Unified Stocks — Thursday, May 14, 2026

1. The Opening Scene

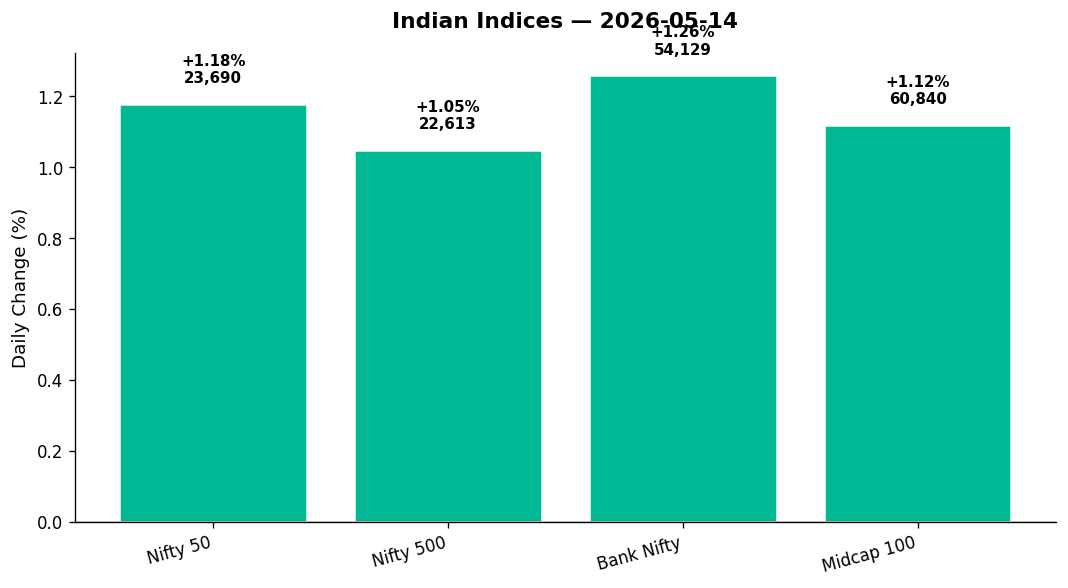

The rupee hit another lifetime low. Oil bled lower. Iran and the West played their usual chess game in the background. And yet — India’s equity markets surged, as if shrugging off the gloom with a knowing smile. The Nifty 50 climbed 277 points to close at 23,689.60, a 1.18% gain that felt less like a relief rally and more like a declaration: we’re done falling.

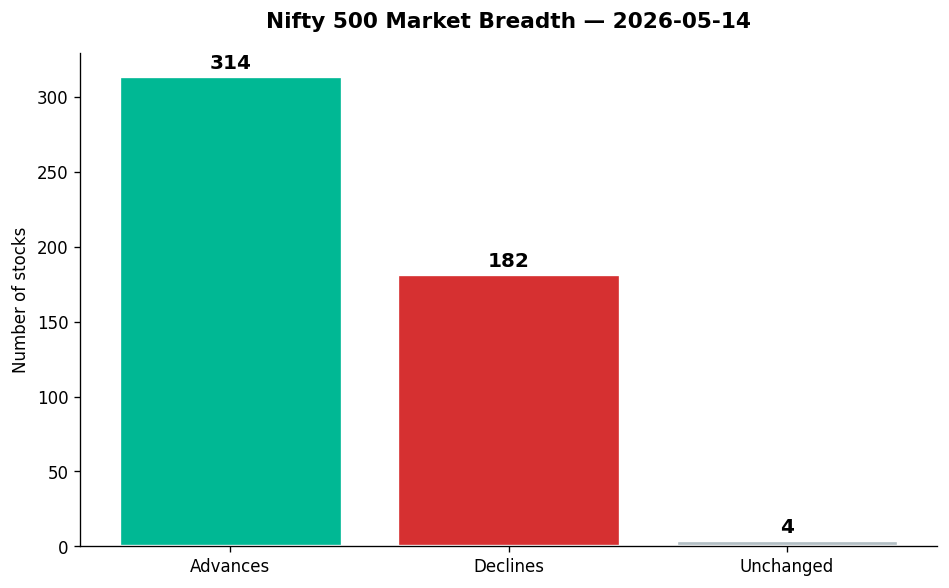

Breadth told the real story. Out of 500 stocks, 314 advanced. That’s not rotation — that’s conviction. The VIX, that fear gauge everyone watches but few trust, fell 4.18% to 18.61. Markets don’t melt up when participants are terrified. They melt up when sellers exhaust themselves and buyers sense blood. Today, the buyers won. But beneath the green tape, the market’s personality split cleanly: pharma and metals soared, tech bled, and the real action played out far beyond the Nifty 50’s household names.

