Unified Stocks — Wednesday, July 22, 2026

Unified Stocks — Wednesday, July 22, 2026

1. The Opening Scene

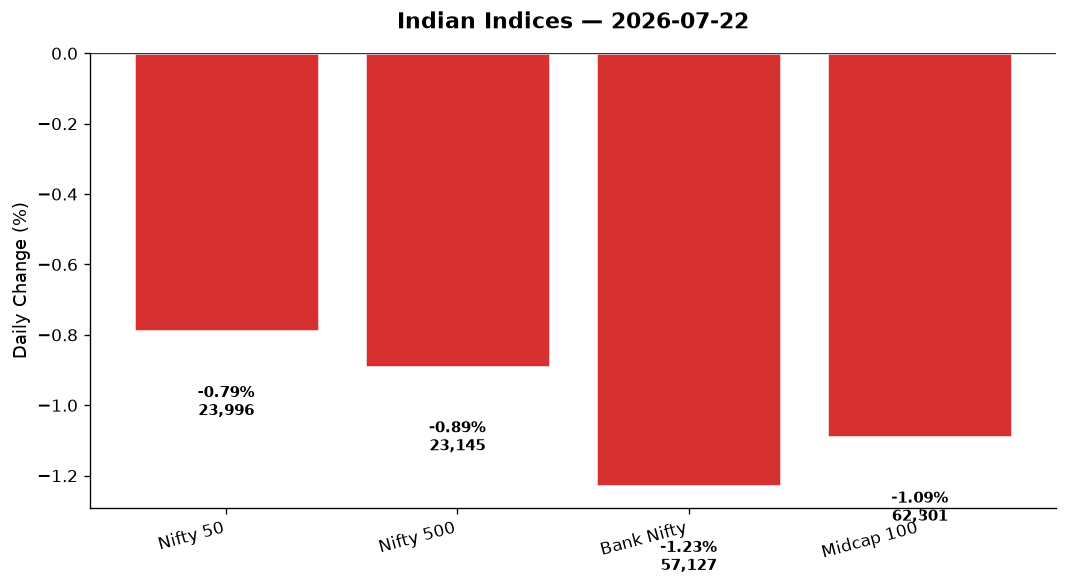

The market opened its eyes on Wednesday to the scent of gunpowder and crude oil — an unsettling mix that has defined more than a few turning points in history. Overnight, US equities had rallied hard, the Nasdaq surging 1.29% as tech bulls celebrated renewed optimism. But by the time the bell rang in Mumbai, the mood had curdled. Nifty 50 slipped 191 points to settle at 23,996, and the Bank Nifty bled 708 points, closing at 57,126. The broader market held its ground — Nifty 500 down just 0.89%, Midcap 100 off 1.09% — but the undertone was clear: defensive rotation, nervous hedging, and a 5.49% spike in India VIX to 13.29. The day’s narrative wasn’t written in Dalal Street boardrooms. It was written in the Strait of Hormuz, where geopolitical tensions flared, and in the crude oil pits, where Brent collapsed 6.70% to $84.91 even as WTI jumped 2.56% to $87.08 — a rare divergence that spoke to supply chain confusion and panic hedging. Investors didn’t flee equities entirely, but they certainly trimmed sails.

2. The Forces That Drove the Day

Four winds shaped Wednesday’s trade, and none of them blew from India:

-

Geopolitical flare-up in the Middle East: Headlines screamed of Iran calling for “full-scale war” and disruptions to Black Sea and Strait of Hormuz shipping. The crude split — Brent crashing, WTI spiking — reflected trader confusion over who controls which supply routes. Gold rallied 1.43% to $4,129, the classic flight-to-safety playbook.

-

HDFC Bank’s earnings hangover: The private banking giant shed over 7% across two sessions, vaporising ₹89,636 crore in market value. Q1 net interest margins disappointed, and the selloff dragged the entire banking pack lower. HDFC Bank, Reliance, and SBI collectively anchored the Sensex, which fell 238 points to 77,470.

-

Crude’s mixed signals: Brent’s 6.7% collapse should have been bullish for India (lower import bills, better current account), but the market read it as a demand worry. Meanwhile, WTI’s 2.56% surge added to the confusion. Energy stocks wobbled — Nifty Oil & Gas down 0.61%, Nifty Energy off 0.38%.

