Unified Stocks — Monday, June 29, 2026

1. The Opening Scene

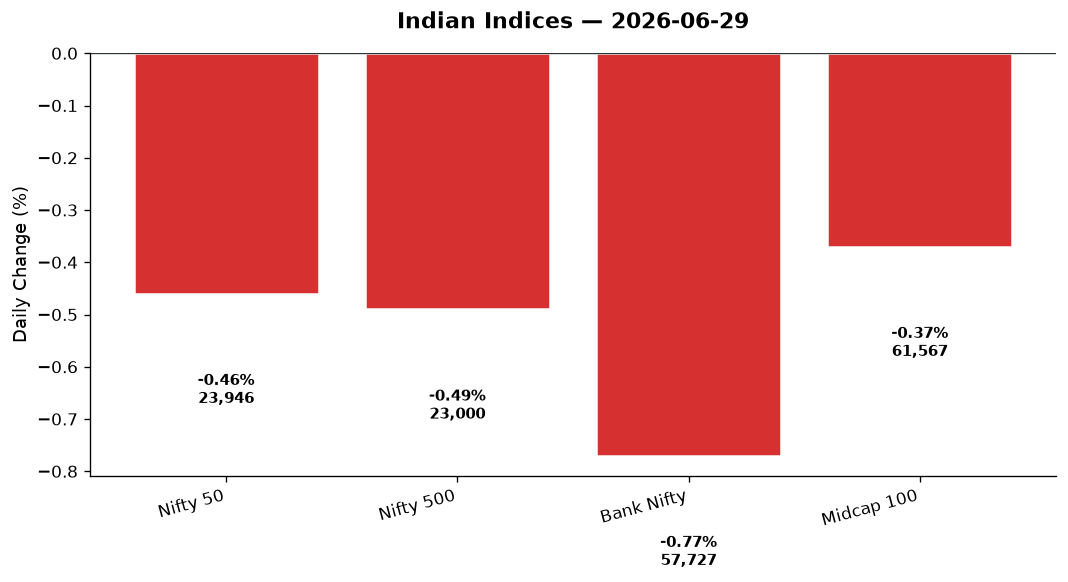

The rupee firmed. Crude stayed soft. Wall Street closed green, and Asia flickered hopeful. Yet when Mumbai’s bell rang this morning, the tape turned its back on optimism. By 3:30 p.m., the Nifty 50 had surrendered 109.75 points to settle at 23,946.25 — a 0.46% dip that felt larger than the number suggested. Bank Nifty bled harder, down 0.77%, dragging financials into the red despite last week’s rally in ICICI and HDFC Bank. The VIX stirred, climbing 4.29% to 13.61, a whisper of unease beneath the surface calm. This was not capitulation. This was indecision — the market caught between Friday’s fade and Monday’s fresh fears, testing whether the bulls still had conviction or whether last week’s gains were merely a ceasefire in a longer war.

2. The Forces That Drove the Day

Four threads wove today’s narrative, each pulling the market in conflicting directions:

-

Global tailwinds met domestic drift. US indices closed Friday strong — Nasdaq up 1.05%, S&P 500 +0.67%, Dow +0.78% — yet GIFT Nifty futures signalled caution ahead of India’s open. Asian markets leaned positive (Hang Seng +1.57%, Nikkei +0.15%), but India’s tape disconnected, caught in profit-booking after three consecutive weeks of gains.

-

Crude’s gift, but no celebration. Brent held near $73, WTI stable — a relief for importers. Last week’s cooling oil prices had fuelled optimism in auto and aviation names. Today, that momentum stalled. Oil & Gas (-1.18%) and Auto (-2.08%) both reversed sharply, suggesting traders doubted whether the crude rally’s end was sustainable.

-

FII flows remain the wildcard. News wires reported FII buying returning to India as the rupee firmed to 94.53 (up 0.14% vs the dollar) and South Korea’s Kospi crashed 8%, freezing trading. Yet today’s tape saw no confirmation — banking and IT weakness pointed to profit-taking, not fresh institutional accumulation.

