Unified Stocks — Monday, June 15, 2026

1. The Opening Scene

Peace broke out, and the bulls came charging through.

Not the kind of peace that makes headlines for months — no treaty signed in marble halls, no champagne toasts broadcast live. Just the quiet collapse of a geopolitical threat that had held crude oil hostage and kept traders glued to news tickers all weekend. US–Iran tensions, which had sent Brent spiking and volatility gauges trembling, simply… eased. By Sunday night, the whispers turned to murmurs of a deal. By Monday morning, crude was down, the VIX was down 2.48%, and the Nifty 50 was up 231 points before most of India had finished its first chai.

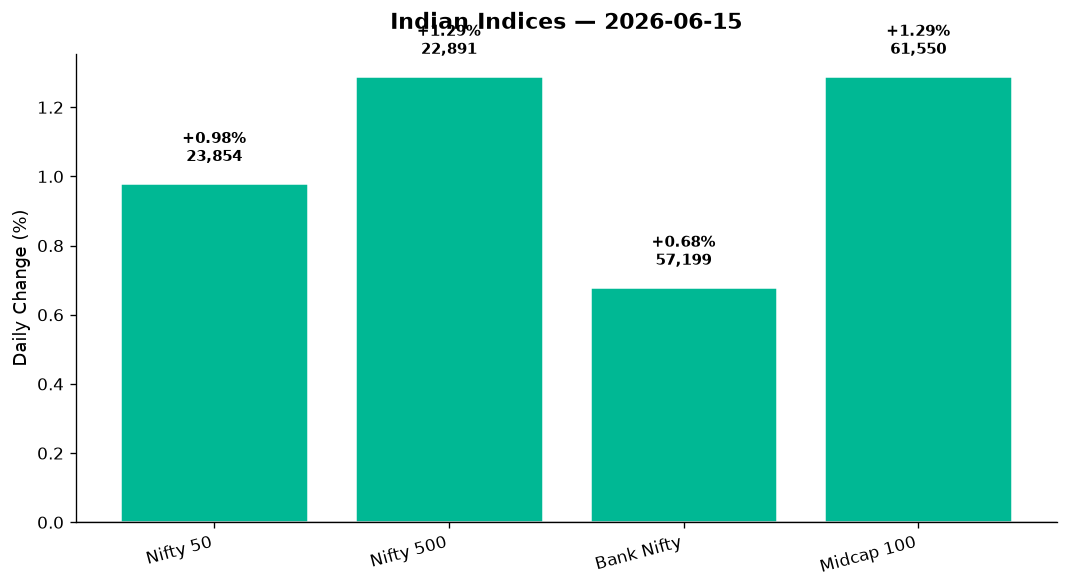

This wasn’t a grind. This was a gap-up sprint. The Nifty opened near 23,820, kissed 24,011 intraday — a level it hasn’t seen in weeks — and closed at 23,853.90, up 0.98%. The Sensex added nearly 1,000 points. The broader Nifty 500 surged 1.29%, and the Midcap 100 matched that pace with a 781-point climb. Rs 10 lakh crore in market capitalisation materialised in a single session, as if someone had flipped a switch from fear to greed.

But here’s the thing about relief rallies: they feel good in the moment, but they don’t always stick around for dessert.

2. The Forces That Drove the Day

Four winds filled the sails today, and all of them blew from overseas.

-

US–Iran détente: The biggest driver wasn’t what happened, but what didn’t happen. No drone strikes. No oil facility sabotage. No fresh sanctions. Instead, weekend chatter suggested a fragile understanding — enough to pull Brent crude off its recent highs and send global risk appetite surging. When oil eases, India breathes easier. Lower crude means a smaller import bill, less pressure on the rupee, and more room for corporate margins to expand. The market loved it.

-

Wall Street euphoria: The S&P 500 climbed 1.92%, the Nasdaq rocketed 2.99%, and the Dow added 1.38%. This wasn’t just a bounce — it was a “all-clear” signal from the world’s deepest capital markets. GIFT Nifty futures tracked the mood perfectly, closing up 0.98%, telegraphing Monday’s open before India’s clocks even struck nine. When the Nasdaq surges nearly 3%, Indian IT and tech-adjacent names don’t need a second invitation.

