Unified Stocks — Friday, May 15, 2026

1. The Opening Scene

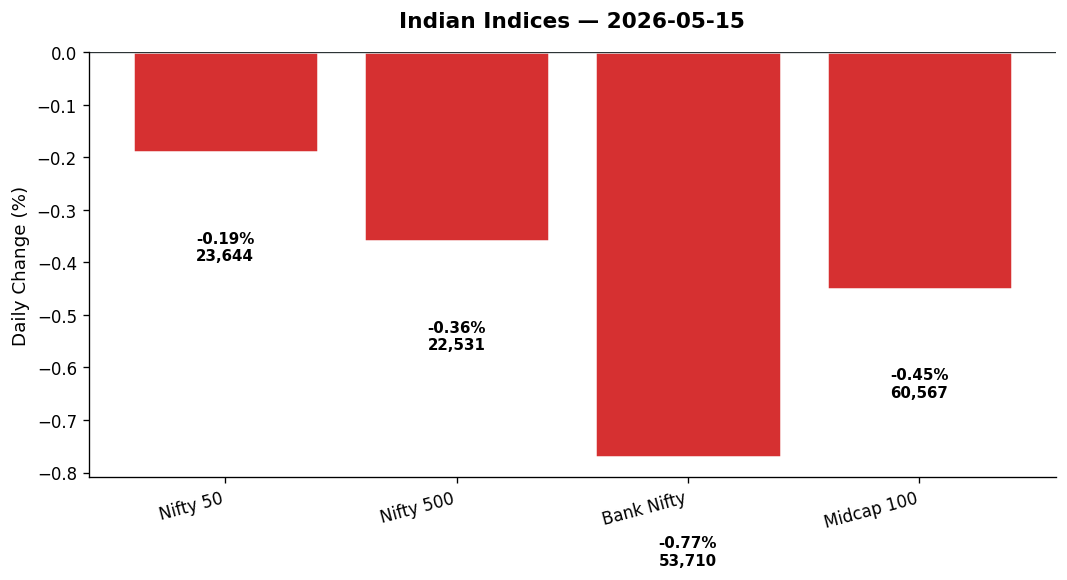

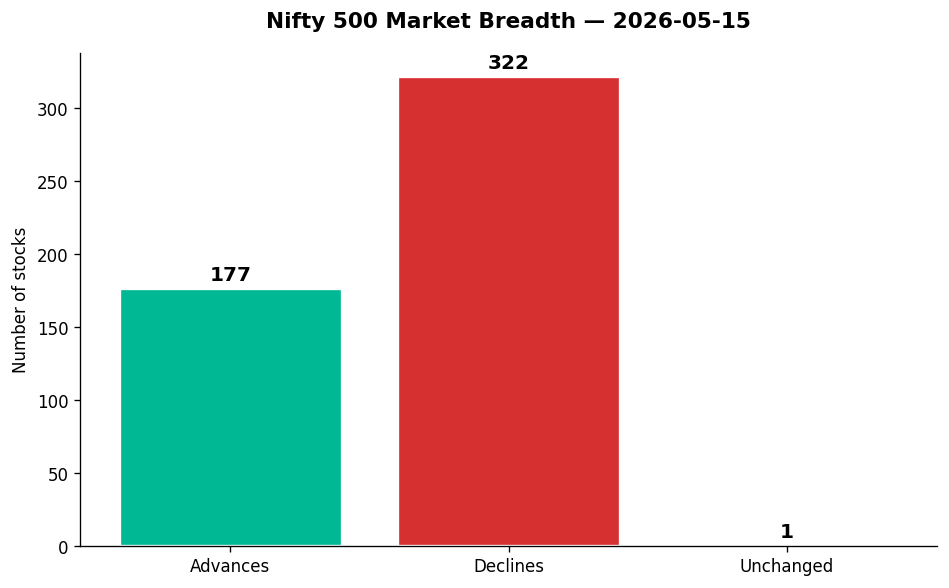

The market opened its eyes on Friday morning with the memory of Thursday’s sugar rush still fresh — but by the closing bell, reality had delivered a sobering slap. The Nifty 50 dipped 46 points to 23,643, a modest 0.19% retreat that masked far deeper fractures beneath the surface. Bank Nifty bled 418 points, down 0.77%, dragging financials into the red. Meanwhile, the broader Nifty 500 told the real story: 322 declines against just 177 advances. This was not a correction; it was a clash of narratives — media and IT soaring on AI optimism, while metals, energy, and realty crumbled under the weight of a strengthening rupee, surging crude oil (Brent up 2.2% to $108), and faltering sentiment in cyclicals. The VIX ticked up 0.95% to 18.79, whispering caution. If Thursday was the Ferrari revving, Friday was the speed bump.

2. The Forces That Drove the Day

Four forces collided to shape Friday’s session — and none of them played nice together:

-

Global crosscurrents: US markets closed strong overnight (S&P +0.77%, Nasdaq +0.88%), buoyed by optimism around the Trump-Xi summit and progress on trade talks. But by morning, Asian markets had soured — Nikkei down 1.99%, Hang Seng off 1.62%, DAX plunging 1.94%. The GIFT Nifty signalled a flat open at 23,643, which proved prescient. Investors were caught between Wall Street’s ebullience and Asian anxiety.

