Unified Stocks — Friday, May 08, 2026

1. The Opening Scene

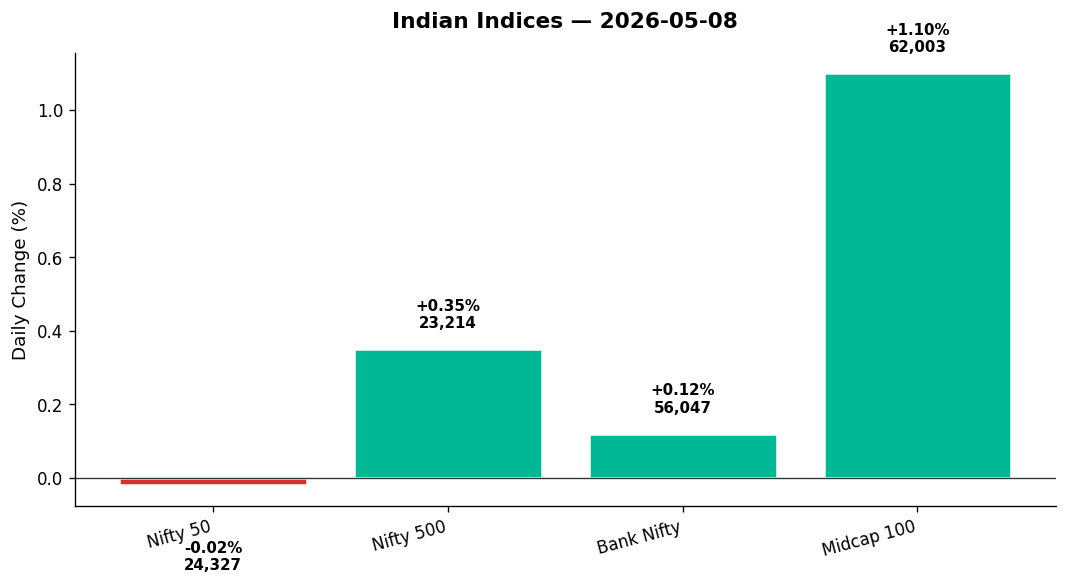

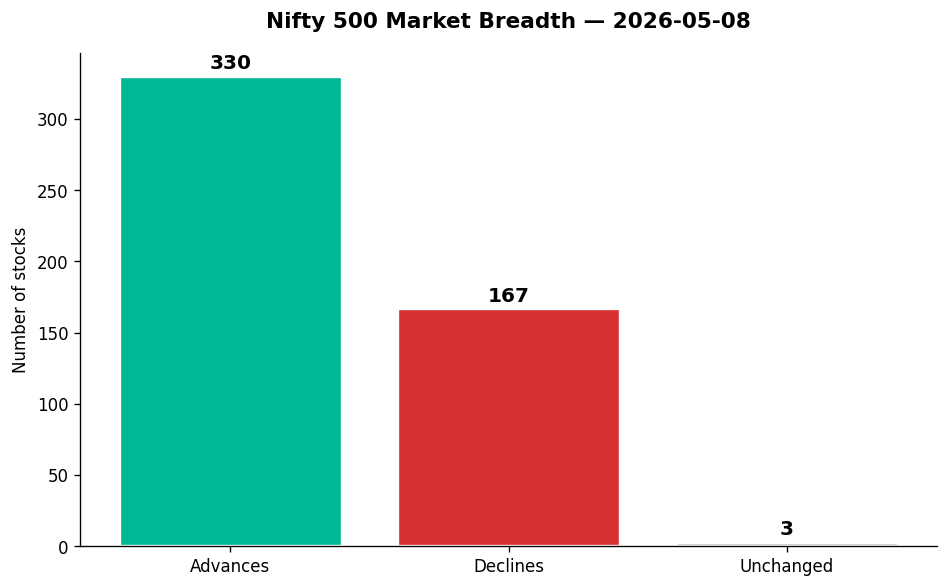

The bell rang on a Friday that seemed to spin on a pinhead. The Nifty 50 closed virtually flat — down 4.30 points, or 0.02%, at 24,326.65 — a day so indecisive that the index high and low stretched nearly 200 points apart before settling at the midpoint, exhausted. Yet beneath that shrug of the headline number, a different market was humming. The Nifty 500 rose 0.35%. The Midcap 100 jumped 1.10%. And most tellingly, 330 stocks advanced against just 167 declines — a 2-to-1 breadth ratio that screamed one thing: this was a stock-picker’s Friday, not a passive index-hugger’s paradise.

You could sense it in the volume. Craftsman Auto Components exploded 12.24% on 15x its usual volume, touching fresh 52-week highs. Godrej Industries — the diversified conglomerate, not the FMCG sibling — rocketed 20%, its biggest single-day gain in years. Meanwhile, IT bellwethers like Infosys and HCL Tech languished in oversold territory, hitting new lows, victims of a sector rotation that favoured old-economy manufacturing, autos, and defence over software and services. The VIX eased 0.34% to 16.62, suggesting calm on the surface. But the internals told a story of churn — money moving fast, pockets of euphoria bumping against zones of capitulation.

2. The Forces That Drove the Day

Crude’s Rally Splits the Tape

- Brent crude surged 1.10% to $102.38, WTI up 1.96% to $96.94. Energy stocks responded in kind: the Nifty Energy index rose 0.82%, but the directional impact was mixed. Upstream explorers and refiners felt the pinch on margins, while energy infra and power names rallied.

- USD/INR fell 0.99% to 94.24 — a stronger rupee easing import fears for oil-dependent sectors. Yet this tailwind didn’t prevent Oil & Gas (-0.10%) from slipping into the red.

Global Cues: Risk-Off in the West, Steady Signals from Asia

- US markets closed lower Thursday night: Dow -0.63%, S&P 500 -0.38%, Nasdaq -0.13%. FTSE 100 tumbled 1.55%. Yet Asian sentiment held firm, and GIFT Nifty signalled a modest positive open for Monday.

- Gold climbed 0.44% to $4,702.60, reflecting safe-haven appetite even as Indian equities ignored the script.

