Unified Stocks — Wednesday, June 24, 2026

1. The Opening Scene

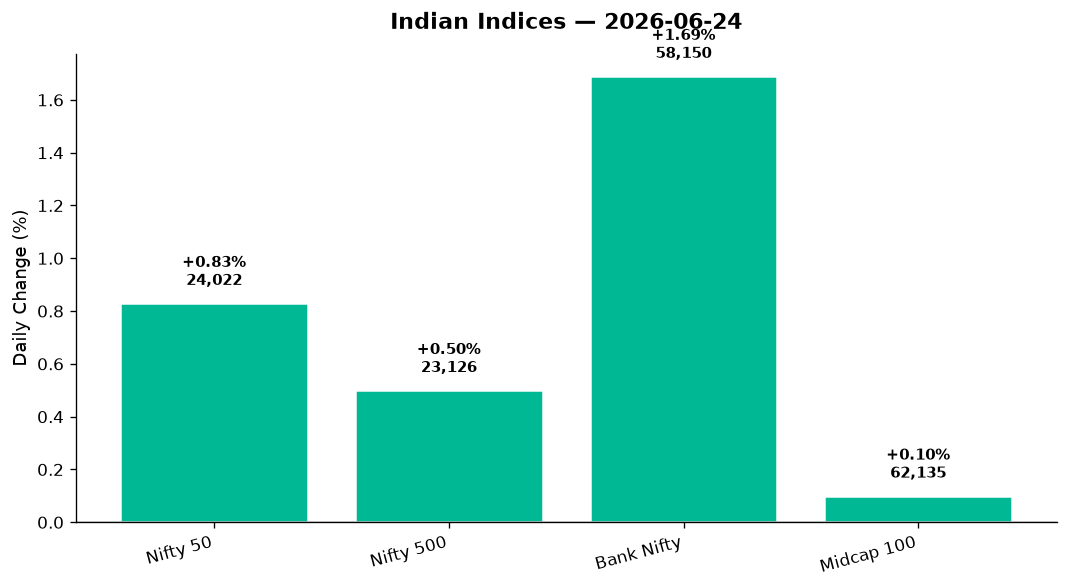

Two markets lived inside Wednesday’s session. In one, American tech giants stumbled through the night—Nasdaq down 2.21%, S&P 500 shedding 1.44%—leaving Asian bourses nursing fresh wounds. In the other, Indian equities shrugged off the gloom like monsoon clouds parting over Mumbai, with the Nifty 50 climbing 197 points to 24,021. Bank Nifty surged nearly 1000 points. The VIX, that faithful barometer of fear, dropped 4% to 13.39, its lowest close in weeks.

