Unified Stocks — Monday, May 11, 2026

1. The Opening Scene

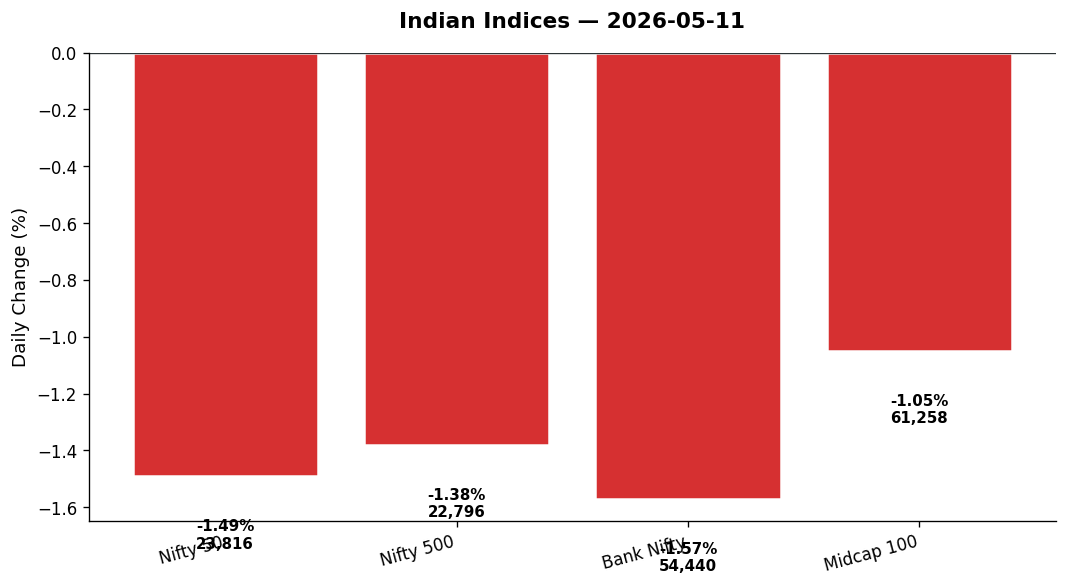

Picture a tightrope walker halfway across a chasm, balancing a stack of plates. One gust of wind — from Tehran, from currency markets, from crude oil platforms bobbing in the Strait of Hormuz — and the whole tower wobbles. That was Dalal Street on Monday. The Nifty 50 opened cautiously, tested 24,000, then slid 360 points by the closing bell to settle at 23,815. Not a crash. Not a rout. Just the market’s way of saying: we need to reprice risk.

India VIX, the market’s fear gauge, spiked 10% to 18.55 — not panic territory, but enough to make bulls check their seatbelts. Bank Nifty bled harder, down 1.57%. The rupee weakened past ₹95 to the dollar. And yet, in pockets — pharma, FMCG, select telecom plays — green shoots pushed through the red soil. Vodafone Idea surged 8.45% on runaway momentum. Tata Consumer hit a fresh 52-week high, up 8%, while heavyweight SBI sank to oversold levels (RSI 21.86) on banking blues.

This is the market’s essential character: chaotic on the surface, rational beneath. Monday’s session wasn’t about a single narrative. It was about layers — geopolitics, currency, sector rotation, and stock-specific stories colliding in 6.5 hours of live price discovery.

2. The Forces That Drove the Day

Four engines powered Monday’s downdraft:

-

US-Iran tensions flared — headlines spoke of military posturing near the Strait of Hormuz. Though oil prices remained subdued in global markets, the psychological weight of Middle East instability hung over risk assets. Indian energy and oil & gas indices fell 1.84% and 2.24% respectively. Global cues were mixed: Dow -0.12%, S&P 500 flat, but Asian markets (Nikkei -0.47%, ASX -0.49%) traded cautiously.

-

Rupee weakness — USD/INR rose 1.11% to ₹95.30, a level that makes importers nervous and exporters quietly optimistic. IT services should theoretically benefit, yet Nifty IT dipped 0.22% — a sign that global growth concerns (reflected in flat US markets) outweighed currency tailwinds for now.