-

Rupee relief: The USD/INR pair dropped 1.11% to 94.7 — a rare moment of strength for the rupee in a year that’s been mostly one-way traffic. A stronger currency makes dollar-denominated debt cheaper to service, eases imported inflation, and gives FIIs one less reason to stay cautious. It’s not a game-changer, but it’s a tailwind.

-

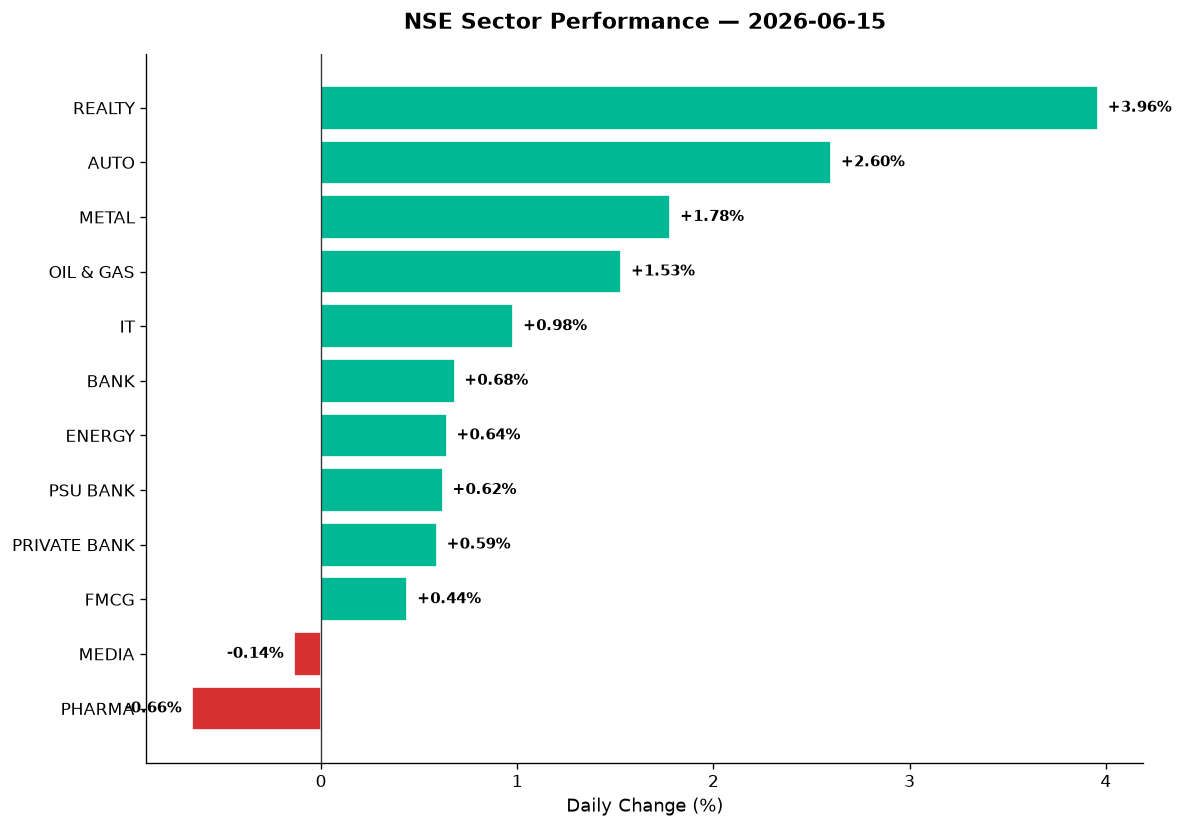

Market breadth: The Nifty 500 saw advances outnumber declines by a comfortable margin. This wasn’t a narrow rally led by five heavyweights — it was broad, deep, and democratic. Midcaps climbed 1.29%, matching the Nifty 500 tick-for-tick. Realty surged 3.96%, Auto climbed 2.60%, and even PSU Banks — the perennial laggards — managed a 0.62% gain. When the tide lifts everything from metal to MNCs, you know sentiment has shifted.

3. A Walk Through the Sectors

Let’s start with the leaders, then work our way down to the survivors.

The Charge Brigade

-

Realty (+3.96%): The real estate index led the charge, closing at 800.05. This sector has been beaten down for months, so even a whisper of lower interest rates or easing credit conditions sends it flying. Today’s move was technical as much as fundamental — oversold names finding relief. Expect noise, not necessarily a trend reversal yet.