Bajaj Auto’s Record Profit Fuels Auto Euphoria

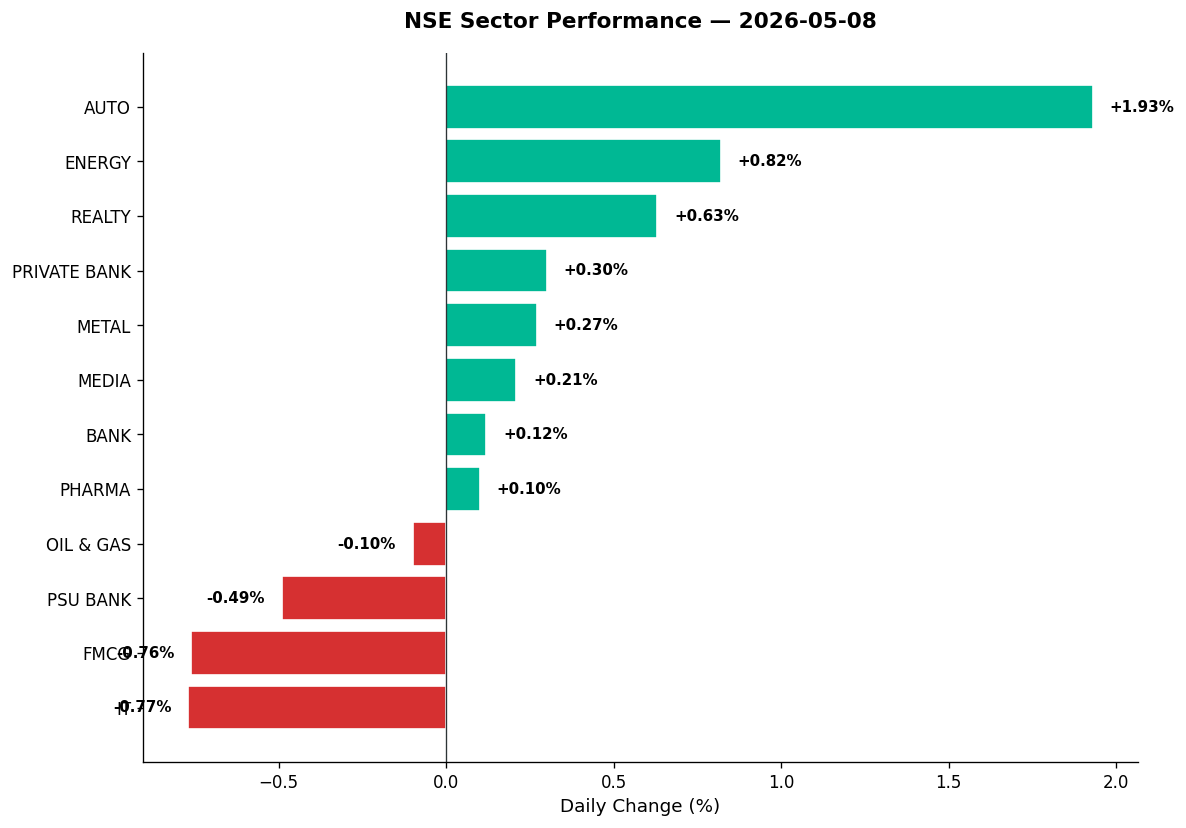

- Bajaj Auto posted its highest-ever quarterly net profit of ₹2,746 crore, driven by export strength and domestic volume surge. This headline rippled across the auto sector, lifting Nifty Auto +1.93% to 27,339.95 — the day’s best-performing major sector.

- Yet buried in the post-earnings commentary was a warning: executive director Rakesh Sharma flagged that more than a third of GST-related pricing gains had been eroded by inflationary pressures. The market chose to celebrate today, but the caution note lingers for Q2.

Breadth Strength = Midcap Muscle

- The 2:1 advance-to-decline ratio in the Nifty 500 reflected money rotating into midcaps, small-cap industrials, and thematic plays — Defence (+3.04%), Manufacturing (+0.85%), PSE (+0.45%).

- This wasn’t a Nifty 50 day. This was a day for the names you don’t see on CNBC tickers every hour.

3. A Walk Through the Sectors

Leaders: Auto Leads the Charge

- Auto (+1.93%): Bajaj Auto’s record profit set the tone. But the real fireworks came from auto ancillaries:

- Craftsman (+12.24%) hit a fresh 52-week high on 15x volume, RSI 62.78 — strong uptrend, not yet overbought.

- Endurance (+8.32%), Bharat Forge (+6.57% on 4.85x volume) — both riding the manufacturing and export momentum.

-

Even within the Nifty 50, sentiment was constructive. The sector’s strength came from depth, not just the headline names.

-

Energy (+0.82%): Crude’s rise lifted sentiment, though results were mixed. Upstream explorers faced margin pressure; power and energy infra names found support. The thematic Nifty Energy index echoed the sector’s 0.82% gain.

-

Realty (+0.63%): A modest bounce after recent volatility. Brigade tumbled 4.83% (RSI 72.85, overbought correction), but broader names in the space held steady. Momentum here is fragile — volume tells the tale.

Laggards: IT’s Painful Descent Continues

- IT (-0.77%): The sector that powered India’s equity bull market for two decades is now its weakest link.

- Infosys closed at ₹1,165.90, RSI 21.19 (oversold) — a strong downtrend with no technical reprieve in sight.

- HCL Tech hit a new 52-week low at ₹1,182.40 (-0.56%), closing with barely any bounce despite the support break.