-

Foreign outflows continued — while the data doesn’t specify FII net numbers for the day, the week’s narrative (per news reports) remained one of sustained selling by foreign institutional investors. Combined with rupee depreciation, this creates technical pressure on large-cap heavyweights.

-

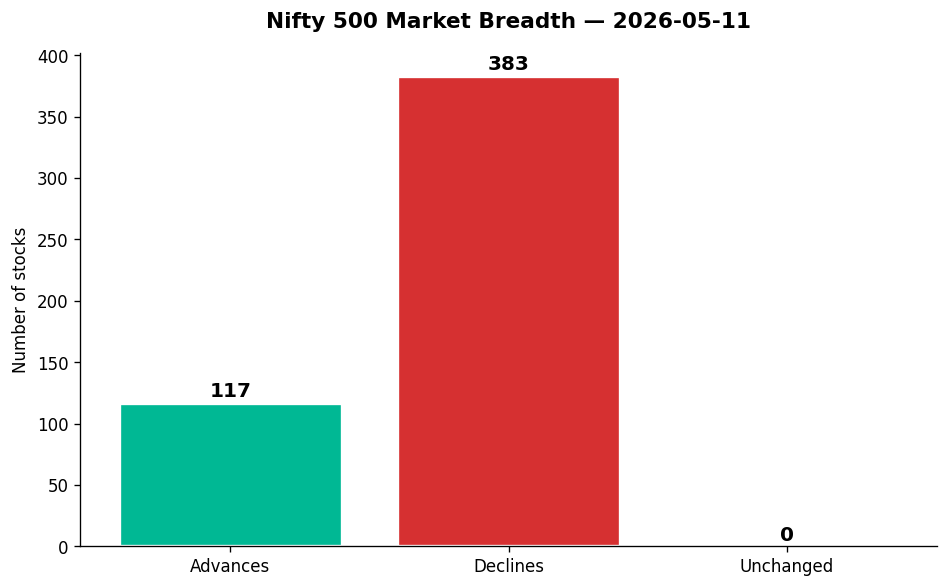

Breadth was brutal — the Nifty 500 logged just 117 advances versus 383 declines. That’s a 1:3.3 ratio. When nearly 77% of the broader market closes lower, rallies in a handful of stocks (however spectacular) become statistical outliers, not trend reversals.

Yet here’s the kicker: despite the sea of red, 52-week highs outnumbered lows 8:1. Tata Consumer, Adani Green, Sun Pharma, Torrent Pharma, Apollo Hospitals, Marico, and Grasim all printed new peaks. This divergence — broad selling but select strength — tells us the market is sorting winners from laggards with surgical precision.