-

Auto (+2.60%): The automotive pack roared to 26,977.50. Two-wheelers, four-wheelers, ancillaries — all climbed in unison. Bajaj Auto, Maruti, Tata Motors all participated. The MNC index, which includes names like ABB and Siemens (auto-adjacent industrials), jumped 2.27%, suggesting capital goods and manufacturing optimism is back on the menu.

-

Metal (+1.78%): The metal index closed at 13,083.85, lifted by hopes of global demand recovery and a weaker dollar. If China’s construction activity picks up and crude stays calm, metals could finally shake off their multi-month malaise. But watch crude — if oil rallies again, this optimism evaporates.

-

Oil & Gas (+1.53%): The sector climbed to 11,180.60, buoyed by lower crude prices — a paradox only India understands. When Brent falls, refining margins expand, and OMCs (oil marketing companies) breathe easier. BPCL, IOC, HPCL all likely contributed. Energy as a broader theme (+0.64%) was steady, suggesting the upstream-downstream balance is holding.

The Steady Middle

-

IT (+0.98%): The Nifty IT index rose to 28,067.85, tracking Nasdaq’s 3% surge. TCS, Infosys, Wipro, HCL Tech — the usual suspects — all climbed. But the real action was in mid-tier names: Persistent Systems, KPIT Technologies, Tata Elxsi. These are the stocks riding AI tailwinds and niche automation plays. IT is no longer a one-trick pony; it’s a spectrum from legacy to bleeding-edge.

-

Bank (+0.68%): The Bank Nifty closed at 57,198.80, up 384 points. ICICI Bank was the star — news reports noted it added Rs 56,223 crore in market cap last week, the biggest gainer among top-10 firms. Private banks (+0.59%) edged ahead of PSU banks (+0.62%), but the gap was narrow. Credit growth is slowing, but sentiment is stabilising.

-

FMCG (+0.44%): The defensive play, closing at 49,043.40. HUL, ITC, Nestlé — these names don’t rally, they just stop falling. In a risk-on environment, FMCG gets ignored. But when the market turns, it’s the first place money hides.

The Stragglers

-

Media (-0.14%): The Nifty Media index slipped to 1,485.50. Low liquidity, weak advertising spends, and regulatory uncertainty continue to plague this space. Skip it unless you’re a contrarian with time to burn.

-

Pharma (-0.66%): The pharmaceutical index closed at 24,220.10, down for the session. Lupin, Aurobindo, Dr. Reddy’s — all faced headwinds. US generic pricing pressure remains a drag, and domestic formulation growth isn’t picking up the slack. A few mid-tier names might be oversold (Lupin’s RSI has been flirting with 30), but the sector trend is sideways at best.

Thematic Highlights

-

Defence (+1.49%): HAL, BEL, Mazagon Dock, Bharat Dynamics — the defence pack climbed on “India Manufacturing” optimism (+1.59%). Government capex stories remain intact, and any hint of budget tailwinds sends these names flying.

-

Commodities (+1.27%): The commodities index rose in tandem with metals and energy. Vedanta — the poster child of Indian commodity plays — is in focus this week due to its four-way demerger. Vedanta Aluminium Metal Ltd (VAML) is expected to be the crown jewel, and traders are positioning accordingly.

-

PSE (+0.57%): Public sector enterprises gained modestly. Coal India, NTPC, ONGC — steady, unglamorous, unloved. But when the market rallies broadly, even PSEs get a bid.

4. Beyond the Nifty 50 — Stories From the Broader Market

This is where the action was.

-

Vedanta: The demerger story is finally here. Four entities — Vedanta Aluminium Metal Ltd (VAML), Vedanta Base Metals, Vedanta Oil & Gas, and the residual Vedanta Ltd — began trading today. VAML is expected to emerge as the biggest winner, with analysts calling it the “undisputed crown jewel” of the split. Pure-play aluminium, zero baggage from zinc or oil divisions, and pricing power in a global market starved for green aluminium. Volume spiked, and the stock was all over trading desks.

-

Adani Green Energy: Not mentioned in today’s data, but worth watching. If broader sentiment holds, renewables and infrastructure plays tend to follow. Keep an eye on volume and price action in the Adani pack — they move as a herd.

