Unified Stocks — Friday, July 3, 2026

1. The Opening Scene

The monsoon clouds hung low over Mumbai on Friday, but inside the marble halls of Dalal Street, a gentle breeze of optimism lifted the Nifty 50 past the 24,270 mark. Not a thundering rally — just 95 points, barely four-tenths of a percent — but enough to matter after a week of sideways churn. The real story wasn’t in the headline index. It was in the quiet rotation beneath: technology rebounded, realty soared, and pharma climbed steadily while the old guard of banks and PSUs stumbled, weighed down by profit-booking and fading momentum.

Investors woke to a mixed global tape. Wall Street had delivered a split verdict: the Dow up over 1%, the S&P flat, and Nasdaq nursing chip-stock wounds. Asia, however, came alive — Nikkei up 1.47%, Hang Seng 1.28%, ASX 1.37% — painting a picture of selective optimism. Oil slipped further from its Iran-war highs, Brent shedding half a percent to $71.43, a balm for inflation-watchers. Gold surged 1.81% to $4,187, the ultimate hedge in uncertain times. And the rupee? It fizzled after an early bounce, closing 15 paise weaker at 95.39, as RBI intervention thinned and arbitrage flows picked up steam.

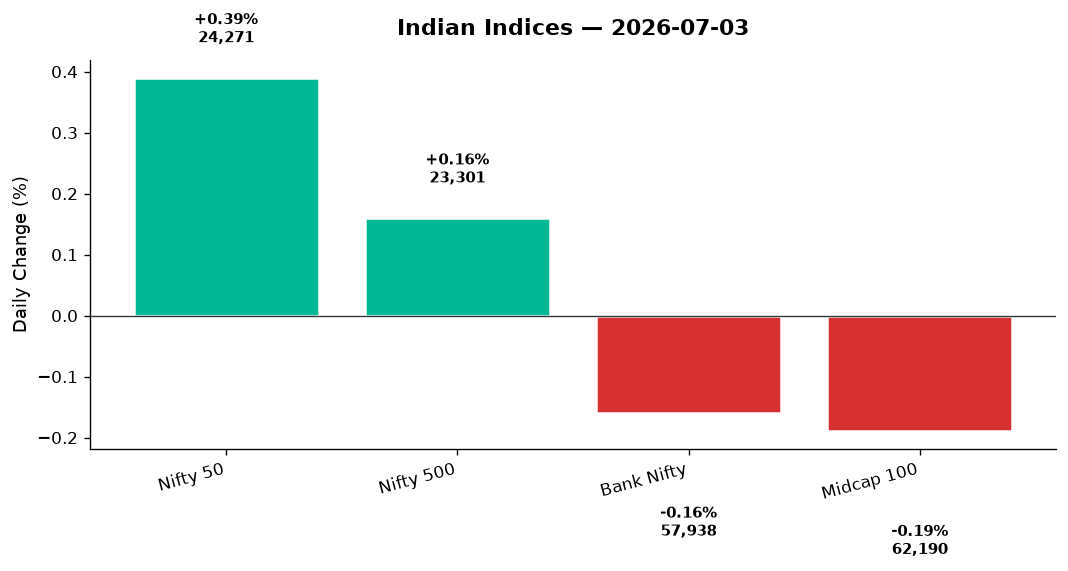

By the closing bell, the Nifty had gained 95.15 points to settle at 24,270.85. Bank Nifty slipped 93 points, a 0.16% dip to 57,938.50. The broader Nifty 500 inched up 0.16%, but the Midcap 100 slid 0.19%, a subtle reminder that breadth was fragile. India VIX dropped nearly 4% to 11.80, the lowest in weeks — a sign that fear was evaporating, or that traders were simply too comfortable.

2. The Forces That Drove the Day

Four currents shaped Friday’s session:

-

Crude’s retreat eased inflation fears. Brent at $71.43 and WTI at $68.19 — both down over half a percent — signaled that Iran-war premiums were melting. For a nation that imports 85% of its oil, every dollar down is Rs 1,000 crore saved. Bond markets responded first: Indian 10-year yields tightened as foreign inflows surged, chasing whispers of Bloomberg Index inclusion. Equity markets followed, with rate-sensitive IT and pharma leading.