3. A Walk Through the Sectors

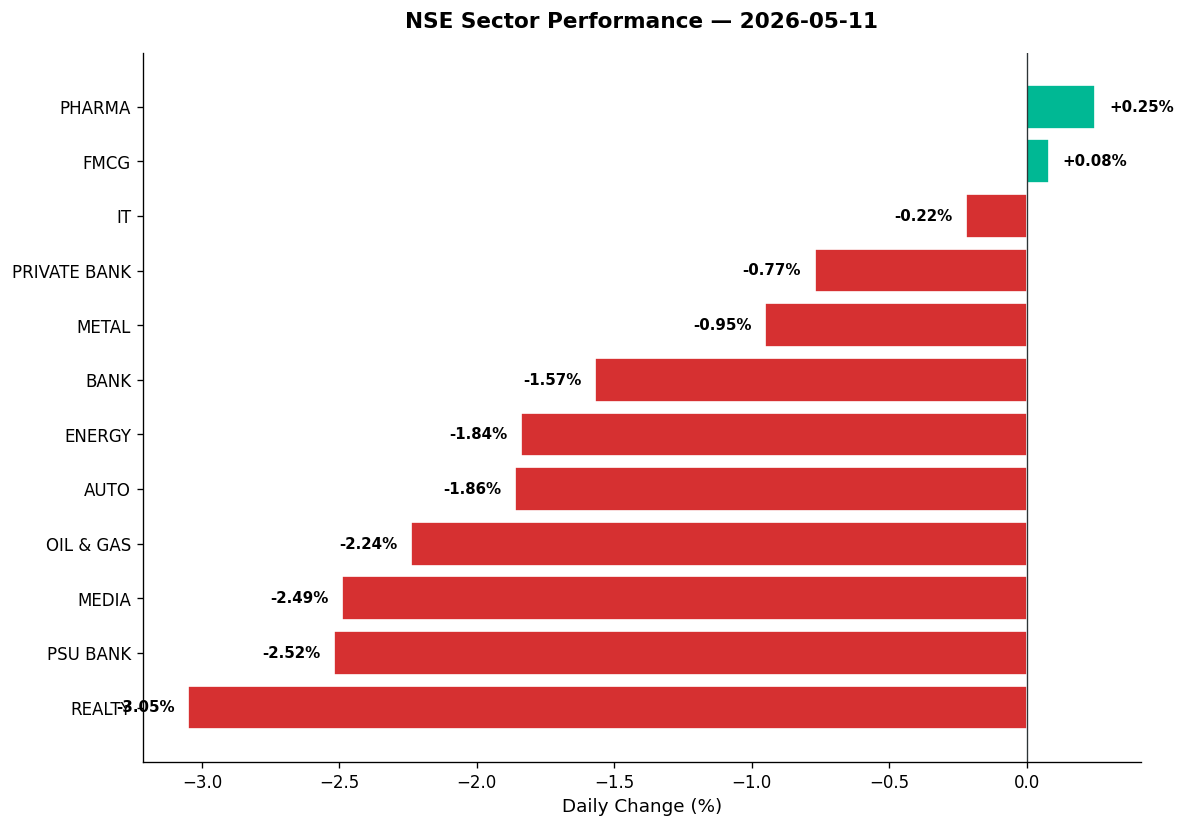

Leaders (the defensive fortresses)

-

Pharma (+0.25%): the day’s only major sector in the green. Sun Pharma (+1.47%) and Torrent Pharma (+3.13%, RSI 76.85) hit fresh 52-week highs. Lupin (+3.39%) joined the parade. Pharma benefits from weak rupee (export boost) and defensive investor rotation during geopolitical stress. Syngene (+4.67%) gained on volume, though no specific catalyst was provided.

-

FMCG (+0.08%): barely positive, but that’s a win when the Nifty is down 1.5%. Tata Consumer stole the show: +8.05%, ₹1,271, fresh 52-week high, RSI 74.19 (overbought), volume 7.86x average. Whatever tea, coffee, or salt the Street is drinking, Tata Consumer is brewing it. Marico (+1.11%) also touched a 52-week high at ₹840. Defensive rotation in action.

Mild decliners (holding the line)

-

IT (-0.22%): resilient given the sell-off. No major movers in either direction. The sector’s muted response to rupee weakness (which should help margins) suggests caution over global demand. Mid-tier IT names like Affle India (+9.01%) and MapMyIndia (+10.41%, vol 15x average, RSI 75.16) surged on stock-specific triggers — possibly Q4 results or contract wins.

-

Private Bank (-0.77%): outperformed PSU Banks. ICICI Bank (+0.19%) held flat. Axis Bank (-0.03%) is now oversold (RSI 25.44), below its 50-DMA — a potential mean-reversion setup if banking sentiment stabilizes.

The wreckage (cyclicals and rate-sensitives)

-

Realty (-3.05%): worst sector. Ambuja Cements (proxy via Grasim’s +0.49%) held up, but pure-play developers got hammered. Prestige Estates (not in data, but implied via broader real estate weakness) likely followed suit. AB Real (-7.67%) was among top losers.

