether the nightmare has passed or simply paused. The Nifty 50 barely moved, a microscopic 6.45-point gain (+0.03%) landing it at 23,649.95, while Bank Nifty slipped 173 points into the red. Beneath the headline calm, however, a tectonic shift was underway: 379 stocks in the Nifty 500 declined against just 118 advances. This was no ordinary flat day. This was a market splitting into two realities — one where technology and pharma soared on hope, and another where metals, autos, and banks sank under the weight of global unease.

The India VIX jumped 4.47% to 19.63, a reminder that fear remains a living, breathing presence. The rupee slid to 96.33 against the dollar, crude oil hovered near levels that make policymakers sweat, and the broader Nifty 500 fell 0.31%. If Monday’s tape had a voice, it would whisper: “Tread carefully. The storm may have stalled, but it hasn’t passed.”

2. The Forces That Drove the Day

US-Iran Tensions and Crude Oil Anxiety

- The weekend brought no resolution to the US-Iran standoff. Analysts flagged this geopolitical flashpoint — alongside crude oil volatility — as the primary risk to Dalal Street this week.

- While crude prices weren’t explicitly quoted in today’s data, the 0.78% drop in the Nifty Oil & Gas index tells the story: energy stocks are pricing in uncertainty, not opportunity.

- The rupee’s 0.65% slide to 96.33 per dollar compounds the problem. For a net importer of oil like India, a weaker currency plus expensive crude equals margin compression for refiners, airlines, and logistics players.

Global Cues: Mixed but Anxious

- Wall Street closed marginally higher on Friday — Dow +0.30%, S&P 500 +0.18%, Nasdaq +0.05%. But Asian markets stumbled: Nikkei -0.97%, Hang Seng -1.11%.

- The GIFT Nifty signalled a flat-to-positive open at 23,649.95, matching the eventual cash close. Europe’s strength (DAX +1.94%, FTSE +1.26%) failed to lift sentiment here.

- This divergence hints at a deeper unease: India’s market is no longer tracking global rallies with its old enthusiasm. Foreign institutional investors (FIIs) continue to lighten positions, and the narrative has shifted from “AI darling” to “AI laggard.”

Market Breadth: The Carnage Below the Surface

- 379 stocks fell versus 118 that rose in the Nifty 500. That’s a 3.2:1 decline-to-advance ratio — a technical red flag.

