Unified Stocks — Tuesday, May 12, 2026

1. The Opening Scene

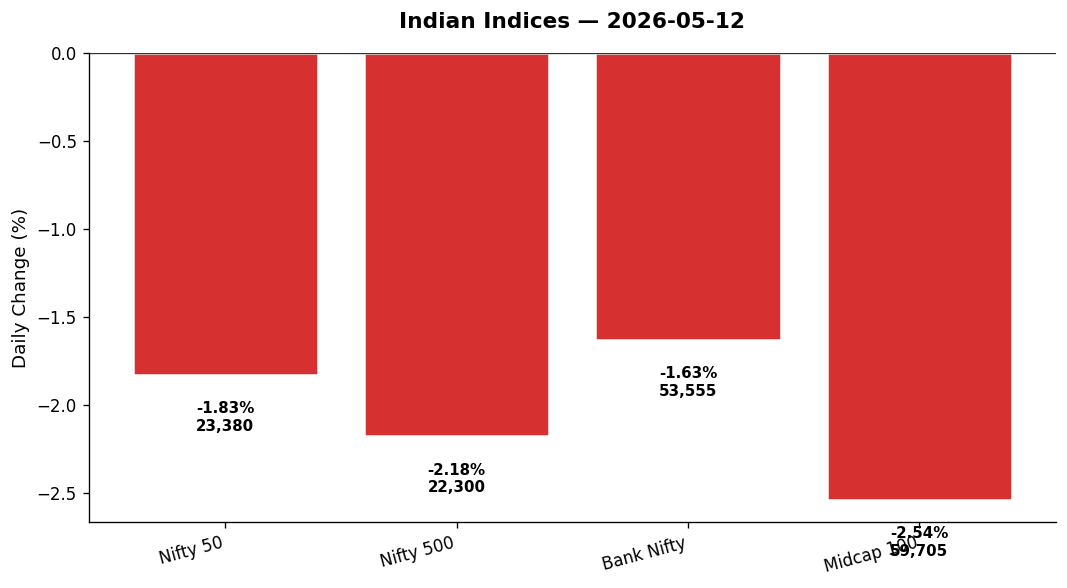

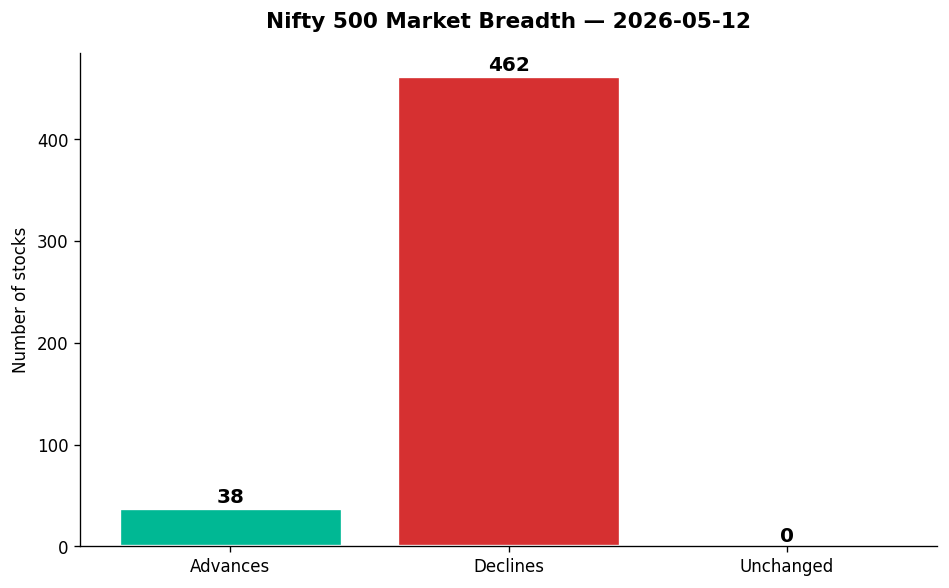

Some days, the market doesn’t just decline — it capitulates. Tuesday felt less like a trading session and more like a scene from a disaster film: panic selling in the opening hour, buyers vanishing by lunchtime, and by the closing bell, 462 stocks on the Nifty 500 had retreated while only 38 stood their ground. The Nifty 50 shed 436 points (-1.83%) to close at 23,379.55, while the broader Nifty 500 bled 2.18%. The Midcap 100 took it worse, down 2.54%, and the India VIX — that barometer of fear — spiked 3.92% to 19.28, its highest close in three weeks.