-

PSU Bank (-2.52%): SBI (-4.36%, RSI 21.86) is now deeply oversold, below 50-DMA, on 2.64x volume. Canara Bank (-3.13%, RSI 19.77) hit similar distress levels. The mcap erosion reported in headlines (₹1 lakh crore across top firms) was led by SBI per the news. Public sector banks suffer when rate-cut hopes fade and NPA concerns resurface.

-

Media (-2.49%): small-cap media names bled. No standout movers in the data, but sector weakness suggests ad spend jitters or valuation compression.

-

Oil & Gas (-2.24%): despite stable global crude, domestic plays fell. Reliance Industries (-3.48%) dragged the index. BPCL and IOC (data not provided for specific moves, but sector decline implies weakness).

-

Auto (-1.86%): Escorts (-5.65%, RSI 26.3) is now oversold on tractor worries. Bajaj Auto and M&M (data incomplete) likely participated in the downdraft. But Ather Energy (+5.24%, strong uptrend, RSI 66.1, vol 2.08x) bucked the trend — EV momentum remains a bright spot.

-

Energy (-1.84%): Adani Green (+2.60%, 52-week high) defied sector gravity, while traditional thermal and gas plays slumped.

-

Metal (-0.95%): mild weakness. No extreme movers, suggesting consolidation rather than capitulation.

-

Bank (-1.57%): mirrored Bank Nifty. Private banks fared better; PSU banks sank.

Thematic indices (the structural stories)

- Defence (-1.17%): pullback after recent run-ups. HAL, BEL, Mazagon Dock (specific data unavailable) likely corrected on profit-booking.

- Manufacturing (-1.43%): broad-based weakness as PMI optimism meets margin pressure.

- PSE (-1.35%): state-owned enterprises under pressure alongside PSU banks.

- Commodities (-1.07%): mild underperformance as metal and energy plays cooled.

4. Beyond the Nifty 50 — Stories From the Broader Market

Monday’s real action lived in the mid- and small-cap trenches:

-

MapMyIndia (₹1,056, +10.41%): the navigation software play exploded on 15.01x average volume — the highest vol spike in the entire market. RSI 75.16 (overbought), above 50-DMA. Strong uptrend intact. No news catalyst provided, but this looks like a breakout on institutional buying or earnings surprise.

-

Affle India (₹1,642, +9.01%): digital marketing platform rallied sharply. Volume spike not quantified, but price action suggests a catalyst. Peer to MapMyIndia in the Software Products / IT Enabled Services space.

-

Vodafone Idea (₹12.19, +8.45%): the telecom stock that refuses to die. RSI 93.11 — severely overbought, strong uptrend, volume 3.61x average. This is speculative frenzy territory. Traders chasing momentum; investors should tread carefully at these RSI extremes.

-

KIMS Hospitals (₹777, +8.28%): healthcare provider surged on 5.51x volume, RSI 74.69 (overbought), above 50-DMA. Hospital chains are benefiting from capacity expansion post-pandemic and rising medical tourism.

-

Tata Consumer (₹1,271, +8.05%): already covered, but worth repeating — this is a defensive stock behaving like a mid-cap growth play. Volume 7.86x, fresh 52-week high.

-

HFCL (₹149.41, +5.85%): telecom infrastructure play. RSI 88.16 (overbought), strong uptrend, volume 1.45x. India’s 5G rollout and fiber network expansion underpin this move.

-

JBM Auto (₹684, +5.25%): auto components supplier rallied on 8.46x volume, RSI 69.64 (neutral but elevated), above 50-DMA. Possibly an EV contract win or Q4 beat.

-

Adani Green (₹1,391, +2.60%): renewable energy bellwether hit a 52-week high despite energy sector weakness (-1.84%). Flight to quality within clean energy.

The pain trades:

-

Urban Company (₹126.10, -9.72%): the on-demand services platform cratered on 3.72x volume, RSI 40.29. Q4 results (per headlines) showed widened losses. Growth-at-any-cost model under scrutiny.