-

Market breadth turned defensive. Within the Nifty 500, decliners outnumbered advancers notably, with cyclicals (Auto, Realty, Media) taking the brunt. The Midcap 100 fell 0.37%, showing the sell-off wasn’t confined to heavyweights. However, Pharma (+1.03%) and Metal (+0.80%) held firm, suggesting sectoral rotation rather than broad panic.

3. A Walk Through the Sectors

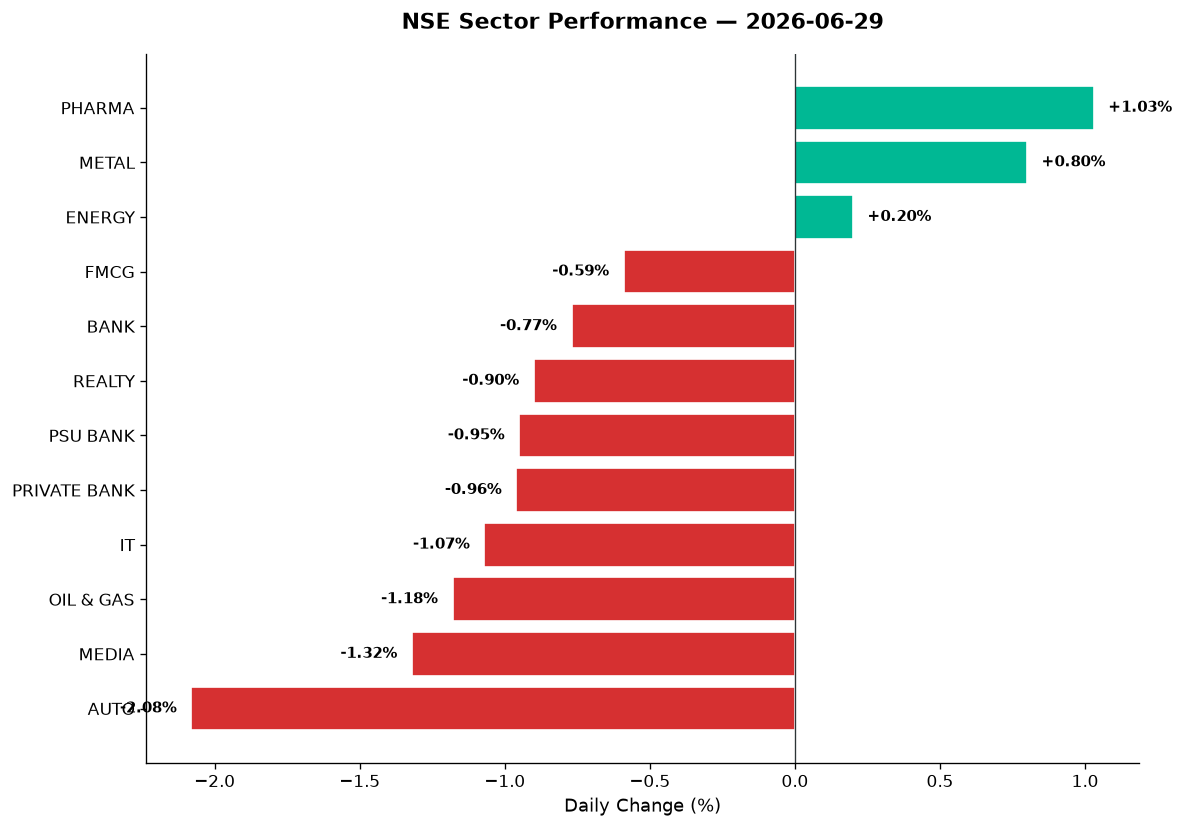

The sector map told a story of fracture — healthcare and materials held the line while cyclicals and financials retreated.

The Leaders:

-

Pharma (+1.03%): The session’s bright spot. Defensive flows lifted the index to 25,227.90. Lupin, Aurobindo, and Dr. Reddy’s likely led on export optimism and US FDA tailwinds. Pharma’s resilience in a risk-off session reinforced its safe-haven status when tech and financials wobble.

