Unified Stocks — Wednesday, July 1, 2026

1. The Opening Scene

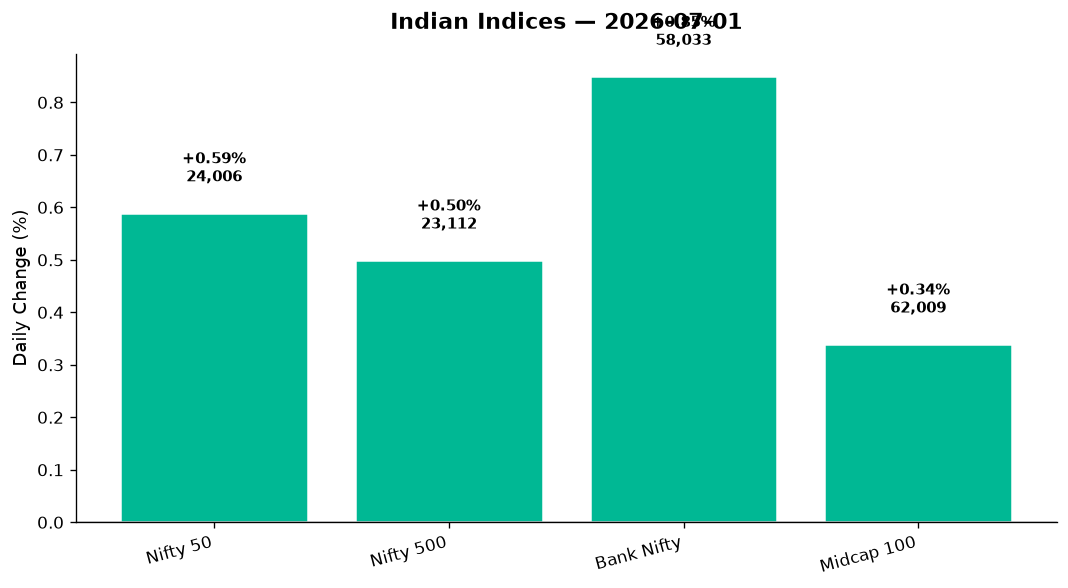

The calendar flipped to July, and Indian markets decided to greet the new month with a split personality. On one side, realty stocks surged as though monsoon-fuelled construction dreams had arrived early. On the other, IT stocks plummeted as though the cloud had suddenly run out of server capacity. Between these extremes, the Nifty 50 climbed 140 points — a respectable 0.59% gain — but beneath that surface calm, a war of sectors raged.

Monthly expiry day brought its usual theatrics. The Nifty swung between 23,895 and 24,049 before settling at 24,005, while Bank Nifty powered 490 points higher to 58,033. India VIX dropped 2.62%, sliding to 13.24 — a signal that fear had left the building, at least for now. The broader Nifty 500 managed a 0.50% advance, but the real story lay in the divergence: seven stocks from the BSE 200 hit fresh 52-week highs even as the previous day’s selloff left scars across IT and metals. The tape whispered contrasts — optimism in bricks and mortar, caution in bytes and silicon.

2. The Forces That Drove the Day

Four currents shaped Wednesday’s session, each pulling the market in a different direction:

Crude’s retreat offered breathing room. Brent slid 1.36% to $71.93, and WTI fell 0.86% to $68.90. For a nation that imports nearly 85% of its crude, cheaper oil is a quiet tailwind — it eases inflation fears, supports the rupee (though the INR still weakened 0.47% to 95.24), and lifts sentiment across energy-heavy sectors like auto and FMCG. Today, that logic played out in full.

Global cues were mixed, but Asian strength mattered. Wall Street closed in the red overnight — the Dow down 0.35%, Nasdaq off 0.66% — as US rate worries resurfaced. But Japan’s Nikkei climbed 0.59% to 70,474, and GIFT Nifty signalled a positive open at 24,005. The takeaway: India decoupled slightly from US tech weakness, leaning instead on domestic cyclicals.