-

Crude oil’s violent spike: Brent crude surged 2.2% to $108.05 on geopolitical tensions following an attack on an Indian-flagged vessel off the Oman coast. India condemned the assault; all crew members were safe, but the incident rattled energy markets. WTI crude, oddly, fell 1.44% to $99.71 — a divergence that suggested supply chain fears in the East, not global demand. Oil & Gas stocks bore the brunt: Nifty Oil & Gas down 1.67%, Energy down 0.66%. Refiners like Reliance (-1.67%) and IOC slumped.

-

Rupee weakness and inflation worries: The rupee slipped 0.13% to ₹95.82 per dollar, a fresh multi-week low. BusinessLine headlines flagged “rupee woes” offsetting trade optimism. With crude spiking and the currency sliding, import-heavy sectors (auto, metals, consumer durables) faced margin compression fears. Gold, meanwhile, tumbled 2.7% to $4,551 — risk-off turned risk-confused.

-

Breadth collapse despite star performers: Despite headline index stability, market internals were weak. The Nifty 500’s 322:177 decline-advance ratio was brutal. Even the midcap index fell 0.45%, shedding ₹272 points. Yet, pockets of frenzy emerged: Saregama (+4.59%) traded ₹38,500 crore in value on 13.6x normal volume. Chamberlain Fertilizers (+6.51%) exploded on 9.7x volume. The market was rotational, not directional.

