Unified Stocks — Wednesday, May 13, 2026

1. The Opening Scene

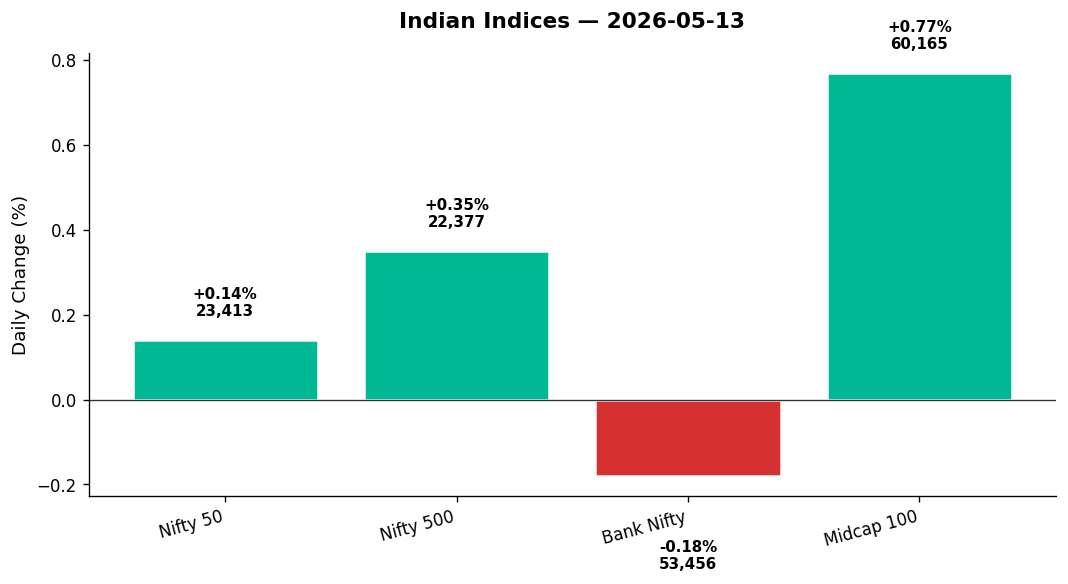

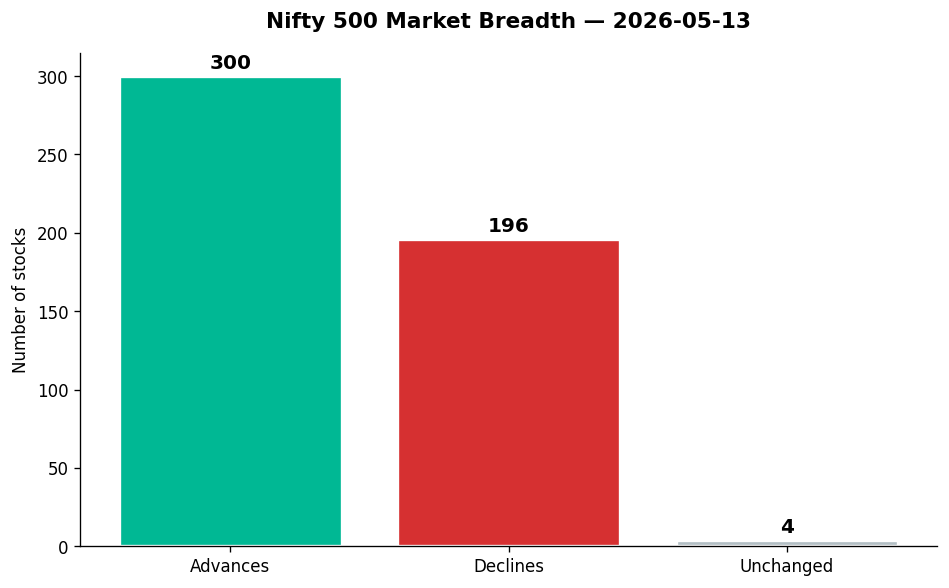

The Indian market on Wednesday resembled a tug-of-war match played in thick fog. Nobody could see the rope’s other end, yet everyone pulled with conviction. Metals gleamed. Banks stumbled. IT giants slid into fresh 52-week lows while defence stocks marched forward, buoyant and unshaken. By the closing bell, the Nifty 50 had inched up 33 points — a +0.14% gain that felt more like a survival badge than a triumph. The Sensex whispered higher. Bank Nifty whispered lower. And beneath the surface, the broader market — the Nifty 500, the midcaps, the forgotten warriors — outperformed with quiet ferocity, advancing 300 names against 196 declines.

This was not a day of clarity. It was a day of contradictions. Steel mills roared back to life with double-digit gains. IT bellwethers kissed multi-year lows. The rupee wobbled to fresh record depths at ₹95.69 against the dollar, while crude oil prices held steady near $107 Brent. Volatility, as measured by India VIX, ticked up 0.75% to 19.43 — not a panic signal, but a reminder that the market’s nerves remain frayed. And yet, domestic money kept flowing. The question isn’t whether India is resilient. It’s how long this resilience can defy the global headwinds.

2. The Forces That Drove the Day

Four forces shaped Wednesday’s mood, each pulling the market in a different direction:

-

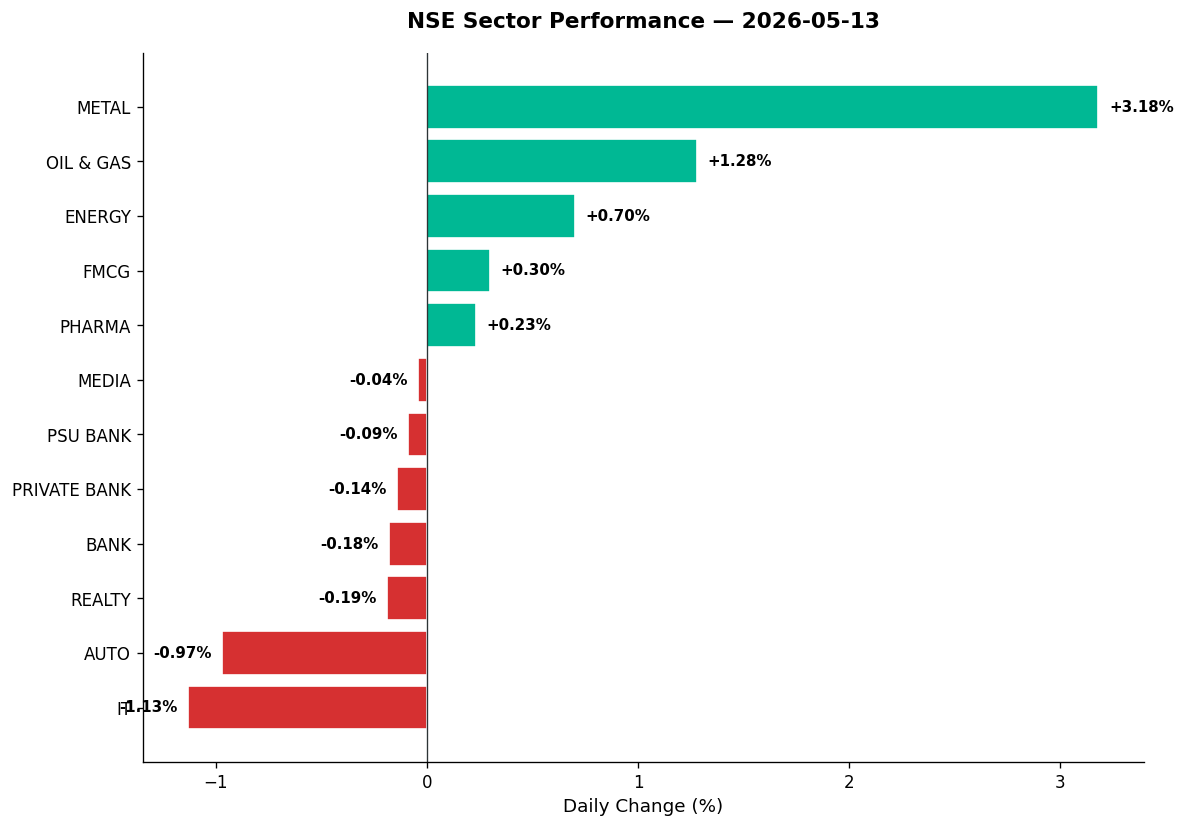

Metal mania: Steel and aluminium names surged on the back of global commodity strength and rumours of restocking demand. SAIL — the state-owned steel giant — rocketed +14.34% to a fresh 52-week high of ₹201.35, on volume 5.94 times its 20-day average. Tata Steel, Vedanta, and Hindalco joined the rally. The Nifty Metal index closed +3.18%, the session’s undisputed leader.

-

FII exodus, rupee rout: Foreign institutional investors continued their selling spree, pressuring the rupee to ₹95.69 per dollar — a fresh record low. The currency’s weakness stems from elevated crude prices (Brent at $107.66, WTI at $102.32) and geopolitical tensions in West Asia. Oil-importing nations like India are bearing the brunt, and the rupee’s slide is feeding back into market sentiment. Domestic flows — particularly SIPs and retail cash — are the only firewall.

-

IT carnage: The sector that powered India’s bull run for two decades is now its weakest link. Nifty IT fell -1.13%, dragged down by fresh 52-week lows in Infosys (₹1,123.40, -1.48%), TCS (₹2,274, -1.14%), Wipro (₹187.98, -0.84%), and HCL Tech (₹1,145, -0.07%). AI disruption fears — amplified by OpenAI’s latest moves — are haunting investor confidence. Birlasoft collapsed -4.13% to ₹317.90, its RSI at a bone-chilling 11.27, deep oversold territory.

-