What drove this rout? A toxic cocktail: Brent crude surged 2.88% to $107.21, the rupee hit a record low at ₹95.62 per dollar, and Prime Minister Modi’s Sunday appeal for Indians to conserve fuel, resume work-from-home, and cut cooking oil consumption finally sank in. The Strait of Hormuz remains a chokepoint; US-Iran tensions are rising, not easing. Global markets gave us no cushion — the DAX fell 0.89%, and GIFT Nifty signalled a flat-to-negative Wednesday open. By day’s end, only the oil and gas explorers stood tall. Everything else? Buried under a landslide of red.

2. The Forces That Drove the Day

Four macro forces turned Tuesday into a bloodbath:

-

Crude oil’s relentless climb: Brent above $107 is a direct tax on India’s import bill. WTI crossed $100.75 (+2.73%). For every $10 rise, India’s CAD widens by ~0.4% of GDP. Defence Minister Rajnath Singh assured the nation of “adequate fuel stocks” — but the market heard “we’re burning forex reserves.”

-

Rupee collapse: At ₹95.62/USD (+1.26%), the rupee hit an all-time low. This hammers IT exporters (receivables lose value) and importers alike. HDFC Bank and ICICI Bank, both down and oversold (RSI 30.1 and 18.44 respectively), reflect FII liquidation and balance sheet stress.

-

PM Modi’s conservation plea: His Sunday call to skip gold purchases for a year, trim cooking oil, and resume WFH isn’t just policy — it’s a distress signal. Markets read between the lines: forex reserves are under strain, and consumption must be curbed. FMCG stocks bled 1.47%, led by Britannia hitting a fresh 52-week low at ₹5,333.

-

Vanishing breadth: Just 38 advances vs 462 declines across the Nifty 500. This isn’t sector rotation — this is capitulation. Even defensive pharma fell 1.36%, and IT collapsed 3.73%. Only the oil explorers dared to rally.

3. A Walk Through the Sectors

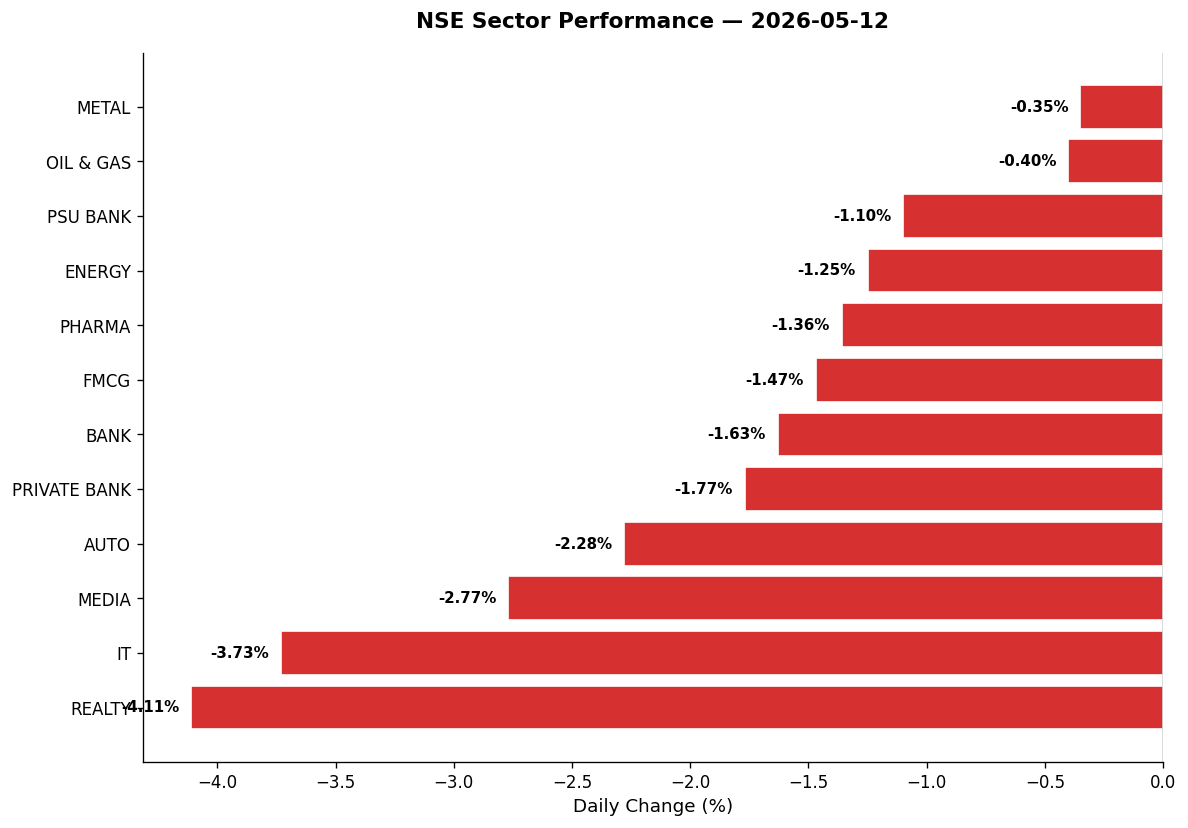

The sectoral damage was broad, brutal, and unapologetic. Let’s walk the wreckage:

Winners (or least damaged):

-

Metal (-0.35%): Held up best. Vedanta (+2.53%) bucked the trend despite being oversold (RSI 16.3), volume spiked 1.3x. Hindalco’s Zinc arm (+2.26%) added ₹13, RSI at a healthy 62.5. Metals found support from crude-driven inflation expectations — higher input costs, but also pricing power.

-

Oil & Gas (-0.40%): The sector’s lone bright spot. Oil India (+7.46%) exploded on 5.11x volume, RSI 58.96, riding crude’s surge. ONGC (+4.70%) followed with 3.05x volume. When crude hits $107, upstream explorers print money. IOC and BPCL (refiners) lagged — data not available, but refining margins compress when crude moves this fast.

The Middle (steady losers):

-

PSU Bank (-1.10%): SBI (+0.26%) eked out a tiny gain but remained deeply oversold (RSI 22.97). After losing $11 billion in market cap over two sessions (per news), the stock’s clinging to ₹976. Canara and BoB in focus post-earnings, but sentiment is fragile.

-

Energy (-1.25%): Defensive utilities held better than growth stocks. JSW Energy (-6.51%) was the exception — despite a 38% YoY profit jump in Q4, it bled ₹36 as investors feared margin pressure from rising coal costs.

-

Pharma (-1.36%): Defensive, but not immune. Biocon (+3.41%) rallied on volume, but the sector leader Sun Pharma (data unavailable) likely dragged the index.

-

FMCG (-1.47%): Modi’s plea to cut cooking oil hit hard. Britannia (-1.43%) touched a 52-week low. Patanjali Edible Oil (-2.59%) fell to ₹442.35 on volume. The PM’s message: belt-tightening begins with breakfast.

Laggards (the carnage):

-

Bank (-1.63%): ICICI Bank (-1.73%) is oversold (RSI 18.44), HDFC Bank (-1.13%) just above oversold (RSI 30.1). Both are in strong downtrends, reflecting FII exodus and NIM compression fears. Bank Nifty shed 884 points to close at 53,555.

-

Private Bank (-1.77%): Amplified the pain. With PSU banks holding steadier, the private sector bore the brunt of foreign selling.

-

Auto (-2.28%): Discretionary spending under threat. Olectra (EVs) (-6.72%) fell despite being above its 50-DMA, RSI 56. Volume spiked 1.3x — someone’s dumping. The PM’s WFH push is bearish for passenger vehicles.

-

Media (-2.77%): Small-cap pain. Ad spends contract when oil eats household budgets.

-

IT (-3.73%): The session’s worst performer. TCS (-3.74%) hit a fresh 52-week low at ₹2,303.50, oversold (RSI 21.36), volume 1.71x. HCL Tech (-4.01%) joined it at a new low. Infosys (-3.17%) bled on 16.8m shares. Sonata Software (-8.68%) crashed on 2.7m volume. The rupee’s collapse means lower dollar realisations, and clients are pausing spending amid global uncertainty.

-

Realty (-4.11%): Worst of all. Anant Raj (-6.25%) fell to ₹504.90 on 4.8m shares. Higher interest rates (bond yields spiked per news) and a slowing economy are death for real estate.

Thematic bloodbaths:

-

Defence (-4.03%): HAL, BEL, Mazagon Dock (data not available for specifics) all sank. Kaynes Tech (-6.79%) fell to ₹4,068 on 1.6x volume, still above its 50-DMA but momentum broken. Defence spending fears as the government prioritises oil security over capex.

-

Manufacturing (-1.84%): Modi’s call to “reduce fertiliser use” and conserve resources is bearish for industrials.

4. Beyond the Nifty 50 — Stories From the Broader Market

The real drama unfolded outside the index heavyweights. Here’s where Tuesday’s narrative turned personal:

-

Groww (-4.98%): The fintech unicorn crashed on 542 million shares — 6.29x its average volume. RSI plunged to 21.88 (oversold). Price: ₹183.89. This is panic liquidation, likely stop-loss triggers cascading. Groww’s debut cohort is underwater.