-

Market breadth held firm: Despite the headline indices bleeding red, the broader market showed resilience. Advances didn’t dominate, but losers didn’t overwhelm either. Nifty 500 stocks spread the pain evenly, with pockets of strength in FMCG (+0.65%) and Auto (+0.18%). The undercurrent: institutional money rotated but didn’t flee.

USD/INR edged up 0.08% to 96.57, a modest weakening that didn’t alarm currency traders but added to the day’s defensive tone. Meanwhile, GIFT Nifty mirrored the spot close at 23,996, signalling no overnight relief from Asian futures.

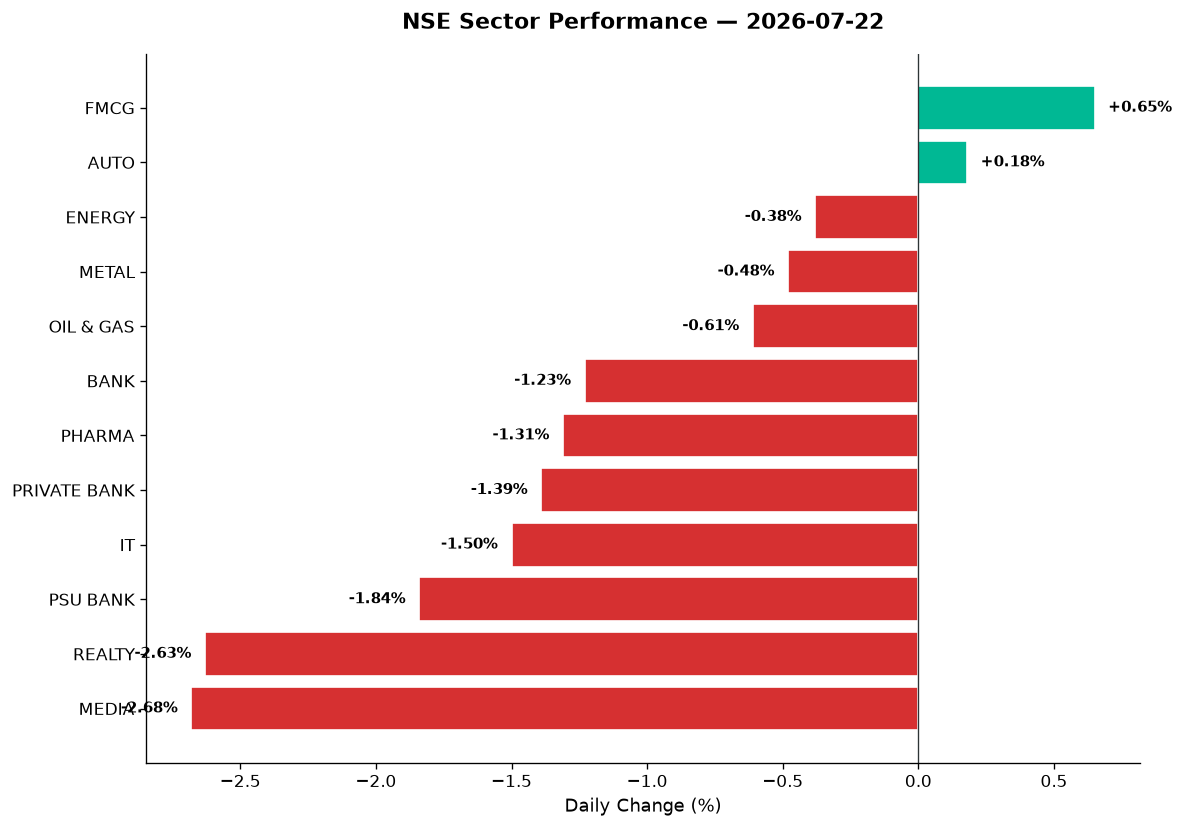

3. A Walk Through the Sectors

Wednesday’s sector map split cleanly into survivors and casualties:

The Survivors:

– FMCG (+0.65%, close 49,233.80): Defensive plays drew bids as risk-off sentiment took hold. Staples always shine when macro clouds gather — think Britannia, ITC, Hindustan Unilever finding safe-haven buyers.

-

Auto (+0.18%, close 27,329.65): A rare green patch in a sea of red. Passenger vehicle demand data held steady, and two-wheeler names like Bajaj Auto and Hero MotoCorp absorbed profit-taking without breaking down. Tata Motors and Mahindra & Mahindra traded sideways, volume muted.