- KPIT Tech (-3.29%) fell on 3.53x volume — a name often cited as a proxy for EV and auto software now caught in the broader tech selloff.

-

Tata Elxsi, Persistent Systems, TCS — all flat to negative. No rotation back into IT yet. The pain is real.

-

FMCG (-0.76%): Consumer staples struggled.

- Godrej Consumer Products (not to be confused with Godrej Industries) crashed 5.26% on 3.82x volume, entering a strong downtrend (RSI 45.39). Earnings disappointment or sector-wide demand concerns? The chart says: get out first, ask questions later.

-

Broader FMCG names like Britannia, Dabur, and Marico saw tepid action. Defensive sectors aren’t working in this rotation.

-

PSU Bank (-0.49%): A modest decline, but notable given Bank Nifty’s +0.12% gain. Private banks outperformed; PSU banks lagged. SBI, Bank of Baroda, and PNB all saw profit-taking after recent rallies.

Mixed Middle: Banks, Pharma, Metal, Media

-

Private Bank (+0.30%): HDFC Bank (-0.13%, RSI 48.49), ICICI Bank (-0.04%) — both treading water in strong downtrends, massive turnover but no conviction. Kotak Bank reportedly slid 4% in intraday action per news flow, though it doesn’t appear in the Nifty 500 top movers — a sign of isolated weakness.

-

Pharma (+0.10%): A tale of extremes.

- PPL Pharma surged 11.14% on 5.87x volume (RSI 71.72, overbought but justified by the breakout).

- Wockpharma fell 4.94% despite an RSI of 81.94 (overbought) — a classic case of profit-taking after a parabolic run.

-

Lupin, Aurobindo, Sun Pharma — all quiet. Pharma is stock-specific, not sector-wide momentum.

-

Metal (+0.27%): A flat sector with one critical outlier — Vedanta.

-

Media (+0.21%): Barely moved. Negligible volume, negligible conviction.

4. Beyond the Nifty 50 — Stories From the Broader Market

This is where Friday’s real story unfolded. The Nifty 50 was a sideshow; the midcaps, small-caps, and thematic plays stole the spotlight.

Godrej Industries (+20.00%): The Conglomerate Awakens

- ₹1,226.85, volume 6.67x average, RSI 73.95 — a blowout session. The diversified play — spanning chemicals, real estate, agri — saw something trigger institutional accumulation. News flow light, but the technicals scream: above 50-DMA, golden cross possible if momentum sustains.

Defence Stocks: The 3.04% Sector Surge

- Nifty India Defence +3.04% — another day, another rally in HAL, BEL, Mazagon Dock, Bharat Electronics.

- BHEL (+5.32%) hit a fresh 52-week high at ₹406.50, RSI 86.71 (overbought), 1.38x volume. Strong uptrend, but nearing exhaustion levels.

- GVT&D (+5.02%), a heavy electrical equipment play, also spiked (RSI 78.47, overbought). The defence-infra-manufacturing complex remains the market’s favourite narrative. Until it isn’t.

Telecom & Semis: Breakouts in Pockets

- Tejas Networks (+14.90%) exploded on ₹48.43 crore turnover — a telecom equipment play riding 5G and optical fibre rollout themes. No RSI data, but the price action speaks.

- HFCL (+3.92%) hit a fresh 52-week high at ₹147, RSI 91.14 — the most overbought stock in the dataset. Strong uptrend, 1.73x volume. Telecom infra, defence electronics, optical fibre. It’s all working. But RSI >90 is a flashing yellow light: take profits or watch tight stops.

Vedanta (-3.41%): The Oversold Outcry

- ₹305.60, RSI 14.97 (deeply oversold), 1.94x volume, below 50-DMA — this is a stock in distress. The demerger news (four entities to be carved out) has created uncertainty. Some see value; the market sees risk. Until the demerger listings clarify, Vedanta remains a knife traders are trying to catch.