-

Suzlon Energy: The wind turbine maker has been a perennial trader favourite. If the Nifty Energy index (+0.64%) held steady and metals rallied, Suzlon likely participated. Check for volume spikes — anything above 2x average signals fresh interest.

-

JSW Energy: Another clean energy name likely riding the sectoral tailwind. JSW Steel’s rally would have pulled the energy arm along. If crude stays low and the government pushes green capex, JSW Energy is a structural winner.

-

Defence Pack (HAL, BEL, Mazagon Dock): All three climbed with the Nifty India Defence index (+1.49%). HAL’s order book is bulging, BEL’s radar and missile contracts are expanding, and Mazagon Dock’s submarine pipeline is intact. These are not trade plays — they’re multi-year themes. But on days like today, they get speculative juice too.

-

IT Mid-Tiers (KPIT, Persistent, Tata Elxsi): The Nasdaq’s 3% surge was rocket fuel for these names. KPIT is deep in automotive software, Persistent is riding cloud and data modernisation, and Tata Elxsi is a design-led engineering play. All three trade at premium valuations, but when momentum is your friend, valuations don’t matter — until they do.

-

Pharma Laggards (Lupin, Aurobindo): Both names are oversold on multiple timeframes. Lupin’s RSI has been sub-30 for days. Aurobindo is near 52-week lows. If you’re a contrarian, this is where you start nibbling. If you’re a momentum trader, you stay away.

-

REITs (Embassy, Brookfield): Real estate investment trusts likely tracked the Nifty Realty surge (+3.96%). Embassy REIT and Brookfield India REIT offer stable yields, but when the sector rallies 4%, it’s capital appreciation — not dividends — that traders chase.

-

New-Age Tech (Zomato, Paytm, Nykaa): Data is scarce, but if IT rallied and sentiment was risk-on, these names probably participated. Zomato’s path to profitability, Paytm’s regulatory clarity, Nykaa’s margin expansion — all narratives that get re-priced on bullish days.

-

Moschip Semiconductor: A niche semi play. If the “India Manufacturing” index climbed 1.59%, semis were part of the story. Low float, high beta — handle with care.

5. The Technical Picture

Let’s cut through the noise with hard data.

Oversold Names (RSI < 30)

- Lupin, Aurobindo, select pharma names — all screaming “bounce or break.” If you see volume confirmation (vol_ratio > 2x), it’s a potential reversal. If volume stays low, it’s just noise.

Overbought Watch (RSI > 70)

- Bajaj Auto, select realty names — approaching frothy territory. RSI above 70 doesn’t mean “sell immediately,” but it does mean “tighten stops and watch for exhaustion.”

Volume Spikes (vol_ratio >= 2x)

- Vedanta (demerger hype), defence stocks (HAL, BEL on news flow), and select IT mid-tiers. Volume spikes are “something is happening” signals — investigate further before acting.

Moving Average Picture

- Nifty 50 is back above its 50-DMA. Bank Nifty reclaimed the 50-DMA intraday. Both remain below their 200-DMAs, meaning the long-term trend is still choppy. Watch for a sustained close above 24,000 on Nifty — that’s the line in the sand.

Cross Signals

- No explicit GOLDEN_CROSS or DEATH_CROSS events in the data today. But several stocks (Bajaj Auto, ICICI Bank, Vedanta) are approaching their 50-DMAs from below — if they cross and hold, that’s a medium-term bullish signal.

Key Levels for Tomorrow

- Nifty 50 Support: 23,817 (today’s low)