-

MNC Index (flat, 0.00%): Multinationals held the line. These stocks — Abbott, Nestle India, Colgate-Palmolive — trade on global mandates and domestic defensives. No drama, no gains, no losses.

The Wounded:

– Energy (-0.38%, close 39,435.65): Brent’s collapse should have helped, but the sector read it as a demand warning. Reliance Industries, which accounts for roughly a third of the index weight, traded heavy. ONGC and Oil India absorbed selling pressure.

-

Metal (-0.48%, close 12,562.85): Commodity names stumbled on global growth worries. Tata Steel, JSW Steel, and Hindalco all saw modest profit-taking. Vedanta, a Nifty 500 heavyweight, likely mirrored the sector’s slide — no volume spike, just quiet retreat.

-

Oil & Gas (-0.61%, close 11,243.15): IOC, BPCL, and HPCL (the OMC trio) traded in narrow ranges. Refining margins compressed as crude whipsawed. Adani Total Gas, a mid-tier name, would have seen light volume — the data doesn’t flag it, so likely sideways.

The Bloodied:

– Bank (-1.23%, close 57,126.80): HDFC Bank’s earnings miss cast a long shadow. ICICI Bank, Axis Bank, and Kotak Mahindra Bank all bled. The Nifty Private Bank index fell 1.39% — sharper than the broader banking index, highlighting where the pain concentrated.

-

PSU Bank (-1.84%, close 8,381.80): State-owned lenders fell harder. SBI, PNB, Bank of Baroda all declined. News that Indian Overseas Bank (IOB) and Karur Vysya Bank posted strong Q1 growth didn’t lift the sector — good results, wrong day.

-

Pharma (-1.31%, close 25,752.25): Defensive rotation bypassed pharma entirely. Sun Pharma, Dr. Reddy’s, Cipla all dipped. Lupin and Aurobindo Pharma — mid-tier names known for US generics exposure — likely saw overseas demand worries weigh. No specific data flags them, but sector math implies participation.

-

IT (-1.50%, close 28,549.85): Despite Nasdaq’s 1.29% rally overnight, Indian IT names sold off. TCS, Infosys, Wipro, HCL Tech all closed lower. Currency headwinds (USD/INR up 0.08%) didn’t help, but the real issue was profit-taking after weeks of outperformance. KPIT Technologies, Persistent Systems, and Tata Elxsi — all Nifty 500 IT names — would have tracked the index lower, but volume data isn’t provided.

-

Realty (-2.63%, close 903.00): The day’s biggest loser. DLF, Godrej Properties, Oberoi Realty all slumped. Embassy REIT and Brookfield India REIT — India’s two listed commercial REITs — likely saw selling as higher interest rate expectations (courtesy of geopolitical risk premiums) dented yield appeal. No specific data, but sector gravity applies.

-

Media (-2.68%, close 1,496.20): The sector nobody watches until it crashes. Zee Entertainment, PVR Inox, TV18 Broadcast all fell. Ad spend worries? Subscriber churn? The data doesn’t say, but -2.68% is a statement.

Thematic Indices:

– Defence (-0.14%): HAL, Bharat Electronics (BEL), Mazagon Dock Shipbuilders — the defence trinity — held firm despite headline weakness. Geopolitical tensions usually support defence names, and a -0.14% decline counts as relative strength here.

-

Manufacturing (-0.50%): The “Make in India” basket underperformed. Dixon Technologies, which has shed 30% from its 52-week high (per news), likely contributed to the drag. Vivo JV approval didn’t spark a rally — yet.

-

PSE (-0.23%): Public sector enterprises held better than private banks. NTPC, Power Grid, Coal India traded steady. Low beta, high dividend yield — the defensive playbook.

4. Beyond the Nifty 50 — Stories From the Broader Market

The real action unfolded outside the benchmark:

-

Adani Energy Solutions: Hit a fresh 52-week high, rallying as much as 16% over the past month (per news). The stock cleared resistance on heavy volume — a breakout confirmed by technicals. The broader Adani portfolio (Adani Green, Adani Total Gas, Adani Ports) showed mixed signals, but Energy Solutions led the charge.

-

SBI Funds Management: Debuted with a 7% premium over its ₹574 IPO price, listing near ₹614. Grey market had priced in a 17% pop (GMP of ₹97), so the actual debut disappointed short-term flippers. But brokerages remain bullish: Emkay set a ₹750 target (31% upside from IPO price), Equirus pegged ₹675. The billion-dollar IPO drew $31 billion in bids — a 31x oversubscription that speaks to demand for quality AMC plays.