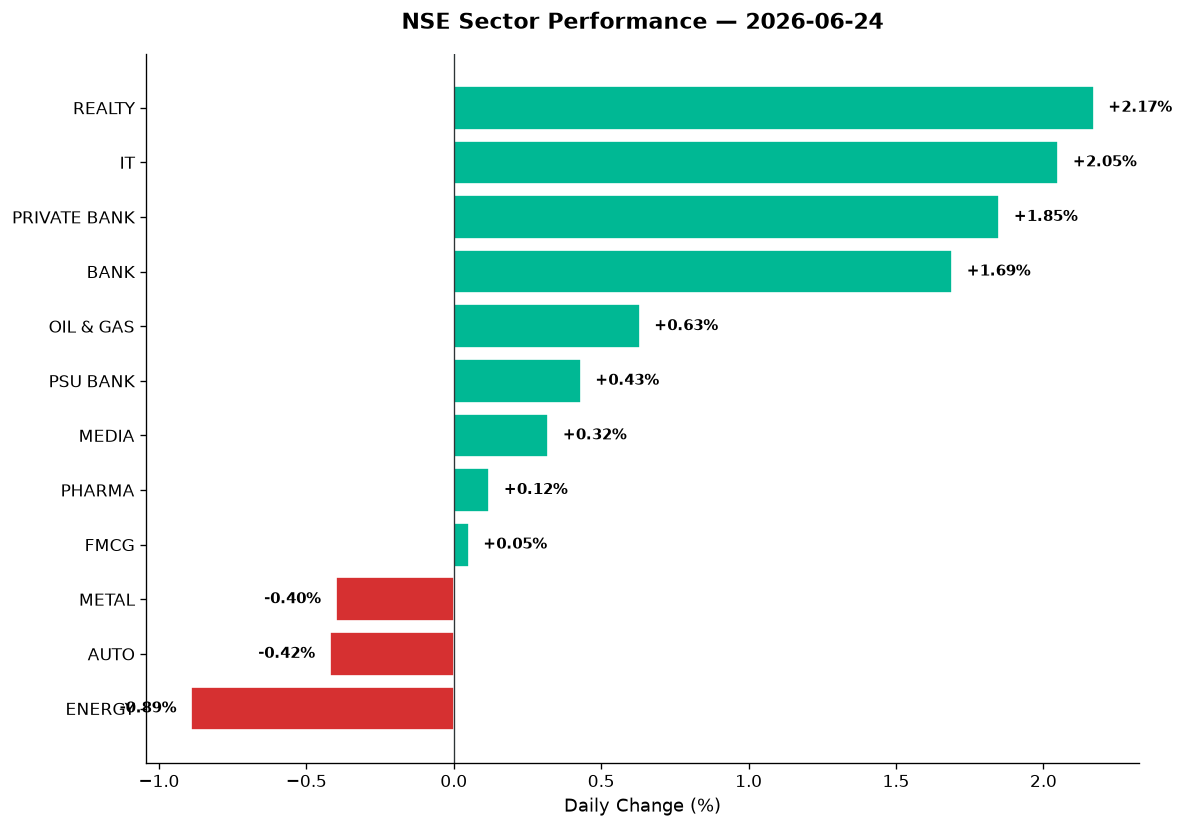

It was a day of selective aggression. While defence stocks nursed a 1.97% drubbing and energy names sagged under the weight of crude’s 3.6% overnight collapse, private banks and IT counters staged a spirited comeback. Realty led the charge, up 2.17%, as if daring the bears to a duel. The advance-decline ratio tilted positive across the Nifty 500, but only just—suggesting this wasn’t a broad-based rally so much as a tactical rotation into oversold pockets. By the closing bell, it was clear: India wasn’t immune to global jitters, but it wasn’t paralysed either.

2. The Forces That Drove the Day

Four crosscurrents shaped Wednesday’s tape, each pulling the market in different directions:

Crude’s collapse. Brent tumbled 3.59% to $74.31, WTI down 3.33% to $70.77. The catalyst? Easing tensions around the Strait of Hormuz blockade and a Bloomberg report suggesting Asian refiners are finding alternative supply from Russia, Africa, and Latin America. Lower crude is a structural tailwind for India—our import bill shrinks, inflation cools, and the rupee steadies. The currency barely moved (94.67, down 0.04%), but oil-sensitive sectors diverged: refiners like IOC and BPCL rallied, while upstream energy majors like ONGC and Oil India slipped.

Tech’s global rout. Nasdaq’s 2.21% fall overnight was the headline scare. Weak US growth data and profit warnings from semiconductor names spooked investors. Yet Indian IT, which had bled 28% over the past year per Livemint’s grim tally, caught a relief bid. Nifty IT jumped 2.05%—the best sectoral performance after realty. Oversold names like TCS, Infosys, and Tech Mahindra saw bottom-fishing. Volume was thin, suggesting this was short-covering rather than conviction buying, but it mattered for sentiment.

Banking’s revival. Private banks led the charge, up 1.85%, with Bank Nifty closing at 58,150 after touching 58,256 intraday. PSU banks lagged (+0.43%), reinforcing the bifurcation. HDFC Bank, ICICI Bank, and Axis Bank all closed above their 50-day moving averages on volume. FII selling, which JP Morgan pegged at $36 billion YTD, appears to be easing—May SIP inflows hit ₹310 billion, per the same note, providing a domestic cushion.

Market breadth. Advances marginally outnumbered declines in the Nifty 500, but the Midcap 100 barely moved (+0.10%). Nine stocks from the BSE MidCap 150 hit 52-week highs, including GE Vernova, per Economic Times—a sign that selective strength remains even as the broader market consolidates. The headline indices masked internal churn: realty, IT, and private banks lifted the Nifty; metals, autos, and energy dragged.

3. A Walk Through the Sectors

The leaders:

-

Realty (+2.17%): The sector’s best day in weeks. Oberoi Realty, DLF, and Godrej Properties all rallied on news that mortgage rates may ease if crude-driven inflation cools. Embassy REIT and Brookfield REIT also found buyers—institutional flows into yield plays are picking up as equity volatility persists.