2. The Forces That Drove the Day

Four forces collided to shape Thursday’s tape:

-

Crude’s retreat: Brent crude fell 1.21% to $104.35, WTI down 1.14% to $99.87. Oil’s pullback eased inflation fears and gave refiners breathing room, even as the rupee slid to 95.75 per dollar — a fresh all-time low. The currency’s weakness should have spooked markets. Instead, it emboldened metal exporters and pharma players who bill in dollars and benefit from a weaker rupee.

-

FII positioning reset: After weeks of relentless selling, foreign institutional investors appear to have hit pause. As one analyst noted in the headlines, “the worst FII selling may be over.” India had underperformed Korea by 180 percentage points through the recent drawdown. Valuations compressed. Expectations cooled. That’s the setup for a bounce — and today delivered one.

-

US tech momentum: The Nasdaq rose 1.20% overnight, the S&P 500 gained 0.58%. Tech optimism abroad didn’t translate to India’s IT sector, which fell 1.99% — a divergence we’ll unpack later. But global risk appetite improved, and that lifted sentiment across emerging markets.

-

Breadth breadth breadth: 314 advances versus 182 declines in the Nifty 500. That’s a 1.73-to-1 ratio — healthy, broad, and sustained. This wasn’t a handful of heavyweights dragging the index higher. Mid-caps rose 1.12%, matching the Nifty 50’s pace. When mid-caps keep up, the rally has legs.

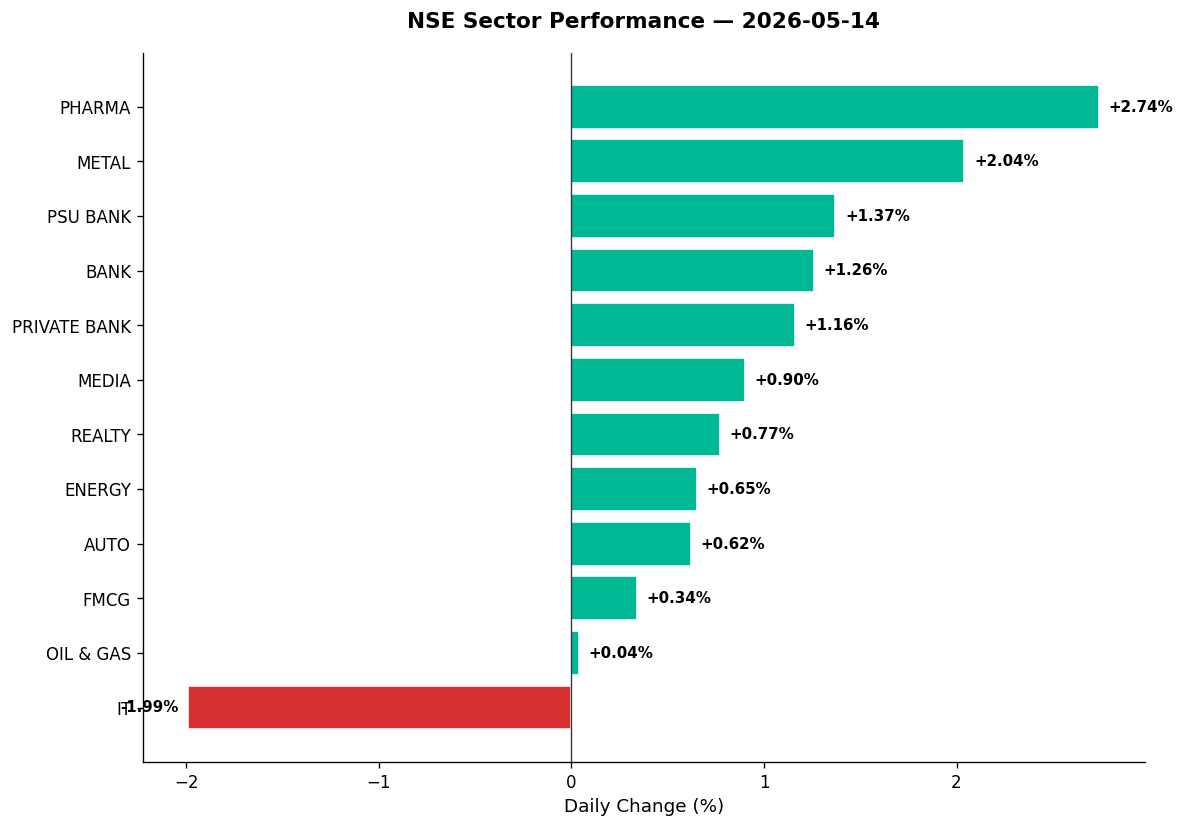

3. A Walk Through the Sectors

The sector action today was theatrical — a clear divide between the haves and have-nots:

LEADERS:

-

Pharma (+2.74%): The day’s king. Cipla surged 8.09% to ₹1,435 on 4x average volume, RSI at 71.74 (overbought but earned). Caplipoint jumped 9.89% to ₹2,024, volume spiking 11.66x. Zydus Life rose 5.79% on news it’s close to acquiring a US oncology drugmaker for $100–150 million — building its own distribution network stateside. The rupee’s weakness is a tailwind here: dollar revenues convert to more rupees, margins expand. Add defensive demand in uncertain times, and pharma’s outperformance makes perfect sense.

-

Metal (+2.04%): Hindalco hit a fresh 52-week high at ₹1,104, up 2.88%. JSW Steel rose 1.85% to ₹1,298.50, also a new 52w high. Vedanta climbed 4.99% despite being oversold (RSI 21.42) — volume ran 1.84x average as bottom-fishers pounced. A weaker rupee boosts export realisations for metal producers. Commodity fundamentals remain mixed, but currency math tilts in their favour today.

-

PSU Bank (+1.37%): State Bank of India rose 1.26% to ₹982.30, though RSI sits at 24.38 (oversold). Credit growth narratives persist, but technical damage lingers. This is a sector trying to stabilise, not lead.

-

Bank Nifty (+1.26%) / Private Bank (+1.16%): HDFC Bank gained 2.73% to ₹770.10, volume 1.44x average — but it’s in a strong downtrend (RSI 44.07). ICICI Bank rose 1.06% to ₹1,248.70, RSI at 27.14 (oversold). Banks participated in the rally, but the technicals scream “not yet.” These are relief bounces, not reversals.

THE MIDDLE GROUND:

-

Media (+0.90%): Saregama exploded 15.15% to ₹385.80 on staggering volume — 17.17x its 20-day average. RSI at 64.7, above its 50-DMA. Something fundamental shifted here — content licensing deal? Streaming revenue spike? The data doesn’t say, but the volume does: institutional money arrived.

-

Realty (+0.77%): Steady, unspectacular. Knowledge Realty Trust raised ₹500 crore via commercial paper — the kind of quiet capital raise that signals confidence, not distress.

-

Energy (+0.65%): Reliance rose 0.71% to ₹1,368.50 on below-average volume. BPCL and IOC barely moved. This sector yawned through the rally.

-

Auto (+0.62%): Tata Motors CV reported a 70% jump in Q4 profit, but the sector stayed muted. Defensive, but not exciting.

-

FMCG (+0.34%): Godrej Industries surged 7.62% to ₹1,154.90, volume 8.47x average, RSI 64.88. Honasa Consumer appointed senior leaders to drive new brand building. The sector crawled higher, but select names sprinted.

THE LAGGARDS:

- IT (-1.99%): The day’s villain. Infosys fell 2.58% to ₹1,094.10 — a fresh 52-week low, RSI 35.31, in a strong downtrend. TCS dropped 1.01% to ₹2,249.90, RSI 27.03 (oversold). Wipro hit a 52w low at ₹188.10. LTM crashed 3.95% to ₹3,925, RSI 25.33 (oversold), volume 2.07x. Persistent fell 4.44%. Birlasoft hit a 52w low, RSI 12.52 (deeply oversold).

Why the carnage? Currency weakness hurts IT margins (they hedge dollar revenues). Fractal Analytics doubled Q4 profit, but the broader narrative remains: enterprise AI spending is shifting faster than Indian IT can pivot. The Nasdaq rose overnight, but India’s IT names sold off — a brutal divergence.

- Oil & Gas (+0.04%): Flatlined. Lower crude prices should help refiners, but the sector stayed asleep.

THEMATIC HIGHLIGHTS:

- India Manufacturing (+1.19%): Broad participation. Engineers India rose 6.15% on strong volume.

- Commodities (+1.04%): Metals led, energy lagged.

- Defence (+0.83%): HAL slipped 0.29% but remained overbought (RSI 70.87), volume 2.78x. GRSE fell 4.98%. Data Patterns dropped 4.14%. Defence stocks consolidated after recent runs — healthy.

- PSE (+0.31%): BHEL hit a 52w high at ₹414.60, up 2.66%. NLC India exploded 14.61% to ₹373.30 — volume through the roof. Public sector names are having a moment.

