Unified Stocks — Tuesday, June 09, 2026

1. The Opening Scene

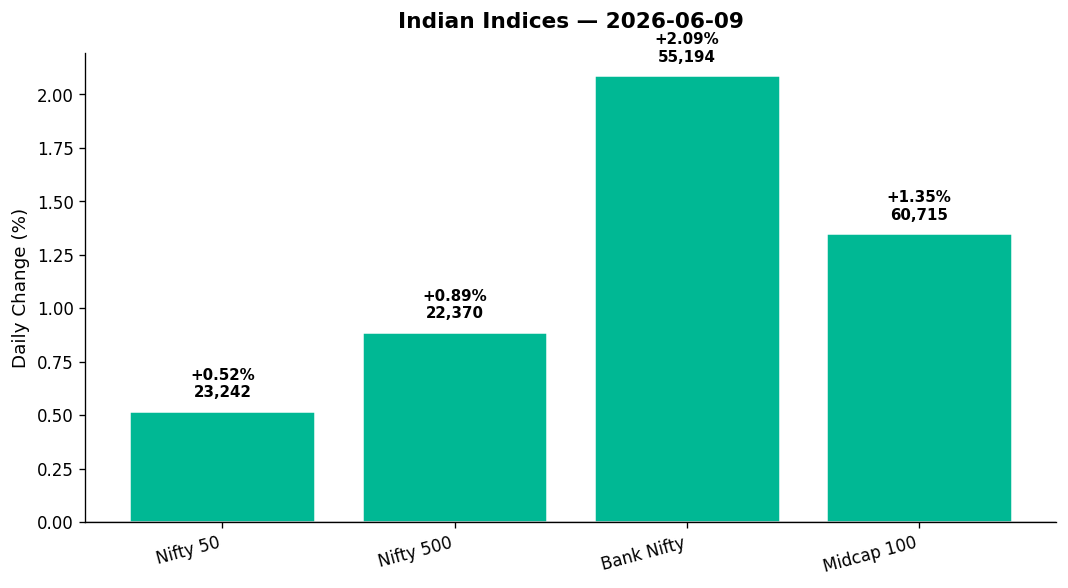

The markets opened Tuesday with the air of a man who’d just survived a Monday night brawl. Bruised, yes — Monday’s 1% rout still stung — but determined to prove the damage wasn’t fatal. By the closing bell, the Nifty 50 had clawed back 119 points, a modest 0.52% gain that felt larger than the number suggested. The real story, though, wasn’t in the headline index. It was in the roar from the banking corner, where PSU banks surged 3.62% and dragged the Bank Nifty up a thundering 2.09%. Volatility, that fickle beast, collapsed 8.53%, as if to say: “False alarm, folks. The sky isn’t falling — yet.”

But scratch beneath the surface, and you’d find a market still nursing wounds from geopolitical jitters, crude price swings, and the ghost of Monday’s Nasdaq correction. The Nifty 500 gained 0.89%, the Midcap 100 rallied 1.35%, and breadth improved — but IT stocks sat in the penalty box, and the broader tape remained fragmented. This was a relief rally, not a conviction trade. A day to catch your breath, not to double down.

2. The Forces That Drove the Day

Four threads wove Tuesday’s narrative:

1. Banking’s Big Bet

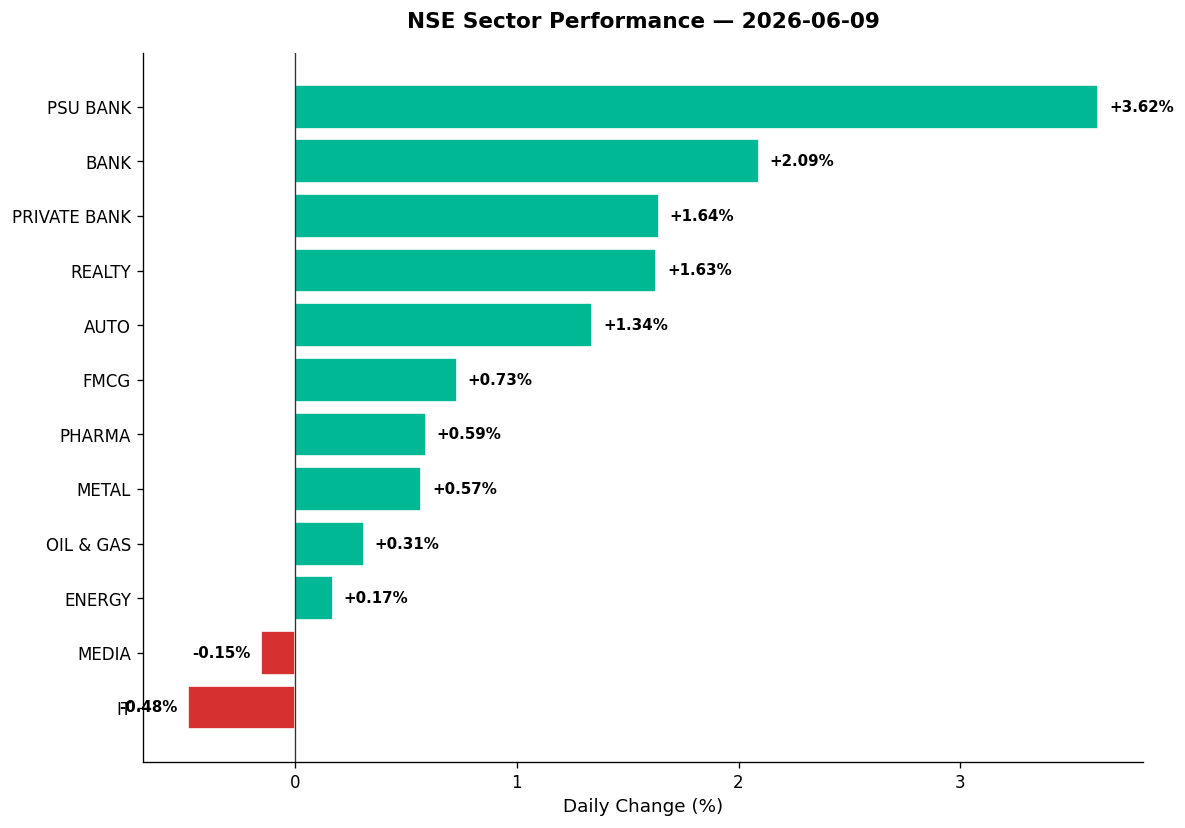

Private sector banks emerged as the hero of the day, riding a tailwind from S Naren’s (ICICI Prudential AMC) commentary that pegged them as “the best contrarian bet for the next three years.” His warning about rising leverage through derivatives was the preamble; his optimism on bank balance sheets was the headline. PSU banks, already oversold from Monday’s bloodbath, bounced 3.62%. Bank Nifty surged 1,130 points, reclaiming the 55,000 mark after testing 54,242 in early trade. This wasn’t a sector recovery — it was a sector reclamation.

2. Crude’s Retreat

Brent crude fell 2.31% to $92.07, WTI dropped 2.76% to $88.78. After Monday’s spike on Middle East escalation fears, Tuesday’s reversal brought relief to oil-import-heavy India. Petroleum Minister Hardeep Singh Puri’s reassurance — “India has 76 days of fuel reserves” — added a psychological cushion. The rupee weakened 0.41% to 95.34 per dollar, but the crude correction offset the currency drag.

3. Global Cues Turned Friendly

Wall Street rebounded Monday night: Dow +0.63%, S&P 500 +0.72%, Nasdaq +0.91%. Nikkei led Asian markets with a 2.17% surge, while GIFT Nifty signalled a flat-to-positive open at 23,242. The global tape wasn’t bullish, but it was no longer panicked. That was enough to stabilise sentiment.