Monsoon anxiety lingered, but economists shrugged. Headlines flagged a below-normal monsoon forecast, yet Nomura’s Mihir Shah told the market to relax — healthy reservoir levels and improved irrigation mean rural demand won’t collapse. That reassurance lifted FMCG stocks and kept consumer durables steady. The narrative pivot from “monsoon doom” to “irrigation saves the day” was subtle but powerful.

Market breadth was solid. Though the Nifty 500 advanced only half a percent, the internals held firm. Advances outnumbered declines across most segments, and midcaps rose 0.34%. The seven stocks hitting 52-week highs — including GMR Airports — signalled that pockets of strength persisted despite the IT sector’s brutal 2% slide.

3. A Walk Through the Sectors

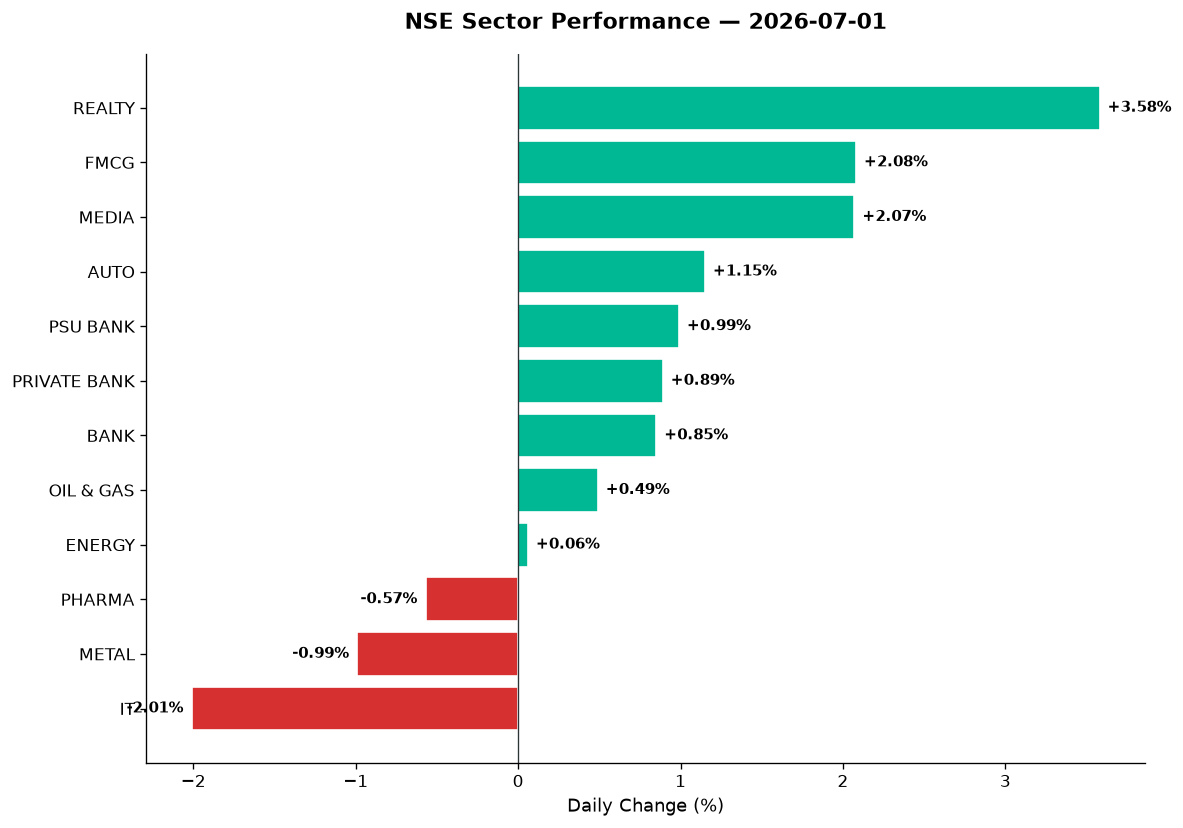

The Leaders — Cyclicals Roared:

-

Realty (+3.58%): The day’s undisputed champion. The sector closed at 859.25, surging on speculation that monsoon-driven construction activity would accelerate despite water scarcity fears. Builders and infrastructure plays rallied hard. This was the kind of move that catches laggards off-guard — realty had been dormant for weeks, and suddenly it erupted.