-

Oil India (+7.46%): The day’s hero. At ₹490, volume hit 31.7 million (5.11x avg). RSI at 58.96 signals room to run. Strong uptrend intact. When crude’s at $107, upstream is king.

-

ONGC (+4.70%): Another oil play. At ₹294.20 on 52 million shares (3.05x), RSI 58.43. If Hormuz stays shut, ONGC’s FY27 EBITDA could jump 15–20%.

-

Vedanta (+2.53%): The diversified metals giant clawed back to ₹305.95 despite being oversold (RSI 16.3) and below its 50-DMA. Volume: 47.6m (1.3x). Vedanta’s a coiled spring — oversold + commodity tailwinds = contrarian buy setup.

-

FirstCry (+2.39%): The baby products e-tailer rallied to ₹235 on 3.53x volume. RSI 34.28, above its 50-DMA. Defensive play — parents don’t cut baby spend even in downturns.

-

Paradeep Phosphates (+4.01%): Fertiliser stocks rallied despite Modi’s “reduce fertiliser use” plea. At ₹127.50 on 5.47x volume, RSI 36.94. Counter-intuitive, but subsidies remain intact, and crude’s rise lifts all input costs — pricing power.

-

Birlasoft (-6.72%): IT mid-cap mauled. At ₹332, volume 2.79x, RSI 12.77 (deeply oversold), in a strong downtrend. This is near-death territory. Either a bounce or ₹300 next.

-

Dixon Technologies (-6.05%): The consumer electronics champ fell to ₹10,120 on 1.31x volume. RSI 29.93 (oversold), in a downtrend. Post-lockdown winners are reversing as consumption slows.

-

Swiggy (-2.62%): Hit a fresh 52-week low at ₹256.80 on 8.3m shares. Q4 loss of ₹800 crore (per news) spooked investors. Nomura and Citi remain divided — growth vs profitability debate rages.

-

Naukri (-2.99%): Another 52-week low at ₹932.50. White-collar hiring freezes as oil shock hits corporate budgets.

-

RKFORGE (-5.44%): Auto component maker hit a GOLDEN_CROSS today (50-DMA crossed above 200-DMA). Yet it fell to ₹588. RSI 57.88, volume 0.69x. Classic “sell the signal” action — bullish long-term, but near-term overbought.

5. The Technical Picture

Tuesday’s technicals scream one word: oversold.

Deeply oversold names (RSI < 25):

- Groww (21.88): Panic selling, volume 6.29x — watch for a dead-cat bounce.

- TCS (21.36): New 52w low, oversold + downtrend = avoid until RSI crosses 30.

- SBI (22.97): Below 50-DMA, but at ₹976, risk/reward tilts bullish for long-term buyers.

- ICICI Bank (18.44): Most oversold of the private banks. Strong downtrend, but single-digit RSI rarely lasts.

- Vedanta (16.3): Oversold + commodity tailwinds = high-conviction contrarian play.

- Birlasoft (12.77): Avoid — strong downtrend, no reversal signals yet.

Overbought extremes (RSI > 80):

- HFCL (86.77): Telecom infra stock at ₹149, volume 1.25x. Parabolic move — take profits.

- Idea (85.29): At ₹11.99, volume 1.9x. Vodafone stake transfer rumours (per news) drove the spike. Overbought + strong uptrend = hold but don’t chase.

- MCX (79.44): Exchange platform at ₹3,175. Overbought but strong trend. Volatility = higher trading volumes = bullish for MCX.

- BSE (75.06): At ₹3,855, RSI overbought but trend intact. Q4 profit jumped 61% YoY to ₹797 crore (per news). Don’t fade the momentum.

Volume spikes (>2x) — “something’s happening”:

- Groww (6.29x): Covered above — capitulation.

- Syrma SGS (5.5x): Industrial tech at ₹1,079, RSI 64.98, strong uptrend. Volume spike on a -3% day = distribution or stop-hunt?

- Paradeep (5.47x), Oil India (5.11x), FirstCry (3.53x): All covered — each tells a story of sector-specific action.

Golden Cross today:

- RKFORGE: 50-DMA crossed above 200-DMA — a classic long-term buy signal. Yet it fell 5.44% today. Why? Overbought short-term (RSI 57.88), and auto stocks are under pressure. File this under “buy the dip in 2–4 weeks.”