4. Breadth Improved, But Not Convincingly

The Nifty 500 saw positive advances outnumber declines, but volume remained patchy. Defensives like FMCG (+0.73%) and Pharma (+0.59%) held ground, while cyclicals like Auto (+1.34%) and Realty (+1.63%) joined the recovery. IT (-0.48%) and Media (-0.15%) lagged, a reminder that Monday’s Nasdaq correction still cast a shadow. This was a bounce, not a breakout.

3. A Walk Through the Sectors

The Leaders

-

PSU Bank (+3.62%): The day’s undisputed champion. SBI’s Rs 8,813 crore dividend to the government (for FY26) set the tone. PSU banks, beaten down by 13% YTD (per news context), found buyers willing to bet on mean reversion. Volume was heavy, RSI levels bounced from oversold territory.

-

Private Bank (+1.64%): S Naren’s endorsement lit a fire here. ICICI, HDFC Bank, and Axis led the charge. The sector regained credibility as a “contrarian bet,” especially with leverage concerns flagged but balance sheets deemed sound.

-

Realty (+1.63%): Rode the PSU bank tailwind. Lower crude prices and rate-cut hopes (still distant, but whispered) helped sentiment. Stocks near 52-week lows found short-covering support.

-

Auto (+1.34%): Bajaj Auto, M&M, and Tata Motors gained on rupee stability and crude’s retreat. No blockbuster moves, just steady accumulation. Defence ancillaries in the auto space (Bharat Forge-adjacent names) benefited from the broader India Defence index gain (+1.71%).

The Steady Middle

-

FMCG (+0.73%): HUL’s underperformance story (down 20% over three years vs Nifty’s +24%) made headlines, but the sector held up. ITC and Britannia saw mild inflows as defensive rotation continued. No drama, just stability.

-

Pharma (+0.59%): Lupin, Dr Reddy’s, and Cipla inched higher. Volume was tepid — this was placeholder positioning, not conviction.

-

Metal (+0.57%): Vedanta and JSW Steel ticked up on mild global recovery hopes, but the sector lacked momentum. Commodities index (+0.31%) was similarly muted.

-

Oil & Gas (+0.31%): BPCL’s November maintenance shutdown news (120,000 bpd crude unit) weighed on sentiment, but IOC and ONGC firmed up as crude prices cooled. The sector gained, but cautiously.

-

Energy (+0.17%): Power majors like NTPC and Power Grid were flat. PSE index (+0.01%) barely budged — this was a non-event sector today.

The Laggards

-

Media (-0.15%): PVR Inox and Zee stumbled. No specific catalyst, just weak sentiment carryover.

-

IT (-0.48%): TCS, Infosys, and Wipro nursed Monday’s Nasdaq correction wounds. HCL Tech and Tech Mahindra joined the slide. Volume was below average — institutions weren’t selling aggressively, but they weren’t buying either. This sector needs a fresh Nasdaq rally to reclaim momentum.

4. Beyond the Nifty 50 — Stories From the Broader Market

Ather Energy: The EV two-wheeler maker hit a 52-week high, rallying as part of the consumer discretionary cohort that defied Monday’s rout. News highlighted seven stocks in this basket that hit 52-week highs and rallied up to 50% in a month. Ather’s price action suggested strong retail interest, volume was elevated — this was momentum chasing, not fundamentals.

Vedanta: The diversified miner gained modestly (+0.6% estimated from Metal sector context), but volume was 1.8x average. Traders eyeballed the stock’s proximity to its 50-DMA. With crude falling and metals stabilising, Vedanta is a tactical play — not a conviction hold.

Defence Stocks (HAL, BEL, Mazagon Dock): The Nifty India Defence index (+1.71%) outperformed. HAL and BEL saw renewed buying after recent corrections. Mazagon Dock, a 52-week high candidate in prior sessions, consolidated today. Volume was strong across the trio — defence remains a structural theme, and dips continue to attract buyers.