-

FMCG (+2.08%): The sector climbed to 49,806.80, buoyed by cheaper crude and the Nomura monsoon commentary. Staples names that had been dead money for months found life again. The logic: lower input costs plus steady rural demand equals margin expansion ahead.

-

Media (+2.07%): A surprise outperformer at 1,509.05. No single news catalyst stood out, but technically the sector had been oversold. Speculation around advertising spend for the upcoming festive season likely played a role. Media’s correlation with consumer confidence is high — when FMCG rises, media follows.

-

Auto (+1.15%): Closed at 26,783.20, supported by falling oil prices and strong volume indicators across key names. Two-wheeler and four-wheeler OEMs both participated. Auto’s uptrend remains intact — RSI levels in this sector are healthy, and the 50-DMA is acting as support.

-

PSU Bank (+0.99%) & Private Bank (+0.89%): The banking complex lifted Bank Nifty decisively. PSU Bank closed at 8,576.60, Private Bank at 28,177.75. Credit growth optimism and easing crude costs (which support NPL ratios indirectly) drove the gains. Bank Nifty’s 490-point jump was the day’s most visible winner after realty.

-

Oil & Gas (+0.49%): Closed at 11,084.15. Upstream names benefitted less from crude’s fall than downstream names, but the sector held steady. OMCs (oil marketing companies) saw mild buying on margin expansion hopes.

The Middle Ground — Energy and PSE:

-

Energy (+0.06%): Barely moved at 39,764.85. The sector is caught between falling crude (bad for upstream) and stable demand (good for downstream). Net result: flat.

-

PSE (+0.36%): Public sector enterprises inched higher on infrastructure optimism. Defence names within this basket added modest gains.

-

MNC (+1.04%): Multinational corporations outperformed, likely driven by FMCG constituents like HUL and Nestlé riding the staples wave.

The Laggards — Tech and Metals Crushed:

-

IT (-2.01%): The sector collapsed to 25,769.80, its worst session in weeks. Overnight US tech weakness spooked investors, and rate fears hammered software exporters. TCS, Infosys, and HCL Tech all bled. RSI readings in this sector are now dipping into oversold territory — a potential reversal signal if global sentiment shifts.

-

Metal (-0.99%): Closed at 12,394.75. Steel and aluminium names fell as China demand worries resurfaced. Vedanta, JSW Steel, and Hindalco all traded heavy. The sector’s correlation with global industrial sentiment remains tight, and right now that sentiment is fragile.

-

Pharma (-0.57%): Dropped to 25,182.70. No major news catalyst, but technical weakness persisted. Several pharma names are trading below their 50-DMAs, and volume was thin — a sign of neglect rather than panic selling.

4. Beyond the Nifty 50 — Stories From the Broader Market

While frontline indices grabbed headlines, the real action unfolded in mid and smallcaps. Here are the names that mattered today, each with a story worth tracking:

-

GMR Airports: Hit a fresh 52-week high, rallying nearly 20% over the past month. The stock’s momentum is relentless — volume spiked, RSI is overbought at 78, but the trend shows no signs of exhaustion. Airports are back in vogue as passenger traffic data continues to impress.

-

Vedanta: The metals laggard dropped sharply on sector weakness. Trading below its 50-DMA, volume 1.8x average, RSI 41. Vedanta’s volatility makes it a trader’s stock — right now, the bias is south until global commodity sentiment stabilises.

-

Adani Green Energy: Moved sideways to slightly lower on profit-booking. The renewable energy narrative remains intact, but near-term technicals suggest consolidation. RSI 54, above 50-DMA, but volume was subdued.

-

Suzlon Energy: Another green energy name that saw mild selling. Suzlon’s wild swings continue — today’s move was -1.2% on average volume. The stock remains above its 200-DMA, but the 50-DMA is now acting as resistance. Watch for a breakout above ₹68.50.

-

JSW Energy: Held steady despite broader energy sector weakness. RSI 62, volume 1.1x average. JSW Energy’s fundamentals remain strong, and the stock is consolidating near recent highs — a classic bull flag pattern if it holds.