-

ABB India (₹6,348, -9.48%): heavy electrical equipment giant plunged on 4.54x volume, RSI 27.67 (oversold), below 50-DMA. Q4 results disappointing, or margin pressure from input costs.

-

Kalyan Jewellers (₹385.90, -9.10%): strong downtrend, RSI 33.98, volume 5.15x. Titan (-6.85%, RSI 33.11, vol 4.28x) also bled. Jewellery retailers hit by gold price volatility and demand softness.

-

Blue Dart (₹5,268, -7.29%): logistics play in strong downtrend, RSI 39.4, volume 5.36x. Post-pandemic normalization hurting high-valuation logistics names.

-

Swiggy (₹263.95, -5.90%): food delivery platform fell on 2.62x volume, strong downtrend, RSI 36.27. Like Urban Company, growth-to-profitability transition scrutinized.

-

Siemens (₹3,589, -6.11%): fellow electrical equipment peer to ABB, also under pressure (strong uptrend but RSI 41.64, vol 1.7x). Sector-wide margin squeeze.

-

Escorts (₹2,969, -5.65%): tractor maker now oversold (RSI 26.3), strong downtrend, volume 2.52x. Rural demand concerns.

5. The Technical Picture

Oversold names (RSI < 30, potential mean-reversion candidates):

- SBI (₹974.90): RSI 21.86, below 50-DMA, volume 2.64x. Deeply oversold. If banking sentiment turns, this is the first bounce candidate.

- Canara Bank (₹130.14): RSI 19.77, below 50-DMA, volume 3.45x. Similar setup to SBI.

- Axis Bank (₹1,267.90): RSI 25.44, below 50-DMA, volume 1.05x. Contrarian play if private banks stabilize.

- Escorts (₹2,968.70): RSI 26.3, strong downtrend. Tractor demand bottom-fishing territory.

- ABB India (₹6,348): RSI 27.67, below 50-DMA. Value trap or earnings reset? Wait for price stability.

Overbought names (RSI > 70, caution zone):

- Vodafone Idea (₹12.19): RSI 93.11. This is parabolic. Avoid chasing.

- HFCL (₹149.41): RSI 88.16. Strong uptrend, but extended short-term.

- BSE (₹3,918.10): RSI 80.74. Exchange platform benefiting from derivatives boom (per headlines), but technically stretched.

- MCX (₹3,187): RSI 78.04, volume 2.26x. Similar story to BSE.

- Torrent Pharma (₹4,518): RSI 76.85, strong uptrend, volume 1.78x. Fresh 52w high, but RSI warns of near-term exhaustion.

Volume spikes (something’s happening):

- MapMyIndia: 15.01x volume — biggest spike in the market. Breakout confirmed.

- Niva Bupa (₹83.70, +2.96%): 14.92x volume, RSI 69.73. General insurance play — possibly stake sale or institutional buying.

- JBM Auto: 8.46x volume. Component play on fire.

- Tata Consumer: 7.86x volume. Defensive rotation with momentum.

- KIMS Hospitals: 5.51x volume. Healthcare sector strength.

No GOLDEN_CROSS or DEATH_CROSS signals explicitly flagged in today’s data.

6. AI Signals — BUY / HOLD / SELL

| Stock | Signal | Reason |

|---|---|---|

| MapMyIndia | BUY | Above 50-DMA, RSI 75 (overbought but trending), volume 15x avg — breakout confirmation |

| Tata Consumer | HOLD | Fresh 52w high, RSI 74, vol 7.86x — strong but extended, wait for pullback |

| KIMS Hospitals | BUY | Above 50-DMA, RSI 74.69, vol 5.51x — healthcare momentum intact |

| Adani Green | HOLD | 52w high but sector weak (-1.84%), no volume data — cautious optimism |

| JBM Auto | BUY | Above 50-DMA, RSI 69.64, vol 8.46x — component play on expansion |

| SBI | HOLD | RSI 21.86 (oversold), below 50-DMA, vol 2.64x — wait for trend reversal signal |

| Axis Bank | HOLD | RSI 25.44 (oversold), below 50-DMA — mean reversion play, but trend still down |