3. A Walk Through the Sectors

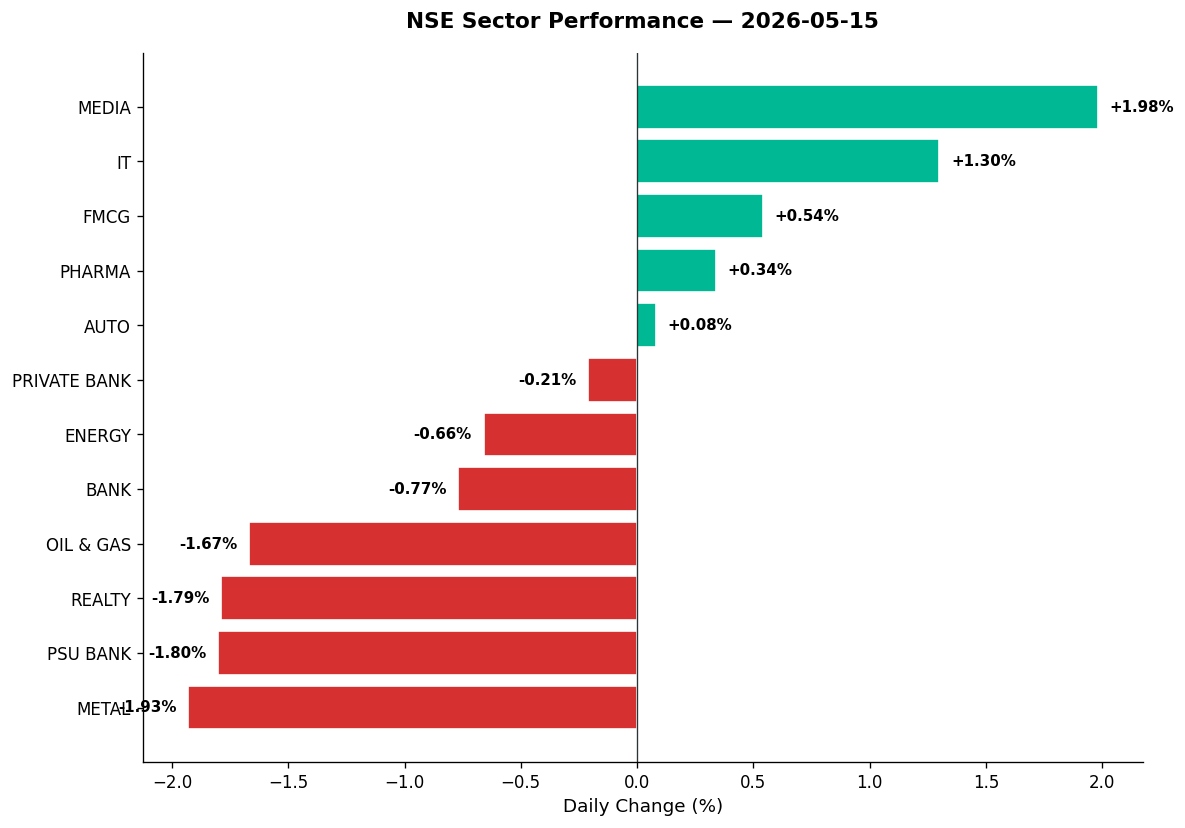

Friday belonged to the storytellers and the code-cutters. Here’s how the sectoral leaderboard shook out:

Leaders:

– Media (+1.98%): Saregama stole the show, surging 4.59% on extraordinary volume (95.6 crore shares, 13.6x average). The music and film IP play is riding a wave of AI-driven content monetisation buzz — expect more on this theme. Media’s resurgence after months of underperformance suggests institutional rotation into defensives-with-growth.

– IT (+1.30%): Infosys (+1.92%), Latent View (+5.06% on 6.6x volume), and the Nifty IT index all rebounded despite three prior sessions of decline. Yet, Times of India headlines warned of “AI worries mounting” — client spending remains muted, and disruption fears linger. This rally feels like a relief bounce, not a reversal.

– FMCG (+0.54%): Marico hit a fresh 52-week high at ₹843 (+0.96%). Defensive rotation is real. When crude spikes and volatility rises, investors flee to toothpaste and tea.

– Pharma (+0.34%): Sun Pharma (+0.79%), Biocon (+2.72%), and Lauruslabs (flat) all touched 52-week highs. The sector is in a stealth bull run — global supply chain shifts, China+1 tailwinds, and steady US demand are driving this. Watch Lupin and Aurobindo for breakout setups.

– Auto (+0.08%): Barely green. Tata Motors PV reported a 32% YoY profit drop in Q4 (₹5,783 crore), though it declared a ₹3/share dividend. Apollo Tyres hit a 52-week low at ₹394.75 (-1.75%), signalling demand concerns. The sector is stuck in neutral.