6. AI Signals — BUY / HOLD / SELL

Based on today’s technical + price action data:

| Stock | Signal | Reason |

|---|---|---|

| OIL INDIA | BUY | Strong uptrend, RSI 58.96 neutral, volume 5.11x avg — crude tailwind intact |

| ONGC | BUY | Strong uptrend, RSI 58.43, volume 3.05x — upstream play on $107 Brent |

| VEDANTA | BUY | Oversold (RSI 16.3), volume 1.3x, metals + oil inflation = contrarian value |

| PARADEEP PHOSPHATES | BUY | Above 50-DMA, RSI 36.94, volume 5.47x — fertiliser subsidies intact |

| FIRSTCRY | BUY | Above 50-DMA, RSI 34.28, volume 3.53x — defensive consumer play |

| SBI | HOLD | Oversold (RSI 22.97), below 50-DMA, volume 1.42x — wait for RSI >30 |

| ICICI BANK | HOLD | Oversold (RSI 18.44), strong downtrend — too early, needs stabilisation |

| TCS | HOLD | Oversold (RSI 21.36), 52w low, downtrend — avoid until trend reverses |

| HFCL | HOLD | Overbought (RSI 86.77), strong uptrend — take partial profits, don’t add |

| IDEA | HOLD | Overbought (RSI 85.29), stake transfer rumour — wait for pullback |

| BIRLASOFT | SELL | Strong downtrend, RSI 12.77 oversold, volume 2.79x — no reversal yet |

| GROWW | SELL | Oversold (RSI 21.88), volume 6.29x panic — wait for bottom confirmation |

| JSW ENERGY | SELL | -6.51% despite Q4 beat, no technical support — avoid until ₹500 holds |

| DIXON TECH | SELL | Strong downtrend, RSI 29.93 oversold, volume 1.31x — consumption slowdown |

7. Tomorrow’s Setup — Global Cues & Calendar

Wednesday’s open depends on three things:

Global tape (mildly positive, but fragile):

- US equities: Dow +0.19%, S&P 500 +0.19%, Nasdaq +0.10%. Barely green — no conviction.

- Asian futures: Nikkei +0.52%, but Hang Seng -0.22%, ASX -0.36%. China’s weak, Japan’s resilient.

- GIFT Nifty: Signals a flat open at 23,379 (same as Tuesday’s close). No gap up, no gap down — all eyes on domestic action.

Commodity storm:

- Crude: Brent at $107.21 (+2.88%), WTI at $100.75. If Hormuz tensions persist, ₹110 Brent is next. Bearish for India (importers bleed), bullish for OIL/ONGC.

- Gold: Flat at $4,717.80 (-0.02%). PM Modi asked Indians to skip gold for a year — but ₹95.62/USD makes gold imports cheaper. Expect jewellery stocks (Titan, Kalyan) to remain under pressure.

- Rupee: At ₹95.62, the RBI’s defending ₹96. If it breaks, FII panic accelerates.

Key technical levels for Wednesday:

- Nifty 50: Support at 23,348 (today’s low). Resistance at 23,757 (today’s high). Below 23,300 = 23,000 next. Above 23,600 = short covering to 23,800.

- Bank Nifty: Support at 53,457 (today’s low). Resistance at 54,000. Oversold banks (ICICI, SBI) need to stabilise here or 52,000 comes fast.

- Nifty 500: Support at 22,270. Below = pain for mid/small caps. Breadth needs to flip — today’s 38:462 ratio can’t repeat.

Watch for: Any news on Hormuz (US-Iran talks), RBI dollar selling, or government stimulus. Without a catalyst, Wednesday could be range-bound — a pause after the plunge.

8. The Honest Take

For long-term investors:

Tuesday was a gift wrapped in fear. TCS at a 52-week low, SBI oversold, ICICI Bank at RSI 18 — these are generational names trading at panic prices. Yes, crude at $107 is a headwind, and yes, the rupee’s collapse hurts short-term sentiment. But zoom out: India’s domestic consumption story hasn’t changed, and FY27 earnings (ex-IT) will reflect pricing power, not just volume growth. If you have cash, deploy 25% today into oversold defensives (SBI, Vedanta, Paradeep). Save the rest for 23,000 on Nifty — if we get there, it’s a buying opportunity disguised as Armageddon.

For active traders:

Avoid heroics. 462 declines vs 38 advances isn’t a market — it’s a landslide. Wait for breadth to flip (at least 150+ advances) before adding longs. Oil/ONGC longs are crowded now; book half if you’re up. Groww’s 6.29x volume signals capitulation, but don’t catch it yet — RSI 21 can go to 15. Watch Bank Nifty at 53,457 support; a bounce from there could spark a 1–2% relief rally. Otherwise, sit on hands. The VIX at 19.28 means premiums are expensive — option sellers, take note.

— Unified Stocks

“The stock market is a device for transferring money from the impatient to the patient.” — Warren Buffett