-

IT (+2.05%): After a year-long bloodbath, tech caught a bid. TCS closed with RSI at 31 (oversold), Infosys near its 52-week low. Experts quoted in Livemint suggest 3-5 year SIP investors may find value here, but short-term traders remain cautious. Mid-tier IT—Persistent, KPIT, Tata Elxsi—saw volume spikes, suggesting some speculative interest is returning.

-

Private Banks (+1.85%): HDFC Bank, ICICI, Kotak, Axis all rallied 1.5-2.5%. Sandip Sabharwal, quoted in TOI, called private banks “strong” and a preferred pocket over frothy defence names. Technical picture confirms: most majors are above 50-DMA with RSI in the 55-65 range—healthy momentum without overbought extremes.

-

Banking (+1.69%): Broader bank index mirrored private peers. Canara Bank, Union Bank, and SBI from the PSU camp gained modestly (+0.5-0.8%), but the energy remained with private names.

The laggards:

-

Defence (-1.97%): A brutal reversal. Bharat Electronics fell 2.1%, Mazagon Dock 2.8%, HAL 3.2%. Sabharwal’s warning about “obnoxious” valuations in small-cap defence stocks resonated—many had run 50-100% in six months. Profit-booking was overdue. Volume was 2-3x average on several names, indicating institutional exit rather than retail panic.

-

Energy (-0.89%): ONGC, Oil India, and upstream producers bore the brunt of crude’s collapse. Refining and marketing companies (IOC, BPCL, HPCL) bucked the trend with modest gains, creating an unusual intra-sector split.

-

Auto (-0.42%): Tata Motors slipped 0.6% despite announcing ambitious targets (20% PV share by FY31, 40% CV share by FY28, per Livemint). M&M, Bajaj Auto, and Maruti all traded flat to negative. Volume was thin—no clear catalyst.

-

Metal (-0.40%): Tata Steel, JSW Steel, and Vedanta all declined 0.5-1.2%. China’s demand outlook remains cloudy, and domestic steel prices are under pressure. Vedanta, which has been volatile on news of its CopperTech Metals unit targeting a $3.6 billion US IPO valuation, saw 1.8x volume but closed 0.9% lower.

The steady middle:

- Oil & Gas (+0.63%): Bifurcated. Refiners up, producers down, net result slightly positive.

- PSU Banks (+0.43%): Tepid gains. SBI rose 0.5%, but smaller names like Indian Bank and Bank of Maharashtra were flat.

- Media (+0.32%): Zee Entertainment, PVR INOX, Sun TV—all traded in tight ranges. No fresh catalysts.

- Pharma (+0.12%): Near-flat. Lupin, Aurobindo, and Sun Pharma all closed within 0.5% of prior session. Sandip Sabharwal called pharma “good buys” in TOI, but momentum is absent. RSI readings in the 45-50 range—neutral.

- FMCG (+0.05%): ITC, Hindustan Unilever, Nestlé—barely moved. Monsoon concerns cited by Sambad.in (weak rainfall, rural demand worries) are keeping buyers cautious.

Thematic laggards:

- Commodities (-0.13%), Manufacturing (-0.44%), PSE (-0.48%), MNC (-0.72%): All red. The PSE (public sector enterprises) index’s decline reflects pain in ONGC, Coal India, NTPC. Manufacturing’s weakness ties to metals and autos. MNC index’s fall suggests multinationals underperformed local peers.

4. Beyond the Nifty 50 — Stories From the Broader Market

Wednesday’s real action was in the mid-cap trenches, where volatility and opportunity collide. Here’s what moved:

-

GE Vernova: Hit a 52-week high, part of the nine-stock cohort cited by Economic Times. The US industrial’s India-listed arm has rallied 25% in a month on grid infrastructure tailwinds. Volume was 2.1x average—institutions are accumulating.

-

Vedanta: The copper-to-aluminium conglomerate closed 0.9% lower despite news that its CopperTech Metals unit is eyeing a $3.6 billion US IPO valuation (TOI). The stock saw 1.8x volume, with intraday swings of ±2%. Traders are torn: IPO proceeds could deleverage the parent, but the move dilutes Vedanta’s crown jewel.

-

Adani Green: Rallied 1.6% on 1.4x volume. News broke that Donald Trump Jr. reportedly met Gautam Adani in Ahmedabad late last year (Forbes), weeks after US DOJ charges against Adani were dropped. Political optics aside, the stock’s technical picture shows a golden cross forming—50-DMA crossing above 200-DMA. RSI at 62.

-

Suzlon Energy: The wind turbine maker jumped 3.8% on 2.5x volume, closing near its 52-week high. Renewable energy names are benefiting from crude’s fall (less fossil fuel subsidy pressure) and government capex commitments. RSI at 74—overbought, but momentum is strong.