Laggards:

– Metal (-1.93%): A bloodbath. Hindalco (-5.45%), Vedanta (-2.63% to ₹330, RSI oversold at 18.57), Hindustan Zinc (-4.97%), and Sarda Energy (-3.55%, RSI 17.02) all crumbled. JSW Steel reported Q4 profit up 11x YoY to ₹16,370 crore — a stunning beat — yet the stock couldn’t hold gains as macro headwinds (stronger rupee, inventory fears) weighed. Metals need a weaker INR and stronger China PMI to revive.

– PSU Bank (-1.80%): State Bank of India (-0.10%) is now deeply oversold (RSI 19.34), trading below its 50-DMA. PSU banks are caught in a sentiment vortex: weak credit growth, asset quality whispers, and FII selling.

– Realty (-1.79%): DLF and the broader index slumped. Rising rates and funding cost fears are back.

– Oil & Gas (-1.67%): Despite crude’s spike, refiners fell. Reliance (-1.67%), IOC, and BPCL all declined. The logic: higher input costs + weak refining margins + inventory losses. This sector wants stable crude, not volatile crude.

– Bank Nifty (-0.77%): ICICI Bank (+0.15%) is oversold (RSI 28.88, strong downtrend). HDFC Bank (+0.06%) is trapped in a downtrend (RSI 41.16). Private banks are underperforming despite decent Q4 earnings. The rupee’s slide and NPA concerns are re-emerging.

– Energy (-0.66%): NTPC, Power Grid, and Adani Green all fell. The thematic India Energy index echoed the pain.

Thematics:

– Defence (-1.84%): HAL (-5.01%), Mazagon Dock, and BEL all retreated. Defence had a monster 2025; profit-taking after fiscal year-end is natural.

– Manufacturing (-0.70%): Kaynes Technology (-1.81%) missed Street estimates and FY26 guidance, sending shockwaves. Electronics manufacturing optimism is facing execution reality checks.

– Commodities (-1.29%): Weak across the board — metals, energy, and agri all fell.

4. Beyond the Nifty 50 — Stories From the Broader Market

Friday’s real action happened in the trenches, far from the Nifty 50 marquee. Here are the standouts:

- Kirloskar Brothers (+9.17% to ₹1,743): The compressors and pumps specialist surged on 4.4x volume. Strong uptrend, RSI 55.82 (neutral). Infrastructure and water management themes are back in vogue.

- Carborundum Universal (+6.52% to ₹1,105): Abrasives play jumped on 8.4x volume but is now overbought (RSI 78.21). Book profits if you hold this — momentum is stretched.

- Chambal Fertilizers (+6.51% to ₹452.25): The agri-input name exploded on 9.7x volume (RSI 52.16). Monsoon expectations and subsidy clarity are driving this.

- JP Power (+6.10% to ₹18.95): Power generation stock rose on massive volume (738 million shares). Technical data incomplete, but this is a speculative momentum play.

- Vijaya Diagnostic Centre (+5.84% to ₹1,344): Healthcare services provider rallied on normal volume. RSI 77.74 (overbought), strong uptrend. Diagnostics are in a secular growth phase.

- Tata Motors DVR (TMPV) (+5.14% to ₹356.15): The DVR shares rallied on 5x volume despite weak PV earnings. RSI 53.52 (neutral). This is a deep value bet on Tata Motors’ turnaround — but execution risk remains.

- Latent View (+5.06% to ₹305): The analytics and AI consulting name surged on 6.6x volume (RSI 56.95). AI hype is real, and Latent View is riding it hard.

- Saregama (+4.59% to ₹402.20): Already covered — the day’s volume king. RSI 69.08 (neutral), strong momentum. Content monetisation is the new gold rush.

- Great Eastern Shipping (+4.43% to ₹1,550.70): Shipping stocks are catching a global trade optimism bid. Volume 9.4x average, RSI 61.72. Strong uptrend.

On the losers’ side:

– Navabharat Ventures (NAVA) (-11.03% to ₹626): Power generation stock collapsed on 3.75x volume despite a strong uptrend. RSI 40.13. Likely profit-booking after a sharp run-up.