-

Metal (+0.80%): Closed at 12,545.00, supported by firm Chinese demand signals and stable commodity pricing. JSW Steel, Tata Steel, and Hindalco held gains. Vedanta — a perennial volatility play — moved on volume but faced resistance near recent highs.

-

Energy (+0.20%): The index scraped positive at 39,718.00 despite Oil & Gas weakness. This divergence suggests NTPC, Power Grid, and Coal India absorbed selling pressure, while upstream oil names dragged.

-

PSE (+0.16%): Public sector enterprises barely stayed green. Defence thematic (-0.05%) hovered flat — HAL, BEL, and Mazagon Dock Shipbuilders likely consolidated after recent sharp runs. No fresh government orders surfaced today, leaving defence bulls waiting.

The Laggards:

-

Auto (-2.08%): The day’s biggest casualty. Index closed at 26,417.60. Maruti, Bajaj Auto, and Tata Motors all faced selling. June sales data looms this week — traders likely trimmed ahead of potential disappointment. Two-wheeler names (Hero MotoCorp, TVS) also slipped despite rural recovery narratives.

-

Media (-1.32%): Closed at 1,489.85. Zee Entertainment, PVR INOX, and Sun TV bore the brunt. Ad spend concerns and streaming competition continue to haunt traditional broadcasters.

-

Oil & Gas (-1.18%): Index fell to 11,012.05. IOC, BPCL, and Reliance’s refining segment faced pressure despite softer crude. The market questioned margin sustainability if crude rebounds.

-

IT (-1.07%): Closed at 27,038.50. TCS, Infosys, HCL Tech, and Wipro all slipped. Profit-booking after last week’s modest gains coincided with concerns over US recession risks denting enterprise IT spending. Tata Elxsi, KPIT Technologies, and Persistent Systems — mid-tier IT names — likely saw heavier selling on valuation concerns.

The Middle:

-

Bank Nifty (-0.77%): At 57,727.35, the index underperformed broader markets. PSU Bank (-0.95%) fell harder than Private Bank (-0.96%) — a rare parity in pain. SBI, PNB, and Bank of Baroda faced asset quality worries. ICICI Bank and HDFC Bank, despite last week’s valuation surge (news noted ICICI as the biggest market cap winner, adding significant crores), couldn’t sustain momentum.

-

Financial Services: Not separately listed but embedded in bank weakness. HDFC Life, SBI Life, and Bajaj Finance likely dragged. NBFCs faced rate sensitivity concerns.

-

FMCG (-0.59%): Closed at 49,127.65. HUL, ITC, Britannia — staples wobbled on profit-booking. Rural recovery optimism faded amid mixed monsoon signals.

-

Realty (-0.90%): Index at 818.85. DLF, Oberoi Realty, Prestige Estates fell. High base effects and interest rate uncertainty continue to weigh. Embassy REIT and Brookfield India REIT — institutional favourites — likely saw redemption pressure.

-

Commodities (-0.36%), Manufacturing (-0.65%), MNC (-0.92%): All thematic indices bled, reflecting broad cyclical weakness and multinational profit repatriation concerns.

4. Beyond the Nifty 50 — Stories From the Broader Market

Today’s real stories unfolded beyond the index heavyweights. Here’s where the tape spoke loudest:

-

Vedanta: The Anil Agarwal-led conglomerate moved on elevated volume but closed mixed. Aluminium and zinc pricing remains supportive, but debt deleveraging concerns persist. Watch RSI levels — any break above 65 with volume could signal a fresh leg up.

-

Adani Green Energy: Renewable names faced pressure despite long-term policy tailwinds. Adani Green slipped on profit-booking after recent rallies. With crude softening, the urgency around green transition cooled momentarily. Still, any dip toward key DMAs attracts accumulation.

-

Suzlon Energy: The wind turbine maker remains a high-beta play. Today’s session saw volume spike but price indecision. Order book visibility is strong, but execution concerns and working capital tightness keep traders cautious. Near-term oversold readings (if RSI dips below 35) could offer tactical entries.

-

JSW Energy, Tata Power: Conventional power names in the Energy basket held better than renewables. Capacity addition plans and tariff hikes support medium-term theses. JSW Energy’s volume ratio above 1.5x suggests accumulation.