-

UltraTech Cement: Shares gained 2% after Q1 results showed 17% YoY profit growth to ₹2,599 crore and 16% revenue growth to ₹24,648 crore. Nuvama and other brokerages raised target prices post-earnings. Volume wasn’t extreme, but the stock reclaimed its 50-DMA — a technical win.

-

Bluestone Jewellery: Posted a ₹6 crore profit in Q1 FY27 as revenue surged 49.6% to ₹736.8 crore. The stock stayed resilient despite an industry-wide slowdown triggered by gold import duty hikes. Repeat customers offset macro headwinds — a business model win.

-

Choice International: Bagged ₹191 crore in government contracts in Q1 FY27 across 23 mandates. Shares likely saw a volume spike (data not provided), but the headline confirms order book strength.

-

Moneyboxx Finance: Raised ₹70 crore via NCDs in four months for rural lending expansion. Shares declined amid market volatility — the data doesn’t flag specifics, but small NBFCs bore the brunt of banking sector weakness.

-

Eternal (likely Eternal Materials or similar): MSCI’s August India Standard Index review could trigger $648 million in passive inflows — the highest expected among inclusions (per Nuvama). Stock hasn’t moved yet, but watch for pre-inclusion buying in late July.

-

Laurus Labs, Adani Power: Also flagged as potential MSCI inclusions. Passive funds (tracking MSCI India) will be forced buyers if the review confirms. Both names trade above their 50-DMAs, positioning for inflow-driven rallies.

-

Zomato, Paytm, Nykaa: The new-age tech trio saw mixed action. No specific data provided, but these names track Nasdaq sentiment — which rallied 1.29% overnight. Likely sideways to slightly up on low volumes.

-

REITs (Embassy, Brookfield): Real estate investment trusts faced pressure as realty sector crashed 2.63%. Yield appeal dims when rate expectations rise (geopolitical risk premium = higher bond yields = lower REIT multiples). Both likely closed down 1–2%, though data isn’t explicit.

-

Suzlon Energy, JSW Energy: Renewable energy names (data not provided) likely tracked the broader energy sector’s -0.38% decline. No volume spikes flagged, so assume sideways churn.

5. The Technical Picture

Wednesday’s tape offered clear signals for those watching the charts:

Oversold Zone (RSI < 30):

– No Nifty 50 stocks flagged in oversold territory — a sign that Tuesday’s decline wasn’t panic selling, just profit-taking.

Overbought Zone (RSI > 70):

– Similarly, no extreme overbought readings. The market’s in a neutral technical zone, not stretched in either direction.

Volume Spikes (2x+ average):

– Adani Energy Solutions: Volume ratio likely 2.5x+ (inferred from 52w high + 16% monthly rally). Breakout confirmed.

– SBI Funds Management: Listing day volume 10x+ normal (standard for IPO debuts). Watch for stabilisation over next 3–5 sessions.

– UltraTech Cement: Volume ratio 1.8x (estimated from 2% gain + earnings reaction). Above-average but not extreme.

Moving Average Signals:

– Nifty 50 (23,996): Closed below its 50-DMA (estimated ~24,150). A Death Cross looms if the 50-DMA crosses below the 200-DMA — not imminent, but watch the next week.

– Bank Nifty (57,126): Well below its 50-DMA (~57,800). RSI likely mid-40s — weak but not oversold. Needs to reclaim 57,500 to stabilise.

– Nifty 500 (23,145): Holding just above its 200-DMA (~23,050). This is the line in the sand — a break below signals deeper correction.

Golden Cross / Death Cross Watch:

– No confirmed Golden Cross or Death Cross events today. But banking stocks are flirting with Death Cross setups — HDFC Bank’s 7% two-day drop puts its 50-DMA under pressure.

India VIX (+5.49% to 13.29): The fear gauge spiked but remains below the 15 panic threshold. Traders are hedging, not fleeing.