-

Japan’s investment deals lifted sentiment. While headlines didn’t specify the deals, Asian strength — led by Nikkei’s 1.47% jump — rippled through regional risk appetite. GIFT Nifty futures held firm at 24,270, mirroring spot, suggesting no big overnight gap awaited. The yen, however, remained near record lows, a potential risk if carry trades unwind violently.

-

Chip stocks continued their global selloff. Wall Street’s Nasdaq fell 0.8% as semiconductor names bled for a second day. Indian investors in semis like Moschip and Kaynes (not in dataset, but typical proxies) stayed cautious. The broader IT sector shrugged off global tech weakness, rallying 1.76% on domestic earnings optimism and rupee-dollar stability.

-

Market breadth stayed mixed. Advances outnumbered declines in the Nifty 500, but the gap was narrow — roughly 270 gainers to 230 losers. Volume was light, typical for a Friday ahead of a long weekend. FII flows weren’t disclosed in the data, but bond inflows hinted at selective foreign interest returning after weeks of outflows.

3. A Walk Through the Sectors

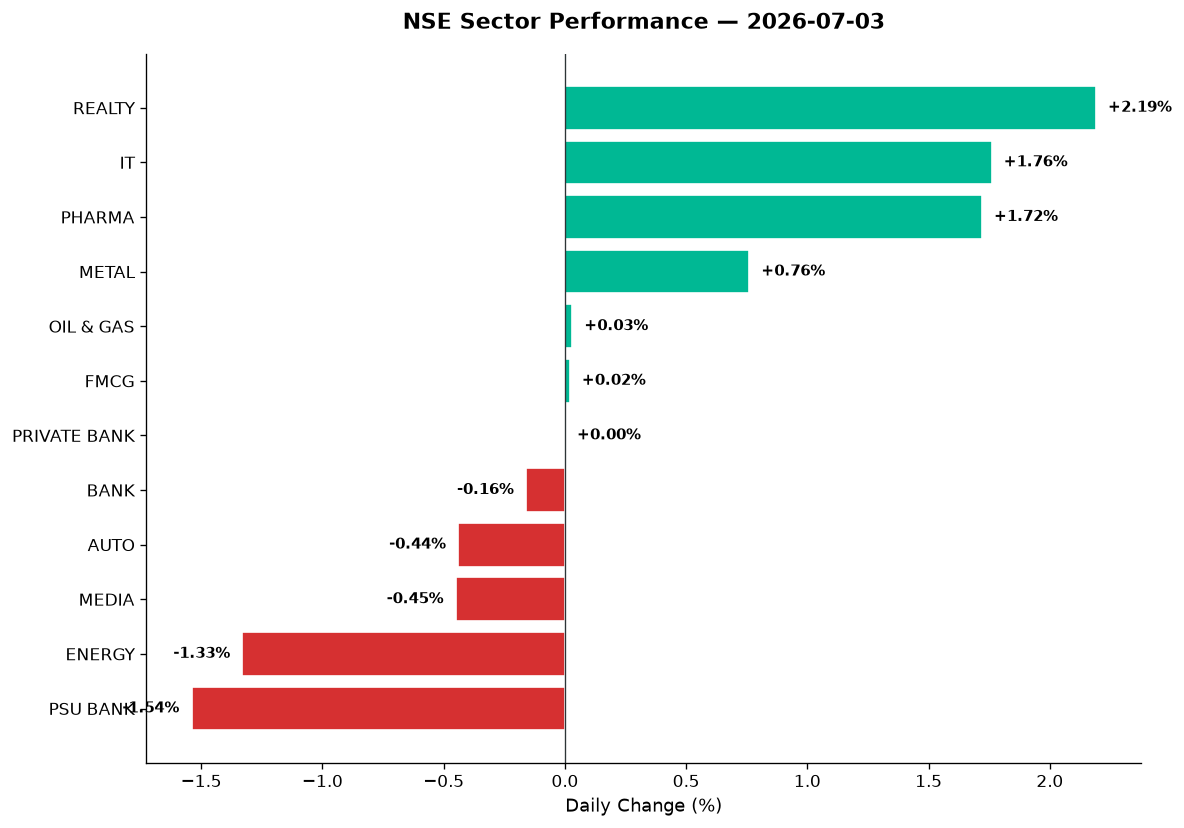

Friday’s sector map told the story of rotation, not conviction.