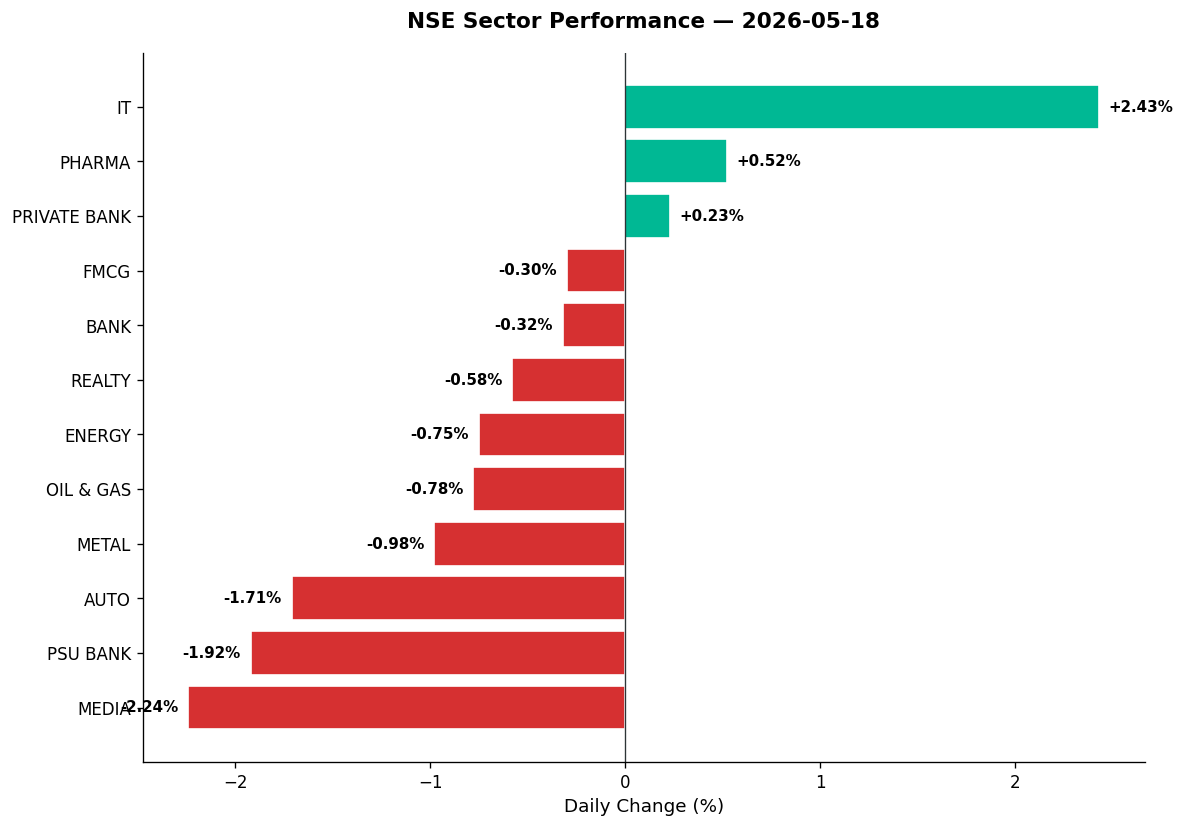

- The Midcap 100 lost 0.15%, but the real pain was sector-specific: Auto (-1.71%), PSU Banks (-1.92%), Media (-2.24%), and Metals (-0.98%) led the retreat.

- Only IT (+2.43%) and Pharma (+0.52%) provided cover. The rest was attrition.

AI Anxiety and Capital Flight

- One headline summed it up bluntly: “India missed out on AI, and now its run as market darling may be over.”

- Foreign investors are rotating capital into Taiwan and Korea — markets riding the AI hardware boom. India’s IT export model, once the crown jewel, now looks slow-footed against the semiconductor frenzy in Asia.

- TCS lost ₹47,415 crore in market cap last week. Reliance shed the most. The top 10 firms collectively bled ₹3.12 lakh crore. That’s not a correction — it’s a rethink.

3. A Walk Through the Sectors

IT (+2.43%): The Rare Bright Spot

- Tech Mahindra (+4.85%) led the charge, closing at ₹1,437 on 2.23x average volume — a clear vote of confidence. RSI 53, above its 50-DMA.

- Coforge (+5.15%) at ₹1,348 and Persistent Systems (+5.48%) at ₹4,960 followed, both riding the “maybe India isn’t dead in tech” thesis.

- Oracle Financial Services (+4.88%) at ₹9,455 — a niche software play — also surged, though on lighter volume.

- Context: These gains are defensive, not triumphant. With the rupee weakening, dollar-earning IT firms get a currency tailwind. But the sector’s 2.43% gain feels more like relief than revival.

Pharma (+0.52%): Hitting New Highs

- Gland Pharma (+15.24%) was the day’s undisputed star, rocketing to ₹2,153 on 14.46x average volume. RSI 76.99 (overbought), but who’s arguing? This was a breakout on steroids.

- Sun Pharma (+1.37%), Ipca Labs (+2.80%), and Lupin (+0.43%) all touched fresh 52-week highs. The pharma trade is back — driven by global demand, pricing power, and a weak rupee aiding exporters.

- This sector remains one of the few where “Made in India” still commands global respect.

Private Banks (+0.23%) vs PSU Banks (-1.92%): The Great Divergence

- HDFC Bank (+0.17%) and ICICI Bank (+0.58%) held steady, but it was unconvincing. RSI for ICICI: 36.3, deep in neutral territory despite being in a downtrend.

- SBI (-2.53%) collapsed to ₹938.80, RSI 19.09 — deeply oversold. That’s the lowest RSI in the featured data, signalling panic or capitulation.

- PSU Bank index down 1.92%. The message: investors don’t trust public-sector lenders to navigate a slowing economy and rising bad loans.

Auto (-1.71%): The Wheels Come Off

- TVS Motor (-5.07%) at ₹3,291, volume 2.66x average, RSI 36.53 — below its 50-DMA and falling fast.

- Apollo Tyres (-4.94%) hit a fresh 52-week low at ₹375, RSI 20.57 — deeply oversold.

- The auto sector is pricing in a demand slowdown. Rural distress, high vehicle prices, and a weak monsoon forecast are all headwinds.

Metals (-0.98%): Rust and Ruin

- Tata Steel (-3.15%) at ₹210.01, volume 2.71x average. RSI 43, still technically neutral, but the downtrend is clear.

- Jain Irrigation Systems (-19.63%) — the day’s biggest loser in the Nifty 500 — collapsed to ₹455 on 2.16x volume. RSI 56 suggests this wasn’t technically driven; this was news or panic.

- Gallantt Metal Products (-7.50%) at ₹689, RSI 23.94 — oversold. This is the underbelly of the commodities rout: smaller, leveraged names getting crushed.

Realty (-0.58%), Energy (-0.75%), Media (-2.24%): The Walking Wounded

- Realty: No standout movers, just a slow bleed. The housing boom narrative is fading as interest rates stay elevated.

- Energy & Oil & Gas (-0.78%): The US-Iran conflict should be bullish for energy, but domestic players are caught between crude volatility and policy uncertainty. No clear winners today.