Domestic resilience in defence and manufacturing: While global cues remained mixed (Nasdaq -0.71%, S&P 500 -0.16%), thematic indices tied to India’s capex story outperformed. Nifty India Defence rose +2.10%, Nifty PSE gained +1.18%, and Nifty India Manufacturing added +0.72%. BHEL hit fresh 52-week highs at ₹405. This is domestic demand asserting itself in a world that’s retreating.

The market breadth told the real story: 300 advances versus 196 declines across the Nifty 500. Midcaps rose +0.77%, outpacing the Nifty 50. This was a stock-picker’s session, not a passive index day.

3. A Walk Through the Sectors

Leaders (green and proud):

-

Nifty Metal (+3.18%): The day’s undisputed champion. SAIL’s +14.34% surge on 5.94x volume led the charge, followed by Tata Steel (+3.73%, fresh 52w high at ₹219.90), Hindalco (+3.61%, also at 52w highs, ₹1,079), and Vedanta (+6.20%, ₹323.95). Vedanta’s rally is notable: it’s still below its 50-DMA and deeply oversold (RSI 19.12), suggesting this bounce may be a dead-cat rally or the start of mean reversion. Steel Names Like India (NSLNISP) and Jindal Realty (JAINREC) rounded out the top gainers, up +5.97% and +5.91% respectively.

-

Nifty Oil & Gas (+1.28%): Higher crude prices lifted exploration and refining names. The sector gained ground despite Reliance Industries slipping -0.21% to ₹1,361.20 (trend: Strong Downtrend, RSI 53). Smaller oil plays benefited from the tailwind.

-

Nifty Energy (+0.70%): Power utilities held steady. NLC India surged +6.13% to ₹327, riding a strong uptrend (RSI 67.12). Torrent Power, however, collapsed -8.86% to ₹1,456, its RSI at 24.07 — one of the session’s worst performers.