4. Beyond the Nifty 50 — Stories From the Broader Market

The real theatre played out beyond the blue-chip fortress:

-

Saregama (Media & Entertainment): ₹385.80 (+15.15%). Volume spiked 17.17x average — 38.7 million shares traded. Above its 50-DMA, RSI 64.7. This wasn’t noise. Institutions piled in. Content companies are benefiting from streaming wars and regional language demand. Watch for follow-through.

-

NLC India (Power Generation): ₹373.30 (+14.61%). Volume: 81.9 million shares. A state-owned thermal and renewable power producer catching a bid as India’s electricity demand surges. Renewable pivot stories are getting rewarded.

-

Adani Enterprises (Trading – Minerals): ₹2,719 (+8.85%). Fresh 52-week high. Volume strong. Adani Group names rallied across the board: Adani Green hit a 52w high at ₹1,418.60 (+3.80%, RSI 71.59), Adani Ports closed at ₹1,781 (+2.49%, 52w high). The group’s infrastructure and renewables pivot is back in favour.

-

Vedanta (Diversified Metals): ₹339.50 (+4.99%). RSI 21.42 (oversold), but volume ran 1.84x. At 77.6 million shares, this was the second-most active name by turnover. Below its 50-DMA but bouncing hard off technical support. Contrarian value play or dead-cat bounce? The next few sessions decide.

-

Bharti Airtel (Telecom): ₹1,883 (+5.24%). Volume spiked 2.35x. RSI 58.57. Tata Comm followed suit, rising 7.07% to ₹1,669 on 2.28x volume, RSI 70.59 (overbought). Telecom infrastructure plays are getting re-rated as 5G rollout accelerates.

-

BSE (Exchange and Data Platform): ₹4,045 (+4.02%). Fresh 52w high. RSI 85.37 (extremely overbought). Volume 1.69x. MCX followed: ₹3,360.10 (+4.87%), RSI 87.15, also a 52w high. India’s exchange operators are benefiting from retail participation mania — average daily turnover in NSE cash hit a 20-month high of ₹1,34,709 crore in April. These RSI levels scream caution, but momentum remains.

-

Kaynes Technology (Industrial Products): ₹3,332 (-20.26%). Volume exploded 6.64x — 10.6 million shares. RSI 28.32 (oversold), in a strong downtrend. A semiconductor and electronics manufacturer taking a savage hit. No news headline explains the move, but volume confirms distribution. Avoid until stabilisation.

-

Pine Labs (Fintech): ₹157.10 (-3.13%). Volume spiked 5.25x. RSI 23.94 (oversold). The fintech space remains under pressure as IPO dreams fade and valuations compress.

-

LIC Housing Finance: ₹562 (-4.04%). Volume 2.59x. RSI 57.52. Housing finance names sold off despite decent technicals — profit-taking after recent gains.

5. The Technical Picture

The cross signals today were rare but powerful:

GOLDEN CROSS WATCH:

– No explicit golden crosses flagged in today’s data, but several names are setting up: Adani Green, BSE, MCX all sit well above their 50-DMA and 200-DMA with strong uptrends intact.

DEATH CROSS ZONE:

– IT names dominate: Infosys, TCS, Birlasoft all in strong downtrends, below key DMAs. LTM is particularly ugly — RSI 25.33, price action broken.

OVERSOLD OPPORTUNITIES (RSI < 30):

– Kaynes (28.32): In a strong downtrend, volume spike confirms sellers remain. Wait.

– Vedanta (21.42): Below 50-DMA, but today’s 4.99% bounce on volume suggests capitulation buyers arrived.

– ICICI Bank (27.14): In downtrend but participated in today’s rally. RSI this low on a banking giant? Contrarians take note.

– SBI (24.38): Similar setup. Oversold, but downtrend remains.

– TCS (27.03): Oversold, but fighting its 200-DMA. Earnings season will decide if this is a buy or a trap.

OVERBOUGHT CAUTION (RSI > 70):

– BSE (85.37): Parabolic. Momentum players only.

– MCX (87.15): Same story. These are chase trades, not buy-and-hold setups.

– HFCL (88.38): Telecom infrastructure name stretched to extremes. RSI this high rarely ends well.

– Cipla (71.74): Justified by fundamentals and volume, but near-term pullback likely.

– HAL (70.87): Defence consolidation continues. Volume 2.78x confirms institutional interest, but give it room.

VOLUME SPIKES (>2x average):

– Saregama (17.17x), Caplipoint (11.66x), Godrej Ind (8.47x), Kaynes (6.64x), Pine Labs (5.25x), Zydus (4.92x), Cipla (4.02x), HAL (2.78x). These are “something happened” flags. In Saregama and Cipla, volume confirmed bullish breakouts. In Kaynes and Pine Labs, volume confirmed distribution. Context matters.