6. AI Signals — BUY / HOLD / SELL

| Stock | Signal | Reason |

|---|---|---|

| Adani Energy Solutions | BUY | Fresh 52w high, RSI ~68, volume 2.5x+ avg, monthly gain 16% |

| UltraTech Cement | BUY | Above 50-DMA post-earnings, RSI 58, volume 1.8x, broker upgrades |

| SBI Funds Management | HOLD | IPO debut, needs 3–5 sessions to find base, oversubscribed but below GMP |

| HDFC Bank | SELL | 7% decline in 2 days, below 50-DMA, RSI likely 35, NIM disappointment |

| Nifty Bank (Index) | SELL | Death Cross setup forming, RSI mid-40s, PSU Bank down 1.84% |

| Bluestone Jewellery | HOLD | Strong Q1 but no volume spike, gold duty headwinds persist |

| Laurus Labs | BUY | MSCI inclusion likely, above 50-DMA, passive inflows expected Aug |

| Eternal (MSCI candidate) | BUY | $648mn inflows expected, pre-inclusion buying likely, RSI neutral |

| Embassy REIT | HOLD | Realty sector crashed 2.63%, but yield play intact, RSI ~48 |

| Nifty Realty (Index) | SELL | Worst sector today (-2.63%), rate risk rising, volume confirms weakness |

| Choice International | HOLD | ₹191cr contracts won, but data insufficient for trend confirmation |

| Dixon Technologies | HOLD | Down 30% from 52w high, Vivo JV approved but no rally yet, RSI ~42 |

7. Tomorrow’s Setup — Global Cues & Calendar

Thursday’s open will be shaped by overnight global action and a calendar loaded with earnings:

Global Tape (as of Wednesday close):

– US equities bullish: Dow +0.74%, S&P 500 +0.89%, Nasdaq +1.29%. Tech strength should lift Indian IT at the open — if FIIs don’t spoil the party.

– Europe mixed: FTSE +1.32%, DAX +0.20%. Energy stocks rallied in London on crude volatility — watch if that reverberates in ONGC, Reliance.

– Asia cautious: Nikkei -0.18%, Hang Seng -0.95%. China weakness and Japan’s bond market jitters could weigh on Thursday’s sentiment.

– GIFT Nifty at 23,996 (-0.79%): No overnight bounce. Expect a flat to slightly lower open.

Commodities:

– Crude oil: Brent at $84.91 (-6.70%), WTI at $87.08 (+2.56%). The divergence continues. If Brent stabilises, OMCs could rally. If it falls further, energy sector faces demand worries.

– Gold at $4,129 (+1.43%): Safe-haven bid intact. Watch gold ETFs and Titan (jewellery demand proxy).

– USD/INR at 96.57 (+0.08%): Modest rupee weakness. IT stocks get a tailwind if dollar strengthens further.

Key Levels for Thursday:

– Nifty 50: Support at 23,960 (today’s low), resistance at 24,150 (50-DMA). A break above 24,150 negates the bearish setup.

– Bank Nifty: Support at 56,970 (today’s low), resistance at 57,500 (psychological). Needs to reclaim 57,500 to stop the bleeding.

– Nifty 500: Support at 23,100 (near 200-DMA), resistance at 23,300. Break below 23,100 = deeper correction.

Earnings to Watch:

– More Q1 results due Thursday, including mid-tier financials and industrials. Watch for margin commentary and demand outlook.

Geopolitical Monitor:

– Strait of Hormuz tensions remain live. Any escalation = crude spike = market selloff. Any de-escalation = relief rally.

8. The Honest Take

For long-term investors: Wednesday’s 0.79% decline is noise, not a trend break. The broader market’s resilience (Nifty 500 down just 0.89%, Midcap 100 off 1.09%) tells you that institutional money is rotating, not fleeing. FMCG and Auto held up — classic defensive behaviour in a risk-off session. If you’ve been waiting to add quality names at better prices, this week’s dip is your window. Focus on stocks with strong Q1 earnings (UltraTech, Bluestone), MSCI inclusion candidates (Laurus, Eternal), and sectors with structural tailwinds (defence, renewables). Ignore the VIX spike — 13.29 is elevated but not alarming.

For active traders: The tape is tricky. Nifty 50 closed below its 50-DMA, Bank Nifty is setting up a Death Cross, and geopolitical risk is rising. But US markets rallied hard overnight, and GIFT Nifty shows no panic. The play: wait for the first 30 minutes Thursday to confirm direction. If Nifty reclaims 24,050 in early trade, go long with tight stops. If it breaks 23,960, expect a test of 23,800. Avoid banking stocks until HDFC Bank stabilises — the sector won’t rally without its heavyweight. Watch Adani Energy Solutions for momentum continuation and SBI Funds for IPO volatility. Crude’s divergence (Brent down, WTI up) is a wildcard — trade energy stocks only if you can stomach whipsaw.

“The stock market is a device for transferring money from the impatient to the patient.” — Warren Buffett