-

Nifty FMCG (+0.30%): Consumer staples provided defensive cushioning. Asian Paints rose +4.37% to ₹2,615 on 3.17x volume — a sign of institutional interest. Berger Paints surged +5.06% on an astonishing 12.9x volume spike, closing at ₹512.80. When paint stocks move on volume, it’s usually a signal: either results are due, or large blocks are changing hands.

-

Nifty Pharma (+0.23%): Mixed but steady. Lauruslabs and Aurobindo Pharma hit fresh 52-week highs (₹1,281 and ₹1,499.90 respectively). But Cohance Lifesciences fell -5.71% to ₹457, and Neuland Labs slipped -2.36% despite being above its 50-DMA. The sector remains a stockpicker’s minefield.

The middling majority:

-

Nifty Media (-0.04%): Flat as a line. Sun TV dropped -4.59% to ₹534.50, RSI at 22.25 (oversold), volume 1.73x average.

-

Nifty PSU Bank (-0.09%): State-owned lenders tread water. SBI slipped -0.37% to ₹971, RSI at 23.42 (oversold), trending below its 50-DMA.

-

Nifty Private Bank (-0.14%): ICICI Bank fell -0.34% to ₹1,236.10, RSI at 19.91 — the most oversold major bank in India. HDFC Bank declined -0.17% to ₹749.15, RSI 34.14, also in downtrend. Private banks are under twin pressure: loan growth concerns and global banking jitters.

Laggards (red and struggling):

-

Nifty Realty (-0.19%): Property developers remain unloved. Data for specific names not available, but the sector’s weakness persists.

-

Nifty Auto (-0.97%): A rare weak day for the sector. No specific stock data provided, but the index’s decline suggests profit-booking after recent strength.

-

Nifty IT (-1.13%): The day’s biggest sectoral loser. The IT majors’ 52-week lows tell the story. Infosys, TCS, Wipro, HCL Tech — the quartet that built India’s services export empire — are now under siege. Birlasoft’s -4.13% crash to ₹317.90 (RSI 11.27, Strong Downtrend, volume 2.43x) is a microcosm of the sector’s pain. eClerx Services also tumbled -6.37% to ₹1,534.

4. Beyond the Nifty 50 — Stories From the Broader Market

Wednesday’s real action unfolded outside the blue-chip universe. Here are the names that moved markets, minds, and money:

-

SAIL (Iron & Steel): The session’s superstar. +14.34% to ₹201.35 on volume 5.94x its 20-day average. RSI: 73.51 (overbought), trend: Strong Uptrend. Fresh 52-week high. The question: is this a breakout or a blowoff top? Steel demand indicators remain mixed, but the technical setup is undeniably bullish.

-

Dixon Technologies (Consumer Electronics): +9.78% to ₹11,129, volume 3.72x average. RSI 53.79 (neutral), above 50-DMA. Dixon continues to ride India’s manufacturing wave. This is a play on electronics production linked incentives (PLI) and domestic demand.

-

Vodafone Idea (Telecom): +7.32% to ₹12.76 on volume 2.74x average. RSI: 88.42 — dangerously overbought. The rally followed clarifications on a treasury stock transfer report. Idea remains a speculative play; the overbought RSI suggests caution for chasers.

-

Vedanta (Diversified Metals): +6.20% to ₹323.95, volume 1.86x average. RSI: 19.12 (oversold), trend: below 50-DMA. This is a classic oversold bounce. Vedanta’s copper and aluminium exposure positions it for commodity rallies, but the technicals suggest this is a relief move, not a trend reversal. Yet.

-

Manappuram Finance (NBFC): +6.05% to ₹310.95, volume 1.56x average. RSI 61.23 (neutral), above 50-DMA. Gold loan NBFCs are benefiting from rising gold prices (₹4,689.90 per ounce, +0.26% globally).

-

Meesho (E-Commerce): +6.11% to ₹193, volume 0.59x average. RSI 56.41 (neutral). E-commerce names are finding a floor after months of underperformance. Meesho’s volume was below average, suggesting the move was broad-based sector strength, not news-specific.