– HUDCO (-7.81% to ₹205.90): The housing finance institution fell on 2x volume. RSI 42.29. Concerns over real estate funding cycles.

– Muthoot Finance (-6.29% to ₹3,309): NBFC slumped on 6.6x volume, now below its 50-DMA (RSI 40.35). Gold loan NBFCs face margin pressure as gold prices correct.

– HAL (-5.01% to ₹4,377): Defence bellwether fell on 1.8x volume despite decent fundamentals. RSI 53.81. This is profit-booking, not a breakdown — watch for re-entry at ₹4,200.

– Vedanta (-2.63% to ₹330): The diversified metals giant is now deeply oversold (RSI 18.57, below 50-DMA). Volume 1.27x. This is a contrarian buy zone for risk-takers — but wait for RSI to bottom above 20.

– Travel Food Services (-4.63% to ₹1,091.30): Restaurant chain in strong downtrend, RSI 16.67 (oversold). Volume 2.6x. Avoid — this needs a catalyst to reverse.

52-week highs and lows:

– Highs: Sun Pharma, Biocon, Lauruslabs, Marico — pharma and FMCG defensives leading.

– Lows: Apollo Tyres, Naukri (-1.15% to ₹927), KFintech, Dalmia Bharat, United Breweries — cyclicals and tech platforms under pressure.

5. The Technical Picture

Friday’s technicals painted a market in turmoil — not crash territory, but decision fatigue:

-

Oversold names (RSI < 30): SBI (RSI 19.34), Vedanta (RSI 18.57), ICICI Bank (RSI 28.88), Sarda Energy (RSI 17.02), Travel Food (RSI 16.67). These are either value traps or contrarian buys. SBI and ICICI Bank stand out — both are below their 50-DMAs but fundamentally sound. Wait for RSI to tick up above 25 before entering.

-

Overbought names (RSI > 70): BSE (RSI 79.7, strong uptrend), Vodafone Idea (RSI 89.18 — absurd, avoid), Solar Industries (RSI 78.38, 3.8x volume), Carborundum Universal (RSI 78.21), RR Kabel (RSI 80.79). These are momentum exhaustion zones. Book profits.

-

Volume spikes (>2x): Saregama (13.6x), Chambal Fertilizers (9.7x), Great Eastern Shipping (9.4x), Carborundum (8.4x), Sailife (7.6x down — bearish), Latent View (6.6x), Muthoot Finance (6.6x down — bearish), TMPV (5x). Volume confirms conviction. Bullish spikes in Saregama, Chambal, and Latent View are actionable. Bearish spikes in Muthoot and Sailife are red flags.

-

No golden crosses or death crosses today — market is in consolidation mode, not trend shift.

6. AI Signals — BUY / HOLD / SELL

| Stock | Signal | Reason |

|---|---|---|

| LATENTVIEW | BUY | Above 50-DMA, RSI 56.95 (neutral), vol 6.6x avg — AI consulting momentum intact |

| GESHIP | BUY | Strong Uptrend, RSI 61.72, vol 9.4x avg — shipping cycle turning |

| CHAMBLFERT | BUY | Above 50-DMA, RSI 52.16, vol 9.7x avg — agri-input demand spike |

| KIRLOSENG | BUY | Strong Uptrend, RSI 55.82, vol 4.4x avg — infrastructure play gaining traction |

| VEDL | HOLD | Below 50-DMA, RSI 18.57 (oversold), vol 1.27x — wait for RSI stabilisation above 20 |

| SBIN | HOLD | Below 50-DMA, RSI 19.34 (oversold), vol 1.45x — fundamentally sound but needs sentiment shift |

| ICICIBANK | HOLD | Strong Downtrend, RSI 28.88 (oversold), vol 0.69x — oversold but trend not broken yet |

| HAL | HOLD | Above 50-DMA, RSI 53.81, vol 1.8x — profit-booking, not breakdown; watch ₹4,200 support |