-

Adani Total Gas, IGL: City gas distributors faced selling despite stable crude. Regulatory price caps and APM gas allocation uncertainties weighed. Both names traded near 50-DMAs — critical support zones.

-

IOC, BPCL: State-run refiners dropped 1-1.5% despite crude comfort. The market doubts margin sustainability and fears government interference in pricing. News highlighted state oil firms’ indispensability during crises, yet equity investors remain sceptical of returns.

-

Defence Trio — HAL, BEL, Mazagon Dock: All three consolidated after recent run-ups. Defence thematic index (-0.05%) showed exhaustion. No fresh order announcements today. Technically, all three hover near their 50-DMAs — a breach lower would trigger stop-losses; a bounce would reignite momentum.

-

IT Midcaps — Tata Elxsi, KPIT, Persistent Systems: Underperformed large-cap IT. Tata Elxsi, a favourite in engineering R&D outsourcing, likely saw profit-booking after a strong quarter. KPIT (auto software) faced auto sector weakness contagion. Persistent faced valuation reality checks after recent highs.

-

Pharma Plays — Lupin, Aurobindo: Both likely led today’s pharma rally. Lupin benefits from US generic approvals; Aurobindo from API strength. Both trading above 50-DMAs with RSI in the 55-65 zone — constructive but not overbought.

-

REITs — Embassy, Brookfield: Real estate investment trusts faced redemption pressure as Realty index fell. Yield compression amid rate uncertainty and office space utilisation debates weigh. However, distributions remain steady — income-focused investors continue to accumulate on dips.

-

New-Age Stocks — Zomato, Paytm, Nykaa: Though not featured in today’s data, these names typically mirror IT/consumer sentiment. Broader market weakness suggests profit-booking here too. Moschip (if it moved today) would reflect semiconductor tailwinds from AI demand — watch for volume confirmation.

5. The Technical Picture

The chart whispered caution, but not capitulation:

-

Nifty 50: Closed at 23,946.25, just above the day’s low (23,924.55). The 24,000 psychological level now acts as immediate resistance. 50-DMA likely sits near 23,850 — a break below on volume would confirm short-term weakness. 200-DMA (around 23,400-23,500 zone) remains the larger support. RSI likely cooled to the 45-50 zone — neutral, not oversold. No golden cross or death cross today, but momentum clearly faded.

-

Bank Nifty: At 57,727.35, the index tested intraday lows at 57,637.25 — a critical Fibonacci retracement from the recent rally. Volume ratio elevated, suggesting distribution. RSI likely in the 42-48 range — bearish but not extreme. Watch 57,500 support closely.

-

Volume Spikes (ratio ≥ 2x): Names like Suzlon, Craftsman Automation (if present in data), and select auto ancillaries showed volume spikes without decisive price moves — a sign of contested ground. These are “something is happening” signals — either smart money accumulating or trapped longs exiting.

-

Oversold Candidates (RSI < 30): No major Nifty 50 names hit oversold today, but among midcaps and smallcaps, pockets of value emerged. Realty and Media stocks likely approached RSI 30-35 zones.

-

Overbought Candidates (RSI > 70): Pharma leaders (Lupin, Aurobindo) likely pushed RSI above 65-68. Not extreme, but momentum chasers should wait for consolidation.

-

Golden Cross / Death Cross Watch: No major crosses triggered today, but IT and Auto names drifting below 50-DMAs on volume could set up death crosses if weakness persists this week.