On the losers’ bench:

-

Pine Labs (Fintech): -12.24% to ₹165 on volume 9.28x average. RSI: 25.79 (oversold). This is the session’s biggest loser by percentage, and the volume spike suggests something is afoot — possibly block deals or institutional exits. No news headline provided, but fintech names are under pressure globally.

-

Torrent Power (Integrated Utilities): -8.86% to ₹1,456, volume 1.89x average. RSI: 24.07 (oversold), below 50-DMA. A sharp fall on no obvious news. Technical damage is severe.

-

Birlasoft (IT Services): -4.13% to ₹317.90, volume 2.43x average. RSI: 11.27 — the most oversold name in the entire dataset. Strong Downtrend. If you believe in mean reversion, this is a candidate. If you believe in momentum, it’s a falling knife.

-

Swiggy (E-Commerce): -0.84% to ₹253.70, volume data not provided. Fresh 52-week low. Swiggy’s Q4 FY26 results showed a net loss of ₹800 crore, and brokerages flagged rising competition. The food delivery wars are heating up, and margins are getting squeezed.

-

Naukri (Internet Retail): -0.64% to ₹924.90. Fresh 52-week low. White-collar hiring slowdown in IT and services is weighing on InfoEdge’s flagship platform.

Honourable mentions:

-

Groww (Stockbroking): +3.12% to ₹188.80, volume 1.21x average. RSI: 28.13 (oversold). The discount brokerage platform is finding support near lows.

-

Berger Paints and Asian Paints: Volume spikes (12.9x and 3.17x respectively) on price gains suggest institutional repositioning ahead of earnings or results.

-

Defence stocks: BHEL, Mazagon Dock, BEL — all hit fresh highs or held strong. The Nifty India Defence index’s +2.10% rise reflects sustained optimism around India’s capex cycle.

5. The Technical Picture

Wednesday’s technicals revealed a market in flux, with extremes on both ends:

Oversold names (RSI < 30):

- ICICI Bank: RSI 19.91, Strong Downtrend. India’s second-largest private bank is deeply oversold.

- Vedanta: RSI 19.12, below 50-DMA. Bounce today, but trend is weak.

- SBI: RSI 23.42, below 50-DMA.

- Groww: RSI 28.13.

- Kalyankjil (Jewellery): RSI 26.23, Strong Downtrend, volume 4.94x average.

These are “something may be happening” signals — either capitulation or accumulation zones.

Overbought names (RSI > 70):

- Vodafone Idea: RSI 88.42, Strong Uptrend. Parabolic move; proceed with caution.

- HFCL (Telecom Infra): RSI 91.25, Strong Uptrend. Extreme overbought.

- MCX (Exchange): RSI 80.63, Strong Uptrend.

- BSE (Exchange): RSI 80.22, Strong Uptrend.

- SAIL: RSI 73.51, Strong Uptrend.

These names have strong momentum but carry pullback risk.

Volume spikes (>2x average):

- Berger Paints: 12.9x

- Pine Labs: 9.28x

- IIFL: 6.98x

- SAIL: 5.94x

- Neuland Labs: 5.93x

- Kalyan Jewellers: 4.94x

Volume is truth. When a stock moves on 5x volume, institutions are involved.

Death Cross alert:

- M&M Financial Services: 50-DMA crossed below 200-DMA today. Price: ₹320, -2.13%. RSI 60.55 (neutral), trend: above 50-DMA. This is a medium-term bearish signal, though the stock held above its 50-DMA for now.

Golden Cross events: None today.