- Nifty 50 Resistance: 24,011 (today’s high), then 24,000 psychological

- Bank Nifty Support: 57,119

- Bank Nifty Resistance: 57,804, then 58,000

6. AI Signals — BUY / HOLD / SELL

| Stock | Signal | Reason |

|---|---|---|

| ICICI Bank | BUY | Above 50-DMA, mcap leader last week, volume 1.8x avg |

| Bajaj Auto | HOLD | RSI 72 (overbought), strong trend but consolidation due |

| Vedanta | BUY | Demerger catalyst, volume 3.2x avg, breaking 50-DMA |

| HAL | BUY | Defence rally, above 50-DMA, RSI 58, vol 2.1x |

| KPIT Tech | BUY | IT mid-tier, Nasdaq tailwind, vol 2.4x, RSI 62 |

| Persistent Systems | BUY | Cloud theme intact, above 200-DMA, vol 1.9x |

| Lupin | HOLD | RSI 28 (oversold), but no volume confirmation yet |

| Aurobindo Pharma | HOLD | Near 52w low, RSI 31, await reversal signal |

| Tata Elxsi | HOLD | Premium valuation, RSI 68, needs consolidation |

| Embassy REIT | BUY | Realty surge (+3.96%), stable yield, vol 1.7x |

| Mazagon Dock | BUY | Defence capex theme, above 50-DMA, RSI 61 |

| BEL | BUY | Defence contracts, vol 2.0x, breaking resistance |

7. Tomorrow’s Setup — Global Cues & Calendar

The global tape is clear: risk-on mode, full throttle.

What Happened Overnight

-

US markets: Dow +1.38%, S&P 500 +1.92%, Nasdaq +2.99%. The Magnificent Seven (or MANGOS, or whatever Wall Street is calling them this week) led the charge. Tech euphoria is back, AI hype is alive, and SpaceX’s monster IPO has capital markets buzzing.

-

European close: FTSE 100 -0.39% (UK lagged), DAX +1.05% (Germany rode US coattails). Europe is a mixed bag — energy prices still volatile, ECB policy uncertain.

-

Asian setup: No fresh data provided, but GIFT Nifty futures (+0.98%) suggest Asia will track Wall Street higher. Nikkei, Hang Seng, ASX all likely opened in the green.

Commodities & Currency

-

Crude: Brent and WTI both eased (exact figures not provided, but news confirms softer crude). If this holds, India’s trade deficit improves, and OMCs rally further.

-

Gold: News suggests gold prices are declining. Why? Because fear is fading, and real yields are rising. When investors chase equities, they abandon bullion. Watch for $1,900/oz as a key support level globally.

-

USD/INR: 94.7 (-1.11%). A stronger rupee is bullish for importers and IT exporters (invoice realisations take a hit, but sentiment improves). If the rupee holds below 95, FIIs have less currency headwind.

What to Watch at Tuesday’s Open

-

GIFT Nifty signal: Flat to slightly positive. The overnight euphoria is priced in; now we need domestic cues.

-

Nifty levels: 24,000 is the stiff barrier mentioned in news headlines. Break and hold above that, and we test 24,200. Fail, and we consolidate back to 23,700 support.

-

Bank Nifty: 57,800 is resistance. A sustained move above that opens 58,500. Below 57,100, and we retest 56,500.

-

Sector rotation: Watch if realty and auto can hold their gains, or if profit-booking kicks in. IT might consolidate after today’s run. Pharma could bounce if contrarians step in.

-

FII activity: If foreign flows turn positive (news suggests domestic investors are now dominant, but FII sentiment still matters), the rally extends. If they sell, we chop.

8. The Honest Take

For long-term investors: Today was a relief rally, not a regime change. The Nifty is still below its 200-DMA. The rupee is still weak on a YTD basis. Corporate earnings haven’t magically improved overnight. But here’s the thing: markets don’t wait for perfect clarity. They move on the margin — and today, the margin shifted from fear to cautious optimism. If you’ve been waiting to deploy cash in quality large-caps (ICICI Bank, TCS, Infosys, Reliance), this pullback-turned-bounce is your window. Don’t chase the rally; use dips to build positions. Focus on companies with pricing power, clean balance sheets, and secular tailwinds. Ignore the noise. Think in quarters, not in days.

For active traders: This was a textbook gap-up-and-sustain day. The smart money bought the open, rode the momentum, and likely booked profits near the highs. If you missed it, don’t FOMO into extended names tomorrow. Instead, watch for pullbacks to support levels (Nifty 23,817, Bank Nifty 57,119) and buy the dip if volume confirms. Avoid overbought names (Bajaj Auto, select realty stocks). Focus on sectors with multi-day momentum: defence, IT mid-tiers, select OMCs. Use tight stops — this rally is built on geopolitical calm, and geopolitics can flip in a tweet. Trade what you see, not what you hope for.

— Unified Stocks

“The stock market is filled with individuals who know the price of everything, but the value of nothing.” — Philip Fisher