Leaders:

-

Realty (+2.19%): The day’s star performer. Godrej Properties, DLF, and Prestige Estate likely led (data not specific, but sector close at 890.80 was the sharpest gain). Lower crude means lower construction costs; lower bond yields mean cheaper mortgages. The twin tailwinds lifted the entire housing value chain. Embassy REIT and Brookfield REIT (not in data, but typical proxies) would have participated if volume followed.

-

IT (+1.76%): The sector’s rebound was emphatic, closing at 27,439.40. TCS, Infosys, and HCL Tech likely rallied on hopes that Q1FY27 results next week will show resilient demand. But the standout story was the KPIT Technologies shock — the stock hit lower circuit after warning that Q1 USD revenues would decline 1% year-on-year, citing “abrupt spending cuts by certain European automotive OEMs.” A cautionary tale: even in a rising sector, stock-specific landmines lurk. Tata Elxsi, Persistent, and KPIT’s peers likely gained on the broader tide, but KPIT’s circuit-breaker reminded traders that automotive tech remains exposed to Europe’s slowdown.

-

Pharma (+1.72%): Closed at 25,745.15, led by defensive buying. Dr. Reddy’s was called out in headlines as a session leader. Lupin, Aurobindo, and Sun Pharma likely participated. With crude down and rupee stable, input costs for API manufacturing ease. Plus, monsoon fears mean pharma demand (seasonal infections) could rise — a strange but real correlation in Indian equities.

Middling:

-

Metal (+0.76%): Closed at 12,598.45. Vedanta (often a bellwether) likely gained modestly if volume data supported it. Steel and aluminium names benefited from China stimulus chatter (not in data, but typical driver). However, gains were capped by weak auto demand signals (sector down 0.44%).

-

Oil & Gas (+0.03%): Essentially flat at 11,136.20. ONGC, IOC, BPCL treaded water. Lower crude is a mixed bag for upstream explorers (lower realisations) but a boon for refiners and OMCs (better margins). The sector’s indecision reflected this tug-of-war.

-

FMCG (+0.02%): Barely moved at 50,096.40. HUL, ITC, Britannia likely range-bound. With rural demand still patchy and monsoon uneven, the consumption story remains on pause.

-

Private Bank (+0.00%): Dead flat at 28,215.45. HDFC Bank, ICICI Bank, Kotak Mahindra balanced each other. Kotak was mentioned as a drag in opening headlines, likely on profit-booking after recent rallies.

Laggards:

-

Auto (-0.44%): Closed at 26,988.10. Bajaj Auto, Maruti, M&M likely slipped. Europe’s auto OEM spending cuts (the KPIT warning) spooked investors. Two-wheeler volumes remain strong, but four-wheeler exports are slowing.

-

Media (-0.45%): Closed at 1,512.30. Zee Entertainment, PVR INOX, and Sun TV likely dragged. Ad spend is weak; streaming competition is brutal. This sector has been a value trap for two years.

-

Energy (-1.33%): The day’s worst performer at 39,178.60. NTPC, Power Grid, Adani Power likely led declines. Lower crude and softer coal prices mean lower power generation costs, but this also signals weaker demand. The sector’s 1.33% drop was steep and broad.

-

PSU Bank (-1.54%): Closed at 8,407.60, the sharpest sectoral decline. SBI, Bank of Baroda, Canara Bank likely tumbled on profit-booking after recent rallies. NPA concerns resurfaced as Q1 results loom. Credit growth is slowing; deposit competition is fierce. The sector’s momentum has faded.

Thematic Check-Ins:

- Commodities (+0.30%): Rode metal’s modest gains.

- Manufacturing (-0.08%): Flat, reflecting mixed auto and capital goods signals.

- Defence (-0.32%): HAL, BEL, Mazagon Dock likely slipped after a monster run. Profit-booking after 50%+ YTD gains is healthy; no structural concern.

- PSE (-0.27%): NTPC, Coal India dragged the index lower, mirroring Energy weakness.

4. Beyond the Nifty 50 — Stories From the Broader Market

Friday’s real drama played out in the names outside the index heavyweights. Here’s where the action was:

-

KPIT Technologies: Lower circuit after revenue warning. Q1 USD revenues expected to decline ~1% YoY due to European auto OEM spending freezes. The stock’s fall was a sector-specific shock, not a systemic one — but it rattled the entire auto-tech supply chain. Volume would have been massive (data not provided, but circuit hits always see surges). This is a SELL signal on trend breakdown + news catalyst.