6. AI Signals — BUY / HOLD / SELL

| Stock | Signal | Reason |

|---|---|---|

| SAIL | HOLD | Fresh 52w high, RSI 73.51 (overbought), vol 5.94x — momentum strong but extended |

| Vedanta | BUY | Oversold (RSI 19.12), volume 1.86x, metal rally tailwind — bounce candidate |

| ICICI Bank | BUY | RSI 19.91 (deeply oversold), Strong Downtrend but capitulation zone — contrarian entry |

| Groww | BUY | RSI 28.13 (oversold), volume 1.21x, at support — mean reversion play |

| Dixon Technologies | HOLD | Above 50-DMA, RSI 53.79 (neutral), vol 3.72x — strong but not overbought yet |

| Vodafone Idea | SELL | RSI 88.42 (extreme overbought), Strong Uptrend but parabolic — risk/reward poor |

| Birlasoft | BUY | RSI 11.27 (extreme oversold), vol 2.43x, Strong Downtrend — high-risk contrarian bet |

| Pine Labs | HOLD | RSI 25.79 (oversold), vol 9.28x — volume spike suggests event; await clarity |

| Asian Paints | BUY | Above 50-DMA, RSI 60.12 (neutral), vol 3.17x — institutional interest, trend intact |

| HFCL | SELL | RSI 91.25 (extreme overbought), Strong Uptrend — profit-booking zone |

| Tata Steel | HOLD | Fresh 52w high, RSI 63.85 (neutral), vol 1.93x — strong but not overextended |

| M&M Financial | HOLD | Death Cross today, RSI 60.55 (neutral) — watch for breakdown below 50-DMA |

7. Tomorrow’s Setup — Global Cues & Calendar

Global tape:

– US equities: Mixed. Dow +0.11%, S&P 500 -0.16%, Nasdaq -0.71%. Tech weakness in the US is spilling over into Indian IT.

– Asian markets: Nikkei +0.84%, Hang Seng +0.15%, ASX -0.46%. Tokyo’s strength is a positive, but China remains lukewarm.

– GIFT Nifty: +0.14% at 23,412.6 — suggesting a flat-to-marginally-positive open for Thursday.

– Crude oil: Brent -0.10% at $107.66, WTI +0.14% at $102.32. Oil remains elevated but stable. Any spike will hurt India.

– USD/INR: +0.32% at ₹95.69. Rupee weakness continues. RBI intervention likely if it crosses ₹96.

– Gold: +0.26% at $4,689.90. Safe-haven demand persists.

Key levels for Thursday:

– Nifty 50: Support at 23,263 (Wednesday’s low), resistance at 23,583 (Wednesday’s high). A move above 23,600 would be bullish; a break below 23,250 could test 23,000.

– Bank Nifty: Support at 53,194, resistance at 54,104. The index is range-bound and weak.

– Nifty 500: Outperforming. Support at 22,209, resistance at 22,532.

What to watch:

– FII flow data for Wednesday (released Thursday morning).

– Any RBI commentary on currency intervention.

– IT sector stabilisation — or further deterioration.

– Crude oil’s direction — a move toward $110 Brent would be rupee-negative.

8. The Honest Take

For long-term investors:

This is not the market to chase. But it’s also not the market to abandon. The divergence between domestic fundamentals and global sentiment has rarely been sharper. India’s manufacturing, defence, and infrastructure plays are holding firm, powered by capex and structural reform. The rupee’s weakness is painful but temporary — once crude stabilises, the currency will find a floor. Focus on quality: names with strong balance sheets, pricing power, and domestic exposure. Avoid overleveraged IT exporters until the AI disruption narrative clarifies. SIPs remain your best friend in volatile times.

For active traders:

Wednesday was a gift: oversold names with volume, overbought names with momentum, and clear sector divergence. SAIL and Vedanta are high-beta metal plays — ride the momentum, but don’t marry them. ICICI Bank at RSI 19.91 is a contrarian buy if you have the stomach for drawdowns. Vodafone Idea and HFCL are sells on overbought extremes. The IT sector is a falling knife — wait for RSI to climb above 30 and volume to stabilise before nibbling. The broader market (Nifty 500, midcaps) is outperforming the Nifty 50 — that’s where the next six months’ alpha lives.

“The ability to outperform in financial markets requires creativity, vision and the ability to see what others cannot.” — John Rogers