Paytm (+7.73%): The Fintech Bounce

- ₹1,196.40, 4.11x volume, RSI 32.65 (neutral but recovering from oversold) — Paytm’s revenue growth guidance for FY27 (per news flow: “faster growth than FY26”) sparked a relief rally. Above 50-DMA, but still in a long-term downtrend. A trade, not an investment — yet.

BSE & MCX: The Exchange Duo Hits New Highs

- BSE (+3.35%) at ₹3,981, fresh 52-week high. MCX (+2.75%) at ₹3,055, also a new high. Both exchanges benefiting from retail trading boom, F&O volumes, and institutional confidence. Clean technicals, rising volume, no overheated RSIs. These are rare pockets of quality momentum.

Polycab (+7.30%): The Cable King’s March

- ₹9,030, fresh 52-week high, RSI 59.96 (neutral), 3.53x volume — strong uptrend. Manufacturing, electrification, infra spend. All tailwinds. This is what “buy the dips” looks like when it works.

Meesho (+0.98%): The E-commerce Dark Horse

- ₹198.20, RSI 67.44, 3.06x volume — the e-commerce play quietly climbing. Not Nykaa volatility, not Zomato drama. Just steady accumulation. Most active by value today, yet few headlines. That’s often when the smart money moves.

5. The Technical Picture

Oversold Zone: Opportunity or Trap?

- Vedanta (RSI 14.97), Infosys (RSI 21.19) — both below 30, both in confirmed downtrends. Oversold doesn’t mean buy; it means: “watch for stabilisation first, then act.”

Overbought Zone: Profit-Taking Alerts

- HFCL (RSI 91.14) — the highest in the dataset. Parabolic. Be cautious.

- Jain Rec (RSI 83.03), Wockpharma (RSI 81.94), Godrej Industries (RSI 73.95), PPL Pharma (RSI 71.72), Brigade (RSI 72.85) — all above 70. Some justified (breakouts), some not (reversals incoming).

Volume Spikes: Where the Action Is

- Craftsman (14.99x), ABLBL (11.79x), CarTrade (7.62x), Godrej Industries (6.67x), Aegis Vopak (6.52x), PPL Pharma (5.87x), Nuvoco (5.60x), Bharat Forge (4.85x) — these aren’t noise. These are institutional moves, breakout confirmations, or capitulation sells. Each warrants a deep dive.

Golden Cross Watch

- No explicit golden crosses (50-DMA crossing above 200-DMA) flagged today, but several names (Craftsman, Bharat Forge, Polycab) are in strong uptrends with momentum intact. Watch next week.

Death Cross Reality

- Infosys, HCL Tech, HDFC Bank — all in strong downtrends, 50-DMA well below 200-DMA. These are confirmed long-term underperformers. Wait for trend reversal signals (RSI divergence, volume capitulation) before re-entry.

6. AI Signals — BUY / HOLD / SELL

| Stock | Signal | Reason |

|---|---|---|

| Craftsman Auto | BUY | Strong Uptrend, above 50-DMA, RSI 62.78 (neutral), vol 14.99x avg, fresh 52w high |

| Bharat Forge | BUY | Strong Uptrend, RSI 52.72 (neutral), vol 4.85x avg, above key DMAs |

| Polycab | BUY | Strong Uptrend, fresh 52w high, RSI 59.96 (neutral), vol 3.53x avg |

| BSE | BUY | Fresh 52w high, strong volume, RSI not overbought, clean uptrend |

| Paytm | HOLD | Above 50-DMA, recovering from oversold (RSI 32.65), vol 4.11x — wait for RSI >40 to confirm |

| Godrej Industries | HOLD | Massive breakout (+20%), but RSI 73.95 overbought, vol 6.67x — profit-taking likely near-term |

| HFCL | SELL | RSI 91.14 (extreme overbought), parabolic move unsustainable despite strong uptrend |