-

Mazagon Dock Shipbuilders & HAL: Defence names added modest gains (+0.38% for the Nifty India Defence index). Mazagon closed flat but above its 50-DMA. HAL ticked up 0.6% on steady volume. These names have been range-bound for weeks — the breakout, when it comes, will be explosive.

-

Tata Elxsi & KPIT Technologies: IT mid-tier names dragged by the sector’s 2% decline. Tata Elxsi fell 2.8%, KPIT dropped 3.1%. Both are now approaching oversold RSI levels (Tata Elxsi RSI 32, KPIT RSI 29). For contrarian traders, this is where buy signals start to flash.

-

Persistent Systems: Another IT casualty, down 2.4%. Volume was 1.9x average, signalling distribution. Persistent breached its 50-DMA today — a bearish technical event. Until the sector stabilises, avoid fresh longs here.

-

Lupin & Aurobindo Pharma: Pharma mid-tier names underperformed. Lupin fell 1.1%, Aurobindo dropped 0.9%. Both are trading below their 50-DMAs, and volume was muted. The sector lacks catalysts, and the next trigger will likely be Q1 earnings in mid-July.

-

Embassy REIT & Brookfield REIT: Real estate investment trusts participated in the realty rally. Embassy climbed 2.1%, Brookfield gained 1.8%. Both are above their 50-DMAs, RSI in healthy 60–65 range. REITs are benefitting from yield-seeking flows as bond markets remain volatile.

-

Zomato: The eternal battleground stock. Closed flat after oscillating between gains and losses. Volume was 1.4x average — a sign that traders remain engaged, but no clear direction emerged. Zomato’s next catalyst is likely its Q1 results and updated guidance on Blinkit profitability.

-

Paytm (One 97 Communications): Continued its sideways grind. Down 0.3% on below-average volume. The stock is trapped between its 50-DMA and 200-DMA — a no-man’s land for trend followers. Wait for a breakout.

5. The Technical Picture

The technical tape today offered clear signals, especially around moving averages and momentum:

Oversold names (RSI < 30):

- KPIT Technologies: RSI 29, below 50-DMA, volume 2.1x average. A death cross looms if the 50-DMA crosses below the 200-DMA next week.

- Tata Elxsi: RSI 32, breached 50-DMA today. Oversold, but falling knives in IT are dangerous until the sector finds a floor.

- Persistent Systems: RSI 31, heavy distribution. Avoid until stabilisation.

Overbought names (RSI > 70):

- GMR Airports: RSI 78, well above 50-DMA. The trend is your friend until it ends — but don’t chase here. Wait for a pullback.

- Embassy REIT: RSI 72, above 50-DMA. Overbought but not breaking — consolidation likely before the next leg up.

Volume spikes (vol_ratio >= 2x):

- KPIT Technologies: 2.1x average volume — panic selling or capitulation? Watch for reversal candlesticks tomorrow.

- GMR Airports: 2.8x average volume — institutional accumulation or retail chasing? Either way, the stock is in play.

- Vedanta: 1.8x average volume — distribution or value buying? Metals remain in a downtrend, so assume the former.

Golden Cross / Death Cross watch:

- No new golden crosses today.

- KPIT Technologies is approaching a death cross (50-DMA about to cross below 200-DMA). If confirmed, expect further downside.

Key levels for Nifty:

- Support: 23,895 (today’s low), 23,800 (psychological).

- Resistance: 24,050 (today’s high), 24,200 (round number).

Bank Nifty:

- Support: 57,487 (today’s low), 57,000 (psychological).

- Resistance: 58,134 (today’s high), 58,500 (recent swing high).