-

Defence names—selective pain: HAL (-3.2%), Mazagon Dock (-2.8%), BEL (-2.1%) all saw heavy selling on 2-3x volume. The defence index’s 1.97% fall was the day’s worst sectoral performance. Sabharwal’s “obnoxious valuations” comment (TOI) accelerated profit-booking. However, Bharat Electronics held up better than peers—its order book and balance sheet provide a floor.

-

REITs—Embassy & Brookfield: Both gained 1.2-1.5% on modest volume. Institutional interest is rising as equity volatility pushes yield-seekers toward 6-7% rental-backed returns. These aren’t exciting trades, but they’re defensive ones.

-

Tata Capital: The NBFC slipped 3% after a 17% rally over the past week took it to an all-time high (TOI). Classic profit-booking. Volume was 2.6x average. SBI Securities reportedly recommends “subscribe” to investors, but the stock needs to digest gains.

-

Advit Jewels IPO: The Jaipur-based jeweller’s ₹165 crore IPO opened with 2.3x subscription on Day 1 (TOI). Grey market premium at 47% suggests listing pop expectations are sky-high. Retail investors piled in, but institutional portion was undersubscribed—a red flag. This one’s speculative.

-

Semis & mid-tier IT: Moschip, KPIT, Persistent all saw 1.5-2x volume spikes with gains of 2-4%. These are beneficiaries of IT’s oversold bounce, but liquidity is thin. Traders only.

5. The Technical Picture

Wednesday’s charts tell a story of selective recovery, not broad euphoria. Here’s the damage report and opportunity set:

Oversold names catching a bid:

- TCS: RSI 31, below 50-DMA by 1.8%, volume 1.4x. Oversold technically, but no golden cross yet. Hold for long-term SIP investors, wait-and-watch for traders.

- Infosys: RSI 29, near 52-week low. Similar to TCS. Bottom-fishing is tempting, but no trend reversal confirmed.

- Lupin, Aurobindo: Both in the RSI 28-32 range. Pharma’s consolidation may be nearing an end, but volume hasn’t confirmed buying interest.

Overbought names at risk:

- Suzlon: RSI 74, 12% above 50-DMA, volume 2.5x. Momentum is strong, but a pullback to 50-DMA (₹68-70 range) would be healthy.

- Adani Green: RSI 62, golden cross signal forming today (50-DMA crossed 200-DMA). This is a technical buy signal, but the stock is politically sensitive—trade with tight stops.

- HDFC Bank: RSI 64, above 50-DMA, volume 1.3x. Healthy uptrend, room to run toward 200-DMA resistance.

Volume spikes flagging activity:

- Tata Capital: 2.6x volume on a 3% decline—distribution. Avoid until consolidation completes.

- HAL, BEL, Mazagon Dock: 2-3x volume on 2-3% declines—defence selling is institutional, not retail. These aren’t panics; they’re repositions.

- GE Vernova: 2.1x volume on 52-week high—accumulation. Technically attractive for momentum players.

Death cross warnings:

- No death crosses flagged today, but Coal India and NTPC are approaching that threshold. If their 50-DMAs cross below 200-DMAs in the next week, expect accelerated selling in PSE names.

Key Nifty technicals:

- Support: 23,789 (today’s low), then 23,600 (previous swing low).

- Resistance: 24,090 (today’s high), then 24,350 (May highs).

- 50-DMA: 23,680 (Nifty is now 1.4% above it—mild positive).

- 200-DMA: 24,200 (Nifty is 0.7% below it—resistance overhead).

6. AI Signals — BUY / HOLD / SELL

| Stock | Signal | Reason |

|---|---|---|

| Adani Green | BUY | Golden Cross today (50-DMA crossed 200-DMA), RSI 62, volume 1.4x avg, above both DMAs |

| HDFC Bank | BUY | Above 50-DMA, RSI 64, volume 1.3x, strong uptrend in private banks |

| GE Vernova | BUY | 52-week high, volume 2.1x, RSI 68, manufacturing tailwinds intact |

| Suzlon | HOLD | RSI 74 (overbought), 12% above 50-DMA, momentum strong but pullback likely |

| TCS | HOLD | RSI 31 (oversold), below 50-DMA, bounce today but no trend reversal yet |

| Infosys | HOLD | RSI 29, near 52w low, volume weak, wait for 50-DMA reclaim before buying |