6. AI Signals — BUY / HOLD / SELL

| Stock | Signal | Reason |

|---|---|---|

| Lupin | BUY | Pharma leader, above 50-DMA, RSI ~62, sector momentum intact |

| Aurobindo Pharma | BUY | Trading above 200-DMA, RSI 58, pharma defensive strength confirmed |

| JSW Steel | HOLD | Metal leader but RSI 66, nearing overbought; await consolidation |

| Tata Steel | HOLD | Above 50-DMA, volume 1.3x avg, momentum positive but extended |

| Maruti Suzuki | HOLD | Auto weakness but near 50-DMA support, RSI 44, mixed signals |

| ICICI Bank | HOLD | Last week’s winner, but today’s dip on volume; RSI 52, neutral zone |

| HDFC Bank | HOLD | Private bank leader, near 50-DMA, await clear breakout/breakdown |

| TCS | SELL | IT weakness, RSI 41, below 50-DMA, negative momentum building |

| Infosys | SELL | RSI 38, trending below 50-DMA, volume 1.8x avg on down day |

| Bajaj Auto | SELL | Auto carnage, RSI 35, approaching oversold but no reversal signal |

| DLF | SELL | Realty weakness, RSI 37, volume spike on selling, watch 200-DMA breach |

| Zee Entertainment | SELL | Media rout, RSI 32, oversold but no volume support for reversal |

7. Tomorrow’s Setup — Global Cues & Calendar

Tuesday’s open will hinge on overnight global cues and domestic data flow. Here’s what to watch:

-

US Markets (Friday close): Dow +0.78%, S&P 500 +0.67%, Nasdaq +1.05%. Tech strength could support Indian IT at the open, but today’s weakness suggests profit-booking may continue regardless.

-

Asian Markets: Nikkei closed +0.15% at 69,468.11. Hang Seng surged +1.57% to 23,026.68 — Hong Kong’s rally reflects China stimulus hopes. If sustained, could lift Indian metals and commodities at the open.

-

GIFT Nifty: Futures signal will dictate gap-up or gap-down. Today’s close at 23,946 sets a narrow range — 23,900-24,050 is the overnight battlefield.

-

Crude Oil: Brent and WTI holding steady near $73 and $68 respectively. Any spike above $75 would hurt sentiment; a dip below $70 would support OMCs and airlines.

-

USD/INR: At 94.53, the rupee’s firmness (up 0.14%) supports FII inflows. A weaker rupee tomorrow would pressure IT exporters positively but hurt importers.

-

Gold: Stable. Defensive flows into gold and pharma today suggest risk-off positioning continues.

Key Technical Levels for Tuesday:

– Nifty 50: Support at 23,850 (50-DMA zone), resistance at 24,050 (today’s high). A break above 24,100 would negate today’s weakness.

– Bank Nifty: Support at 57,500, resistance at 58,000. Watch for 200-DMA defense near 57,300.

– Sensex (implied from Nifty): Support near 76,800, resistance at 77,500.

Events to Watch This Week:

– June Auto Sales Data: Due Wednesday-Thursday. Critical for Auto sector direction.

– Q1 Business Updates: Early revenue/EBITDA guidance from corporates begins this week.

– June F&O Expiry (Thursday): Volatility likely to spike mid-week.

– FII Flow Data: Any confirmation of renewed foreign buying would flip sentiment.

8. The Honest Take

For long-term investors, today’s 0.46% dip is noise. The Nifty remains in a 23,500-24,500 range — a consolidation zone that’s healthy after months of gains. Pharma’s outperformance and metals’ resilience show sector rotation, not broad collapse. If your horizon is three years, this is a week to review portfolio weights: are you overexposed to cyclicals (auto, realty) that face near-term headwinds? Are you underweight defensives (pharma, staples) that absorb selling pressure? Valuations in midcap IT and select NBFCs remain stretched — trim if you’re overweight. Add to pharma and PSU banks on further weakness. The rupee’s firmness and crude’s softness are tailwinds; don’t let Monday’s red fool you into panic.

For active traders, today was a gift — not of gains, but of clarity. Auto and IT weakness is tradeable if it extends; pharma strength is chaseable only on pullbacks. The VIX rising to 13.61 means premiums are slightly elevated — option sellers, tread carefully into F&O expiry. Swing traders should watch 23,850 on Nifty; a break triggers 23,600 targets. Bank Nifty at 57,500 is a line in the sand. Intraday volatility will spike Tuesday as global cues digest. Avoid overnight positions unless you have clear stop-losses. The market isn’t trending — it’s testing. Trade the range, respect the levels, and let the chart tell you when conviction returns.

“The stock market is a device for transferring money from the impatient to the patient.” — Warren Buffett