| Vedanta | SELL | RSI 14.97 (oversold), below 50-DMA, strong downtrend, demerger uncertainty — avoid until clarity |

| Infosys | SELL | RSI 21.19 (oversold), strong downtrend, death cross confirmed, no reversal signals yet |

| HCL Tech | SELL | Fresh 52w low, strong downtrend, RSI not provided but price action confirms weakness |

| Wockpharma | SELL | Down 4.94% despite RSI 81.94 overbought — profit-taking after parabolic run, avoid |

| Godrej Consumer | SELL | Down 5.26%, strong downtrend (RSI 45.39), vol 3.82x — distribution phase, exit |

7. Tomorrow’s Setup — Global Cues & Calendar

Global Tape: Risk-Off Overnight, But Asia Holds

- US equities closed lower Thursday: Dow -0.63%, S&P 500 -0.38%, Nasdaq -0.13%. Tech weakness persists. FTSE 100 -1.55% adds to the cautious tone.

- GIFT Nifty signals modest positive open Monday — the weekend gap will depend on headlines, but the setup is neutral-to-mildly-bullish.

Commodities: Crude’s Rally, Gold’s Creep

- Brent crude at $102.38 (+1.10%), WTI at $96.94 (+1.96%) — energy complex on edge. Watch for OPEC+ commentary over the weekend. A break above $105 Brent will pressure import-heavy sectors.

- Gold at $4,702.60 (+0.44%) — creeping higher. Safe-haven flows suggest macro unease despite equity resilience.

Currency: Rupee Strength a Short-Term Relief

- USD/INR at 94.24 (-0.99%) — a stronger rupee eases FII concerns and import costs, but sustainability depends on Fed policy signals and domestic data flow next week.

Key Technical Levels for Monday

- Nifty 50: Support at 24,284 (today’s low), resistance at 24,482 (today’s high). A break above 24,500 opens 24,650; below 24,250 invites 24,000 retest.

- Bank Nifty: Support at 55,783, resistance at 56,334. Range-bound; watch for breakout above 56,500 or breakdown below 55,500.

- Nifty 500: Strong close at 23,214 (+0.35%). Midcap momentum intact; watch for follow-through above 23,300.

8. The Honest Take

For long-term investors: This market is rewarding selectivity and punishing complacency. The Nifty 50’s flatness masks a violent rotation beneath the surface — away from IT and large-cap defensives, toward manufacturing, autos, defence, and energy infrastructure. If your portfolio is overweight TCS, Infosys, and HDFC Bank, you’re feeling pain. If you own Craftsman, Bharat Forge, BSE, and Polycab, you’re smiling. The message: diversify beyond the usual suspects. The India growth story is broadening, not narrowing. But breadth-driven rallies are fragile — they work until they don’t. Stay disciplined. Rebalance winners. Don’t chase RSI >80 names.

For active traders: Friday was a gift — 2:1 breadth, volume spikes, breakouts on confirmation. But it was also a minefield. Oversold names like Vedanta and Infosys look tempting, but downtrends don’t reverse on hope. Wait for RSI divergence, volume capitulation, or 50-DMA reclaims. Overbought names like HFCL (RSI 91!) are screaming “take profits.” The sweet spot today was names like Craftsman, Bharat Forge, and BSE — strong uptrends, neutral RSIs, volume confirmation. That’s the template: buy momentum with room to run, not parabolas begging for gravity. Next week, watch crude, watch global sentiment, and watch the midcap 100. If it stays above 62,000, the broadening rally continues. If it cracks, rotate to cash and quality large-caps.

“The stock market is filled with individuals who know the price of everything, but the value of nothing.” — Philip Fisher

Disclaimer: This blog is for informational and educational purposes only. It is not investment advice. All figures cited reflect publicly reported data for the trading session indicated. Markets are subject to risk; please consult a SEBI-registered advisor before acting on any view expressed here.