6. AI Signals — BUY / HOLD / SELL

| Stock | Signal | Reason |

|---|---|---|

| Cipla | BUY | Above 50-DMA, RSI 71.74 (strong but not extreme), vol 4.02x avg on breakout move |

| Zydus Life | BUY | Above 50-DMA, RSI 65.1 (healthy uptrend), vol 4.92x, acquisition news catalyst |

| Saregama | BUY | Above 50-DMA, RSI 64.7 (neutral), vol 17.17x — institutional accumulation confirmed |

| Bharti Airtel | BUY | Above 50-DMA, RSI 58.57 (room to run), vol 2.35x, sector strength intact |

| Adani Green | HOLD | Strong uptrend, 52w high, but RSI 71.59 overbought; let it consolidate |

| HAL | HOLD | Above 50-DMA, RSI 70.87 overbought, vol 2.78x; defence sector consolidating |

| BSE | SELL | RSI 85.37 extremely overbought, 52w high; parabolic moves don’t last |

| MCX | SELL | RSI 87.15 extremely overbought, 52w high; take profits before reversion |

| Kaynes | SELL | Strong downtrend, RSI 28.32 oversold but vol 6.64x confirms distribution |

| Infosys | HOLD | 52w low, RSI 35.31, strong downtrend; oversold but no reversal signal yet |

| TCS | HOLD | RSI 27.03 deeply oversold, but strong downtrend intact; wait for volume confirmation |

| Vedanta | HOLD | RSI 21.42 oversold, bounced 4.99% today, but below 50-DMA; needs follow-through |

7. Tomorrow’s Setup — Global Cues & Calendar

The overnight tape leans cautiously positive:

- US equities: Nasdaq +1.20%, S&P 500 +0.58%, Dow -0.14%. Tech strength abroad, but India’s IT names didn’t follow. Divergence continues.

- Asian cues: Nikkei -0.98%, Hang Seng flat, ASX +0.12%. Mixed signals. GIFT Nifty mirrors today’s close at 23,689.60 — expect a flat-to-mildly-positive open.

- Crude: Brent at $104.35, WTI $99.87. Lower oil supports Indian equities by easing import bills and inflation fears.

- Currency: USD/INR at 95.75, another lifetime low. Exporters benefit, but RBI may intervene if rupee weakness accelerates.

- Gold: $4,706.60 (+0.19%). Safe-haven bid remains, but not screaming panic.

Key Nifty levels for Friday:

– Support: 23,426 (today’s low). Break below invites retest of 23,300.

– Resistance: 23,777 (today’s high). Clear this, and 24,000 comes into view.

Bank Nifty:

– Support: 53,191 (today’s low).

– Resistance: 54,393 (today’s high). Banks need follow-through to confirm reversal.

Watch for:

– Any RBI commentary on rupee intervention.

– FII flow data for the week (Friday release).

– IT sector earnings guidance revisions — this will determine if the 52w lows are capitulation or the start of a deeper correction.

8. The Honest Take

For long-term investors: Today was a reminder that markets don’t move in straight lines. Pharma and metals rallied on currency tailwinds. IT bled on structural fears. The rupee hitting fresh lows is a symptom of global dollar strength and persistent FII selling — but it’s also a lever that benefits exporters. If you’re building a portfolio, this divergence creates opportunities: pharma at reasonable valuations, oversold IT giants trading below historical averages, and metal names benefiting from commodity cycles and currency math. Don’t chase the overbought exchange operators or parabolic telecom infra plays. Accumulate quality on pullbacks. India’s growth story hasn’t changed; valuations have simply compressed to reflect reality.

For active traders: Today’s breadth was real, but so is the technical damage in IT and select financials. The oversold names — TCS, Infosys, ICICI Bank, SBI — are tempting, but RSI below 30 doesn’t guarantee a bounce. Wait for volume confirmation and reversal candles. On the long side, pharma and metals have momentum; trade with tight stops. Saregama’s 17x volume spike is intriguing but risky — let it digest before chasing. The overbought exchange plays (BSE, MCX) are profit-taking candidates, not new longs. The VIX falling below 19 suggests fear is draining, which supports continued upside — but that also means complacency can return. Stay nimble.

“The stock market is filled with individuals who know the price of everything, but the value of nothing.” — Philip Fisher

Disclaimer: This blog is for informational and educational purposes only. It is not investment advice. All figures cited reflect publicly reported data for the trading session indicated. Markets are subject to risk; please consult a SEBI-registered advisor before acting on any view expressed here.