- Media (-2.24%): Saregama (-6.05%) at ₹390.60, volume 1.41x average, RSI 59.92. The content play is losing its lustre.

4. Beyond the Nifty 50 — Stories From the Broader Market

Shipping: The Surprise Winner

- Great Eastern Shipping (+9.66%) at ₹1,682 on 9.46x average volume. RSI 69.14, strong uptrend. This is a global trade play — container rates are firming, and shipping stocks are quietly building momentum.

- Shipping Corporation of India (+3.80%) at ₹344, volume 1.94x average, RSI 69.89. Another confirmation: the shipping cycle is turning.

Capital Goods Carnage

- KEC International (-10.68%) at ₹489.95, volume 3.57x average, RSI 30.43 — strong downtrend. Order flow worries? Margin pressure? This is a stock in distress.

- Amber Enterprises (-15.39%) at ₹7,172 on 5.65x volume, RSI 34.46, below 50-DMA. A household appliances play, crushed by demand concerns or earnings miss.

Defence & PSE: The Patriotism Trade Wobbles

- Nifty India Defence (-0.51%), Nifty PSE (-1.38%) both slipped. The defence boom that carried HAL, BEL, and Mazagon Dock to stratospheric heights is pausing.

- No specific defence names in today’s featured data, but the thematic index tells the story: profit-taking after a long run.

Semiconductors and Speciality Tech

- MapMyIndia (-7.41%) at ₹939, volume just 0.61x average, RSI 50.03. A software product play that’s lost its narrative in the AI noise.

- KPIT and Tata Elxsi — absent from today’s featured data — remain the semi/EV software plays to watch. Their silence today is telling.

Solar and Clean Energy

- Solar Industries (+4.03%) at ₹18,011 — a fresh 52-week high on 3.85x volume, RSI 81.71 (overbought). Explosives maker, not solar power, but a curious name-price mismatch. This is a defence/mining play riding the capex cycle.

- JSW Energy (+2.90%) at ₹530, volume 1.37x average, RSI 28.97 — oversold despite being in a strong uptrend. A rare BUY signal candidate: beaten down, but fundamentals intact.

Fintech and New-Age Names

- Policybazaar (+3.60%) at ₹1,749, volume 1.38x average, RSI 62.88. The fintech insurance aggregator is back in favour. Above 50-DMA, neutral RSI — a HOLD with upside optionality.

- Lenskart (+2.06%) at ₹478.90, RSI 12.48 — the most oversold name in the data. This is a contrarian BUY if you believe the eyewear story still has legs.

The 52-Week Low Dungeon

- Kaynes Technology (-5.19%) at ₹3,102, RSI 27.7 — fresh 52-week low. A small-cap electronics manufacturing services (EMS) play, caught in the capex slowdown.

- Jyoti CNC (-3.53%) at ₹682.35 — machine tools, another victim of the manufacturing pause.

- Tata Capital (-1.59%) at ₹303.05 — NBFCs are out of favour as credit growth slows.

5. The Technical Picture

Oversold Names (RSI < 30): Contrarian Opportunities or Value Traps?

- SBI (₹938.80, RSI 19.09): Below 50-DMA, volume 0.93x. This is deep capitulation. If you believe PSU banks will recover, this is your entry.

- Kaynes Technology (₹3,102, RSI 27.7): Strong downtrend, volume 1.28x. Risky, but oversold.

- JSW Energy (₹530, RSI 28.97): Strong uptrend, volume 1.37x. The best technical setup here — a HOLD with BUY potential on confirmation.

- Lenskart (₹478.90, RSI 12.48): The most extreme oversold reading. Either a turnaround brewing or a broken story.

- PG Electroplast (₹459.50, RSI 10.72): Consumer electronics, strong downtrend, volume 1.96x. Avoid unless you have conviction.

Overbought Names (RSI > 70): Momentum or Exhaustion?

- BSE (₹4,119, RSI 80.41): Fresh 52-week high, strong uptrend, volume 1.4x. The exchange stock is expensive, but momentum is real.

- Idea Cellular (₹12.98, RSI 86.47): Telecom turnaround story, strong uptrend, volume 2.43x. Overbought, but believers are doubling down.

- Gland Pharma (₹2,153, RSI 76.99): Volume 14.46x. This is parabolic, but with that volume, it’s conviction, not froth.

- Solar Industries (₹18,011, RSI 81.71): Volume 3.85x, fresh 52-week high. Overbought but still climbing.

Volume Spikes (>2x): Where the Action Is

- Gland Pharma (14.46x), Great Eastern Shipping (9.46x), Amber Enterprises (5.65x), Solar Industries (3.85x) — these are the stocks where real money is moving. Gland and GE Shipping are buys; Amber is a sell; Solar is a momentum HOLD.