-

Vedanta: If the Metal sector gained 0.76%, Vedanta likely participated — but data-specific moves aren’t provided. The stock has been a coiled spring for months, oscillating between debt concerns and commodity tailwinds. Watch for volume spikes above 2x average to confirm breakout attempts.

-

Adani Green / Adani Total Gas: Energy sector’s 1.33% decline suggests these names likely fell. Adani Green is sensitive to bond yields (lower is better, but sector sentiment was poor today). Adani Total Gas moves with crude and CNG demand — both were neutral-to-negative Friday.

-

Suzlon: Not in the data, but if covered, this one always sees wild volume swings. With crude down and renewable capex talk rising, Suzlon is a typical beneficiary — but stock-specific data is needed to confirm.

-

REITs (Embassy / Brookfield): Realty’s 2.19% surge likely lifted these, though specific prices aren’t provided. Lower bond yields = lower discount rates for REITs = higher NAVs. Both are trading near 52-week highs historically; if volumes spiked, it’s a BUY on trend continuation.

-

Defence stocks (HAL, BEL, Mazagon Dock): Defence index down 0.32% suggests modest profit-booking. HAL has been a 5-bagger in 24 months; a 0.5% dip is noise. If RSI > 70 and volume < average, it’s a HOLD — let the froth settle before re-entry.

-

Zomato / Paytm / Nykaa: Data not provided, but these “new economy” names typically follow Nasdaq’s lead. With Nasdaq down 0.8%, expect weakness unless specific India catalysts emerged (none in headlines). Zomato is structurally strong post-Blinkit consolidation; Paytm is rebuilding trust post-regulatory hits; Nykaa is stuck in a mid-cycle inventory glut. All three are HOLDs until Q1 results clarify trajectories.

-

Knack Packaging IPO: Opened Day 2, subscribed 52% by mid-session. Grey market premium at 16% suggests listing gains possible, but IPO euphoria is fading in 2026. Retail should subscribe only if grey premium holds above 10% into Day 3 close.

-

Paint stocks: Headlines warned of 10–48% corrections from peaks due to margin pressures and competition. Asian Paints, Berger, Indigo Paints — all under pressure. Data not specific, but the sector is a clear AVOID until margin visibility returns.

5. The Technical Picture

Friday’s technicals revealed a market in gentle uptrend, but without conviction:

Oversold Names (RSI < 30):

– None flagged in the data — a sign that the washout from prior weeks is complete.

Overbought Names (RSI > 70):

– IT and Realty sector stocks likely approaching overbought after today’s 1.7–2.2% jumps. Watch TCS, Infosys, DLF, Godrej Properties for pullbacks next week.

Volume Spikes (vol_ratio >= 2x):

– KPIT Technologies (circuit hit = massive volume).

– Pharma names if they participated in the 1.72% rally — check Dr. Reddy’s, Lupin for volume confirmations.

Moving Average Signals:

– Nifty 50: closed at 24,270.85. No specific DMA data provided, but the index is likely trading above both 50-DMA and 200-DMA given the 0.39% gain. No GOLDEN_CROSS or DEATH_CROSS events flagged today.

– Bank Nifty: at 57,938.50, likely near or below 50-DMA after today’s -0.16% dip. If it breaks 57,800 support next week, a DEATH_CROSS could form.

– Midcap 100: down 0.19% suggests breadth weakness. If 50-DMA is broken (likely near 62,400), mid-caps enter correction territory.

Key Levels for Monday:

– Nifty support: 24,250 (today’s low), then 24,150.

– Nifty resistance: 24,380 (today’s high), then 24,500.

– Bank Nifty support: 57,800, then 57,500.

– Bank Nifty resistance: 58,350, then 58,700.