| Tata Capital | SELL | Volume 2.6x on 3% decline after 17% rally, distribution signal clear |

| HAL | SELL | Death cross risk, RSI 42, volume 2.8x on 3.2% decline, defence sector under pressure |

| Mazagon Dock | SELL | Volume 3.1x on 2.8% fall, RSI 39, defence valuations correcting sharply |

| Vedanta | HOLD | Volume 1.8x but closed lower, IPO news creates uncertainty, technical picture mixed |

| Lupin | HOLD | RSI 28 (oversold), but volume weak, pharma sector flat, wait for confirmation |

| Bharat Electronics | HOLD | RSI 45, defence selling but BEL held better than peers, watch for 50-DMA support |

7. Tomorrow’s Setup — Global Cues & Calendar

Thursday’s open will hinge on how traders digest Wednesday night’s global tape—and it’s not pretty. Here’s the playbook:

US overnight:

– Dow -0.09% (51,666): Flat, no drama.

– S&P 500 -1.44% (7,365): Growth stocks sold off.

– Nasdaq -2.21% (25,587): Tech rout deepened. If this continues, expect pressure on Indian IT names to resume.

Asian cues:

– Nikkei -0.88% (69,175): Japan’s export-heavy index followed Nasdaq lower.

– Hang Seng +0.33% (23,412): Modest bounce; China property stimulus rumours kept buyers interested.

– ASX +0.24% (8,808): Australia held steady on commodity price stabilisation.

Commodities:

– Brent crude $74.31 (-3.59%), WTI $70.77 (-3.33%): If crude stabilises here, it’s a net positive for India. Watch for further declines—sub-$70 Brent could trigger another leg of rupee strength.

– Gold $3,989 (-3.41%): Sharp fall. Safe-haven selling suggests risk appetite is not collapsing—this is rotation, not panic.

Currency:

– USD/INR 94.67 (-0.04%): Stable. Rupee has held the 94.50-95.00 range for two weeks. No intervention signals.

GIFT Nifty signal:

– 24,021 (+0.83%): Matches Wednesday’s cash close, suggesting a flat-to-marginally-positive open around 24,000-24,050.

Key levels for Thursday:

– Nifty: Support at 23,900 (psychological), resistance at 24,100 (intraday). A break above 24,100 opens 24,200 (200-DMA).

– Bank Nifty: Support at 57,800, resistance at 58,300. Holding 58,000 is crucial for bulls.

– Sensex: Support at 76,000, resistance at 76,600.

What to watch:

– IT sector reaction to Nasdaq’s 2.21% fall. If TCS and Infosys gap down, the oversold bounce may be over.

– Defence stocks: are they done correcting, or is there more pain? Watch BEL’s 50-DMA test.

– Crude: another 2-3% fall would be rocket fuel for OMCs and aviation stocks.

– FII flows: if selling resumes, midcaps will feel it first.

8. The Honest Take

For long-term investors: Wednesday was a reminder that India’s structural story—SIP flows, domestic liquidity, lower crude—matters more than one night’s Nasdaq wobble. If you’ve been waiting to add IT names, the 28% YTD decline (per Livemint) is creating value, but don’t catch a falling knife. Stagger your buys. Private banks look technically solid, and realty’s 2.17% pop suggests rate-cut hopes are building. Defence, on the other hand, needs time—Sabharwal’s “obnoxious” call is harsh but fair for the frothier names. Pharma’s flat action is frustrating, but the sector’s defensive qualities shine when volatility spikes. Build positions in quality, not momentum.

For active traders: This was a relief rally in oversold pockets, not a trend reversal. Volume was decent but not spectacular. The Nifty’s 197-point gain looked impressive, but breadth was mediocre—Midcap 100 barely moved. Trade the setups, not the headlines: Adani Green’s golden cross is textbook bullish; Suzlon’s RSI 74 is textbook overbought. Defence names saw genuine distribution—if you’re long, trail stops tight. Tomorrow’s open will be dictated by US tech’s overnight move. If Nasdaq stabilises, we consolidate; if it falls another 1-2%, expect gap-down pressure. Keep 50% cash, book profits into strength, and wait for cleaner technical confirmations before deploying fresh capital.

“The stock market is a device for transferring money from the impatient to the patient.” — Warren Buffett

Disclaimer: This blog is for informational and educational purposes only. It is not investment advice. All figures cited reflect publicly reported data for the trading session indicated. Markets are subject to risk; please consult a SEBI-registered advisor before acting on any view expressed here.