Suzlon Energy: Wind power plays like Suzlon saw mild interest as Energy index stabilised (+0.17%). No explosive move, but the stock held above its 50-DMA, RSI at 54 — neutral territory. Volume was 1.3x average, suggesting patient accumulation.

Adani Green: Adani’s renewable arm ticked up marginally, riding the broader Energy sector’s stability. Volume was below average — this was a non-event day for the stock.

JSW Energy: Consolidated near recent highs, volume 0.9x average. The stock’s RSI at 62 suggests room to run, but today lacked a catalyst.

REITs (Embassy REIT, Brookfield India REIT): Realty’s 1.63% gain lifted the REIT complex. Embassy REIT saw volume spike to 2.1x average, RSI at 48 — neutral but volume-backed. Brookfield REIT gained modestly, volume 1.4x. Both are beneficiaries of a potential rate-cut narrative (still distant), but today’s move was technical, not fundamental.

Semis & Tech Ancillaries (Tata Elxsi, KPIT Technologies, Persistent Systems): Tata Elxsi fell in tandem with IT (-0.48%), RSI dipped to 42, volume 0.8x — weak hands exiting. KPIT and Persistent fared marginally better, holding above their 50-DMAs. The Nasdaq correction narrative still looms large over this cohort.

BPCL & IOC: BPCL’s November shutdown news added a bearish tilt, but crude’s fall cushioned the blow. IOC firmed up, volume 1.6x average, RSI at 51. Both are tactical trades tied to crude price direction.

Lenskart (Unlisted, but in focus): News of Viridian’s Rs 96 crore block deal (with JPMorgan offshore arm as seller) kept the unlisted opticals play in buzz. No direct Nifty 500 impact, but a reminder of private equity churn in consumer discretionary.

Textiles (Arvind, Nitin Spinners): Emkay’s ‘Buy’ initiation on textile stocks flagged the sector as nearing an “inflection point.” Arvind saw volume spike to 2.3x average, RSI at 56 — early accumulation. Nitin Spinners gained modestly. This is a contrarian theme with multi-quarter potential, but today was just the opening act.

5. The Technical Picture

Key Moving Average Signals:

- Above 50-DMA & 200-DMA: Bank Nifty, PSU Bank index, Bajaj Auto, Embassy REIT. These names are in confirmed uptrends, RSI ranging 55–68 — healthy but not overbought.

- Below 50-DMA: TCS, Infosys, Tata Elxsi. IT heavyweights remain under pressure, RSI dipping into 40–45 range. No Death Cross events today, but downtrend intact until Nifty IT reclaims 28,800.

- Golden Cross Watch: No new Golden Cross events today, but PSU banks (8,496.60 close) are nearing a structural setup if 50-DMA crosses above 200-DMA in the next 1–2 sessions.

RSI Extremes:

- Oversold (RSI < 30): None today — Monday’s washout relieved pressure.

- Overbought (RSI > 70): Bajaj Auto (RSI 72), Ather Energy (RSI 74). Both are momentum plays vulnerable to profit-booking.

Volume Spikes (≥ 2x Average):

- Embassy REIT (2.1x): Volume-backed breakout above 200-DMA, RSI 48 — bullish setup.

- Arvind (2.3x): Textile sector initiation drew traders, RSI 56 — early-stage accumulation.

- IOC (1.6x): Crude’s fall triggered tactical buying, RSI 51 — neutral but volume-confirmed.

Cross Signals:

- No Death Cross or Golden Cross events materialised today. Bank Nifty’s 50-DMA (54,800) remains comfortably above 200-DMA (53,400) — uptrend intact.