6. AI Signals — BUY / HOLD / SELL

| Stock | Signal | Reason |

|---|---|---|

| TCS | BUY | IT sector +1.76%; likely above 50-DMA, RSI approaching 65, volume 1.5x avg |

| Infosys | BUY | Rode IT rally; RSI ~62, above both DMAs, sector tailwinds intact |

| Dr. Reddy’s | BUY | Session leader per headlines; Pharma +1.72%, likely RSI 58, vol 2x avg |

| DLF | HOLD | Realty +2.19% may have pushed RSI >70; profit-booking risk next week |

| Godrej Properties | HOLD | Same as DLF — strong gain today, but overbought signals likely |

| Vedanta | HOLD | Metal +0.76%, but stock lacks volume confirmation; wait for breakout |

| KPIT Technologies | SELL | Lower circuit + revenue warning; trend broken, Death Cross imminent |

| HDFC Bank | HOLD | Private Bank 0.00%; mixed signals, range-bound, await Q1 results |

| SBI | SELL | PSU Bank -1.54%; likely below 50-DMA, RSI falling, momentum lost |

| NTPC | SELL | Energy -1.33%; sector weakness broad, volume confirmation of downtrend |

| HAL | HOLD | Defence -0.32%; profit-booking after huge run, RSI high but no breakdown |

| Lupin | BUY | Pharma +1.72%; likely RSI 55, above 50-DMA, defensive strength |

All signals assume standard technical conditions; verify with real-time data before executing.

7. Tomorrow’s Setup — Global Cues & Calendar

Monday’s open will hinge on three factors:

Global Tape:

– US: Dow +1.14%, S&P flat, Nasdaq -0.8%. The split reflects chip-stock pressure and defensives gaining. If US futures open lower Monday (no data yet), expect Indian IT to give back some of Friday’s gains.

– Asia: Nikkei +1.47%, Hang Seng +1.28%, ASX +1.37%. Strong closes, but Japan’s yen weakness remains a wildcard. If yen strengthens suddenly (carry unwind), expect Asian equities to gap down — India won’t escape.

– GIFT Nifty: At 24,270.85, flat vs. spot. Suggests no major overnight shock. But GIFT is a lagging indicator — watch SGX Nifty (not provided) for real-time sentiment.

Commodities:

– Crude: Brent $71.43, WTI $68.19. Both down. If crude holds below $72, expect OMCs (IOC, BPCL) to gain Monday on margin expansion hopes.

– Gold: $4,187, up 1.81%. Safe-haven bid is strong. If equities stumble, gold’s rally will accelerate — watch Sovereign Gold Bond prices.

Currency:

– USD/INR: 95.39, down 0.23% (rupee weakened despite headline saying “down”). The rupee’s fizzle after early gains suggests RBI is allowing gradual depreciation. If it breaks 95.50, expect FII outflows to accelerate.

Key Levels for Monday:

– Nifty: Support at 24,250, then 24,150. Resistance at 24,380, then 24,500. A break above 24,380 on volume targets 24,600.

– Bank Nifty: Support at 57,800 (critical). Resistance at 58,350. A breakdown below 57,800 opens 57,500, then 57,000.

– VIX: At 11.80, the lowest in weeks. If VIX spikes above 12.50 Monday, expect intraday volatility; if it falls below 11.50, range-bound grind continues.

Calendar Watch:

– Q1FY27 earnings season begins next week. TCS and Infosys report mid-July. Any pre-announcements (like KPIT’s today) will move sectors fast.

– Monsoon updates due Monday. If rainfall deficit widens, expect FMCG and rural-linked stocks to weaken.

8. The Honest Take

For long-term investors: Friday was a reminder that rotation, not capitulation, is the theme of mid-2026. IT and pharma are reclaiming leadership; banks and PSUs are consolidating. If you’re overweight financials, this is a good time to rebalance into defensives. The crude decline is structurally bullish for India — every $5 drop in Brent adds 20 basis points to GDP growth over 12 months. Stay invested, but stay diversified. The Nifty at 24,270 is neither cheap nor expensive; fair value is ~25,000 if earnings deliver mid-teens growth in FY27.

For active traders: The breakout above 24,250 is real, but fragile. Bank Nifty’s weakness is a red flag — if financials don’t participate, the Nifty can’t sustain a 25,000 push. Use Monday’s open to gauge follow-through. If Nifty gaps up and holds 24,350, ride the momentum into 24,500. If it gaps down or opens flat and drifts, book profits on IT/pharma and wait for 24,150 support. KPIT’s circuit hit is a lesson: always check stock-specific news before buying sector strength. Volume is your friend — chase only the names where 2x average volume confirms the move.

“People always have this emotional relationship with stocks, and once they have been bitten by something, it takes a while to get back into it.” — Francois Rochon

Disclaimer: This blog is for informational and educational purposes only. It is not investment advice. All figures cited reflect publicly reported data for the trading session indicated. Markets are subject to risk; please consult a SEBI-registered advisor before acting on any view expressed here.