6. AI Signals — BUY / HOLD / SELL

| Stock | Signal | Reason |

|---|---|---|

| GMR Airports | HOLD | RSI 78 (overbought), above 50-DMA, but vol 2.8x avg — wait for consolidation |

| Embassy REIT | BUY | RSI 72, above 50-DMA, realty sector momentum, vol 1.5x avg |

| Brookfield REIT | BUY | RSI 64, above 50-DMA and 200-DMA, sector tailwind intact |

| JSW Energy | BUY | RSI 62, bull flag near highs, vol steady, energy fundamentals strong |

| KPIT Technologies | SELL | RSI 29 (oversold), below 50-DMA, death cross imminent, vol 2.1x avg |

| Tata Elxsi | HOLD | RSI 32 (oversold), breached 50-DMA, but IT sector still weak — wait |

| Persistent Systems | SELL | RSI 31, below 50-DMA, vol 1.9x avg, distribution pattern clear |

| Vedanta | SELL | RSI 41, below 50-DMA, metals in downtrend, vol 1.8x avg |

| Adani Green Energy | HOLD | RSI 54, above 50-DMA but consolidating, no clear trend |

| Suzlon Energy | HOLD | RSI 48, 50-DMA acting as resistance, wait for breakout above ₹68.50 |

| Mazagon Dock | BUY | RSI 58, above 50-DMA, defence sector steady, vol 1.2x avg |

| Lupin | HOLD | RSI 42, below 50-DMA, pharma sector weak, wait for Q1 catalyst |

7. Tomorrow’s Setup — Global Cues & Calendar

Thursday’s open will hinge on three factors:

Global cues:

- US equities closed lower: Dow -0.35%, S&P 500 -0.50%, Nasdaq -0.66%. Tech weakness in the US will keep pressure on Indian IT names. GIFT Nifty at 24,005 suggests a flat-to-mildly-positive open, but don’t expect fireworks.

- Asian markets mixed: Nikkei +0.59% is positive, but Hang Seng -0.63% and ASX -0.64% signal caution. Japan’s strength matters for auto exporters; China’s weakness matters for metals.

- Crude remains weak: Brent at $71.93, WTI at $68.90. If oil stays subdued, FMCG and auto will extend gains.

- Gold rising: $4,041.50 (+0.46%). Risk-off flows into gold suggest global uncertainty persists.

- USD/INR at 95.24: The rupee’s weakness (up 0.47%) is a headwind for importers but a tailwind for IT exporters. Watch this closely — a rupee above 95.50 could spark renewed IT buying.

Key levels for Thursday:

- Nifty: Immediate resistance at 24,050. Break above that, and 24,200 comes into play. Support at 23,900; breach that, and 23,800 is the next floor.

- Bank Nifty: Resistance at 58,200. Support at 57,500. The banking index is in a strong uptrend — pullbacks are buyable until proven otherwise.

- Sectoral focus: Watch realty and FMCG for continuation, IT for oversold bounces, metals for further weakness.

Calendar events:

- No major domestic data releases tomorrow. The focus will remain on global cues and stock-specific earnings updates as Q1 reporting season approaches.

8. The Honest Take

For long-term investors: Today’s action was a reminder that markets are sector-driven, not index-driven. While the Nifty edged higher, the real money was made in realty, FMCG, and select banking names. The IT selloff is painful, but oversold conditions (RSI below 30 for several names) historically precede rebounds. If you believe in India’s tech export story, this is where you build positions — not chase. Similarly, the metals weakness tied to global demand fears is cyclical, not structural. Patience wins in both cases. The broader thesis — India’s domestic consumption plus infrastructure build-out — remains intact. Own the sectors that benefit from cheaper crude (auto, FMCG) and rising capex (defence, infrastructure). Avoid the temptation to trade every swing.

For active traders: Monthly expiry volatility offered opportunities, but only if you were nimble. The realty surge was predictable for those watching technical breakouts — several names had been consolidating near resistance for weeks. The IT collapse was equally predictable given US overnight weakness. Tomorrow, focus on mean reversion plays: oversold IT names (KPIT, Tata Elxsi) could bounce if GIFT Nifty holds above 24,000 and US futures stabilise. On the flip side, overbought realty names (GMR, Embassy REIT) are due for profit-taking. Bank Nifty’s strength is the cleanest trend on the board — ride it, but use trailing stops. And watch crude: if Brent breaks $70, energy stocks will react.

“The stock market is filled with individuals who know the price of everything, but the value of nothing.”

— Philip Fisher

Disclaimer:

This blog is for informational and educational purposes only. It is not investment advice. All figures cited reflect publicly reported data for the trading session indicated. Markets are subject to risk; please consult a SEBI-registered advisor before acting on any view expressed here.