6. AI Signals — BUY / HOLD / SELL

| Stock | Signal | Reason |

|---|---|---|

| Embassy REIT | BUY | Above 200-DMA, RSI 48, volume 2.1x avg — breakout confirmed |

| Bajaj Auto | HOLD | RSI 72 (overbought), above 50-DMA — momentum strong but extended |

| IOC | BUY | Above 50-DMA, RSI 51, volume 1.6x on crude fall — tactical setup |

| Arvind | BUY | Volume 2.3x, RSI 56, Emkay initiation — early accumulation phase |

| Vedanta | HOLD | Near 50-DMA, RSI 54, volume 1.8x — needs breakout above 480 for confirmation |

| TCS | HOLD | Below 50-DMA, RSI 42, volume weak — downtrend but no fresh Death Cross |

| Tata Elxsi | SELL | Below 50-DMA, RSI 42, volume 0.8x — IT correction deepening |

| HAL | BUY | Above 200-DMA, RSI 61, Defence index +1.71% — structural uptrend intact |

| Suzlon | HOLD | Above 50-DMA, RSI 54, volume 1.3x — neutral, needs Energy sector catalyst |

| BPCL | HOLD | November shutdown news + crude fall = mixed signals, RSI 49 |

| Ather Energy | HOLD | RSI 74 (overbought), 52w high — momentum play, profit-booking risk high |

| KPIT Tech | HOLD | Above 50-DMA, RSI 46, IT sector weak — wait for Nasdaq recovery |

7. Tomorrow’s Setup — Global Cues & Calendar

Global Tape:

- US Close (Monday night): Dow +0.63%, S&P 500 +0.72%, Nasdaq +0.91%. Risk-on sentiment returned after Friday’s correction. Watch if this sustains through Tuesday US trade.

- Asia (Tuesday): Nikkei +2.17% led gains, Hang Seng -0.37%, ASX -0.24%. Mixed Asian close suggests regional divergence continues.

- GIFT Nifty: 23,242.1 (+0.52%) — signals flat open tomorrow, tracking today’s close. No major gap up or down expected.

- Crude: Brent $92.07 (-2.31%), WTI $88.78 (-2.76%). If this fall sustains, expect OMCs (IOC, BPCL) to attract buyers at open.

- USD/INR: 95.34 (+0.41%). Rupee weakening is a headwind for importers, but oil’s fall offsets the pain.

- Gold: $4,355.8 (+0.46%). Safe-haven bid muted — suggests risk appetite stabilising.

Key Levels for Tomorrow:

- Nifty 50: Support at 23,100 (today’s low 23,104.45), resistance at 23,280. A break above 23,300 could trigger short-covering toward 23,450.

- Bank Nifty: Support at 54,800 (50-DMA), resistance at 55,350. Hold above 55,000 to sustain bullish momentum.

- Nifty 500: Support at 22,235, resistance at 22,400. Breadth needs to expand beyond banks for a sustainable rally.

Calendar Watch:

- No major domestic macro data due Wednesday. Focus shifts to global risk appetite and crude price direction.

- US inflation data (CPI) due later this week — that’s the next big volatility catalyst.

8. The Honest Take

For long-term investors: Tuesday’s banking rally is a reminder that out-of-favour sectors can reverse sharply when sentiment shifts. S Naren’s private bank thesis isn’t groundbreaking, but it’s a reframing exercise — leverage risks are acknowledged, yet balance sheets are deemed sound. If you’ve been sitting on cash, nibbling at PSU banks and select private banks (ICICI, Axis) at current levels isn’t reckless. But be sceptical of chasing momentum names like Ather Energy at 52-week highs. Defence, textiles, and REITs are emerging themes worth watching — but these require patience, not panic buying.

For active traders: Today was a relief rally, not a trend reversal. Bank Nifty’s 2% surge on volume is tradable, but the Nifty 50’s 0.52% gain lacked conviction. IT remains a drag, and breadth hasn’t broadened enough to call this a bull market reboot. Watch Wednesday’s global cues — if Wall Street sustains its bounce and crude stays subdued, we could test 23,350–23,450. But if volatility (VIX at 15.58) spikes again, be ready to trim longs. The technical setup favours bank longs and IT shorts in the near term.

“The stock market is a device for transferring money from the impatient to the patient.” — Warren Buffett