| CARBORUNIV | SELL | Above 50-DMA, RSI 78.21 (overbought), vol 8.4x — momentum exhausted, book profits |

| MUTHOOTFIN | SELL | Below 50-DMA, RSI 40.35, vol 6.6x down — bearish breakdown on volume |

| IDEA | SELL | Strong Uptrend, RSI 89.18 (extreme overbought), vol 2.2x — unsustainable euphoria |

| NAVA | SELL | Strong Uptrend, RSI 40.13, vol 3.75x down — sharp reversal after run-up, exit on bounce |

7. Tomorrow’s Setup — Global Cues & Calendar

Monday’s opening will hinge on how global markets digest Friday’s mixed tape:

-

US close (Thursday night): Dow +0.75%, S&P +0.77%, Nasdaq +0.88%. Wall Street is pricing in trade deal optimism and AI earnings beats. But US markets were closed for the session when Asia tanked Friday — expect a catchup correction Monday morning in US futures.

-

Asian close (Friday): Nikkei -1.99%, Hang Seng -1.62%, ASX -0.11%. The selloff was broad-based — Japan and Hong Kong leading losses. If Asian futures open weak Sunday night, expect India to gap down.

-

GIFT Nifty: Flat at 23,643. No early signal for Monday’s open — markets are in wait-and-see mode.

-

Commodities: Brent crude at $108.05 (up 2.2%) is the wildcard. If geopolitical tensions ease over the weekend, crude could retreat, helping Indian energy and auto stocks. Gold at $4,551 (down 2.7%) suggests risk-on sentiment is fragile.

-

Currency: USD/INR at ₹95.82 (up 0.13%). A weaker rupee hurts importers (tech, auto, consumer durables) but helps exporters (IT, pharma, textiles). Watch for RBI intervention signals.

Key technical levels for Monday:

– Nifty 50: Support at 23,610 (Friday’s low), resistance at 23,839 (Friday’s high). A break below 23,600 opens 23,400; a break above 23,850 targets 24,000.

– Bank Nifty: Support at 53,628 (Friday’s low), resistance at 54,325 (Friday’s high). Watch 53,500 — a breakdown there accelerates selling.

– Nifty 500: Support at 22,502 (Friday’s low). Breadth needs to improve — watch for 200+ advances to confirm any rally.

Macro watch: No major India data releases Monday, but global trade headlines (Trump-Xi follow-up) and crude oil supply news will dominate sentiment.

8. The Honest Take

For long-term investors: Friday’s churn is noise. The real signal is in the 52-week highs list — pharma (Sun Pharma, Biocon, Lauruslabs) and FMCG defensives (Marico) are in stealth bull markets. Meanwhile, cyclicals (metals, energy, auto) are in drawdowns — Vedanta at RSI 18.57 and SBI at RSI 19.34 are near capitulation levels. If you have dry powder, accumulate quality cyclicals on this weakness. Ignore the daily headline drama. Three years from now, today’s ₹330 Vedanta or ₹961 SBI will look like gifts. Raamdeo Agrawal’s “Ferrari market” comment (Sensex to ₹3 lakh by 2036) isn’t hype — it’s math, compounded over time. Stay invested.

For active traders: Friday’s session was a masterclass in sector rotation. Media, IT, and pharma bid up; metals, banks, and energy sold off. The volume spikes in Saregama, Chambal, and Latent View are actionable momentum plays — but RSI discipline is critical (exit if RSI > 75). The oversold cluster (SBI, Vedanta, ICICI Bank) offers contrarian swing trades — but wait for RSI to turn up before entering. Don’t catch falling knives on volume. Monday’s open will set the week’s tone — if GIFT Nifty gaps down, fade the rally in overbought names; if it gaps up, chase oversold reversals. Trade the tape, not your emotions.

“The stock market is filled with individuals who know the price of everything, but the value of nothing.” — Phillip Fisher