| Vodafone Idea | SELL | RSI 93.11 (extreme overbought), vol 3.61x — parabolic move unsustainable |

| ABB India | HOLD | RSI 27.67 (oversold), below 50-DMA, vol 4.54x — wait for earnings clarity |

| Escorts | HOLD | RSI 26.3 (oversold), strong downtrend — too early to catch the knife |

| Blue Dart | SELL | Strong downtrend, RSI 39.4, vol 5.36x — logistics sector under pressure |

| Swiggy | SELL | Strong downtrend, RSI 36.27, vol 2.62x — growth-to-profit transition rocky |

7. Tomorrow’s Setup — Global Cues & Calendar

Global tape is mixed but stable:

- US close: Dow -0.12%, S&P 500 +0.01%, Nasdaq -0.10%. Flat is the new up in volatile times.

- Asian close: Nikkei -0.47%, Hang Seng +0.05%, ASX -0.49%. No panic, but no euphoria either.

- GIFT Nifty: mirrors Monday’s close at 23,815.85 (-1.49%). Expect a flat to mildly negative open Tuesday.

- Currency: USD/INR at ₹95.30 (+1.11%). Weak rupee continues to weigh on importers, benefit exporters. Watch for RBI intervention signals.

- Crude oil: data not provided, but news references stable prices despite Middle East tensions. If Brent stays below $85, energy sector pressure may ease.

- Gold: data not provided, but typically rises during geopolitical stress — could support metal stocks if it rallies.

Key technical levels for Tuesday:

- Nifty 50: Support at 23,799 (Monday’s low), resistance at 23,997 (Monday’s high). Break below 23,750 opens 23,500. Break above 24,000 signals short-covering.

- Bank Nifty: Support at 54,360 (Monday’s low), resistance at 55,002. Needs to reclaim 55,000 to stabilize sentiment.

- India VIX at 18.55: still elevated. If it spikes above 20, expect more downside volatility.

What to watch Tuesday:

- FII flow data (if released).

- Any fresh Middle East developments overnight.

- Q4 earnings trickle: BSE reported Q4 profit jump +61% y-o-y (per headlines) — watch if derivatives momentum sustains.

- Rupee trajectory — sustained weakness past ₹95.50 could trigger risk-off selling in rate-sensitive sectors.

8. The Honest Take

For long-term investors: Monday was noise. If you own Sun Pharma, Tata Consumer, Adani Green, or quality pharma — congratulations, you just set fresh 52-week highs. If you own SBI or Axis Bank, you’re nursing paper cuts. The question is: do you believe India’s banking sector is structurally broken, or cyclically correcting? History says the latter. Oversold levels (RSI sub-25) on PSU banks have marked buying opportunities 7 out of 10 times over the past decade. But don’t catch falling knives — wait for price stabilization and trend reversal confirmation. Use the Raamdeo Agrawal framing from headlines: “India is the Ferrari among markets.” That’s not hype. It’s demographics + capex cycle + services exports. Volatility is the price you pay to ride the Ferrari. Buckle up.

For active traders: Monday was a stock-picker’s market. Broad indices down 1.5%, yet MapMyIndia +10%, Tata Consumer +8%, Vodafone Idea +8%. The divergence screams opportunity — but only if you have the tools to spot volume spikes and RSI extremes early. The oversold PSU banks (SBI, Canara) are on the radar for mean-reversion trades, but wait for at least one green candle above the 5-day EMA before entry. On the short side, anything overbought (RSI > 85) with weakening volume is a fade candidate — but Vodafone Idea’s 93 RSI might still squeeze higher before the crash. Risk management is everything when breadth is 1:3.3 against you.

“The stock market is filled with individuals who know the price of everything, but the value of nothing.” — Philip Fisher

Disclaimer: This blog is for informational and educational purposes only. It is not investment advice. All figures cited reflect publicly reported data for the trading session indicated. Markets are subject to risk; please consult a SEBI-registered advisor before acting on any view expressed here.