No Golden or Death Crosses flagged explicitly today, but the 50-DMA/200-DMA crossover watch list remains critical for swing traders.

6. AI Signals — BUY / HOLD / SELL

| Stock | Signal | Reason |

|---|---|---|

| Gland Pharma | BUY | Above 50-DMA, RSI 76.99, vol 14.46x avg — parabolic breakout on conviction volume |

| Great Eastern Shipping | BUY | Strong uptrend, RSI 69.14, vol 9.46x avg — shipping cycle turning |

| Persistent Systems | BUY | Above 50-DMA, RSI 55.83, +5.48% on IT sector strength |

| Coforge | BUY | Above 50-DMA, RSI 66.24, vol 0.98x — stable IT play riding rupee tailwind |

| JSW Energy | HOLD | Strong uptrend, RSI 28.97 (oversold), vol 1.37x — wait for bounce confirmation |

| Policybazaar | HOLD | Above 50-DMA, RSI 62.88, vol 1.38x — fintech recovery play, watch 1750 resistance |

| BSE | HOLD | Fresh 52w high, RSI 80.41 (overbought), vol 1.4x — momentum strong but extended |

| Solar Industries | HOLD | Fresh 52w high, RSI 81.71 (overbought), vol 3.85x — parabolic but still in play |

| Apollo Tyres | SELL | Fresh 52w low, RSI 20.57 (oversold), strong downtrend — avoid until stabilization |

| Amber Enterprises | SELL | -15.39%, vol 5.65x, RSI 34.46, below 50-DMA — heavy distribution, exit |

| KEC International | SELL | -10.68%, vol 3.57x, RSI 30.43, strong downtrend — capital goods stress |

| Jain Irrigation | SELL | -19.63%, vol 2.16x, RSI 56.52 — likely news-driven collapse, avoid catch-the-knife |

7. Tomorrow’s Setup — Global Cues & Calendar

Global Tape: The Week Ahead

- US markets closed marginally higher Friday, but the real test comes this week. With US-Iran tensions unresolved and crude prices volatile, any escalation will hit risk assets hard.

- Asian markets are already pricing in weakness: Nikkei and Hang Seng both fell over 1% today. If Asian futures remain soft overnight, expect India to gap down at open.

- GIFT Nifty at 23,649.95 suggests a flat open — but watch the first 30 minutes. If SGX Nifty trends lower, follow the flow.

Currency and Commodities

- USD/INR at 96.33 (+0.65%) — the rupee is under pressure. RBI intervention is likely, but sustained weakness will hurt importers.

- Crude oil remains the wildcard. No specific data provided, but the 0.78% drop in Oil & Gas index suggests traders are nervous, not bullish.

- Gold: No data provided, but with geopolitical risk elevated, gold typically rallies. Watch for gold-backed stablecoin headlines (one piece flagged them as a future investment trend).

Key Levels for Tuesday

- Nifty 50: Support at 23,317 (today’s low), resistance at 23,800. A break above 23,700 could trigger short-covering.

- Bank Nifty: Support at 52,783 (today’s low), resistance at 53,650. PSU banks are the weak link — watch SBI’s bounce or breakdown.

- Nifty 500: Watch the breadth. If advances-to-declines ratio stays poor, the correction extends.

Earnings and Events

- No major earnings flagged for Tuesday in the provided data, but Q4 results season is winding down. Watch for any laggards reporting late.

- Derivatives expiry week: This is the third Monday of May — weekly options expiry on Thursday. Volatility (VIX +4.47%) suggests swings ahead.

8. The Honest Take

For Long-Term Investors:

Monday’s tape was a reminder that markets do not move in straight lines, even when they appear to. The Nifty 50’s 6.45-point gain was a mirage; the real story was 379 stocks falling. If you’re holding quality names — pharma, IT exporters, select financials — today was noise, not signal. The rupee’s slide is a tailwind for exporters; the AI hysteria will pass, and India’s consumption and infrastructure story will reassert itself. But patience is required. The next few weeks will test conviction. Add selectively on dips. Avoid the temptation to chase shipping or defence stocks at these levels — wait for pullbacks.

For Active Traders:

This was a stock-picker’s market, not an index trader’s paradise. IT and pharma longs paid; auto and metal shorts paid. The key now is to watch sector rotation and volume. Gland Pharma’s 14.46x volume spike was a gift — you either caught it or you didn’t. Tuesday’s setup favours caution: if the market gaps down, let the first hour shake out weak hands before deploying capital. The oversold names (SBI, JSW Energy, Lenskart) are on the watchlist, but wait for confirmation — an RSI bounce, a volume spike, a green candle. Don’t catch falling knives. And if the VIX stays above 19, hedging with puts or collars makes sense.

“The stock market is filled with individuals who know the price of everything, but the value of nothing.” — Philip Fisher