Unified Stocks — Thursday, June 25, 2026

1. The Opening Scene

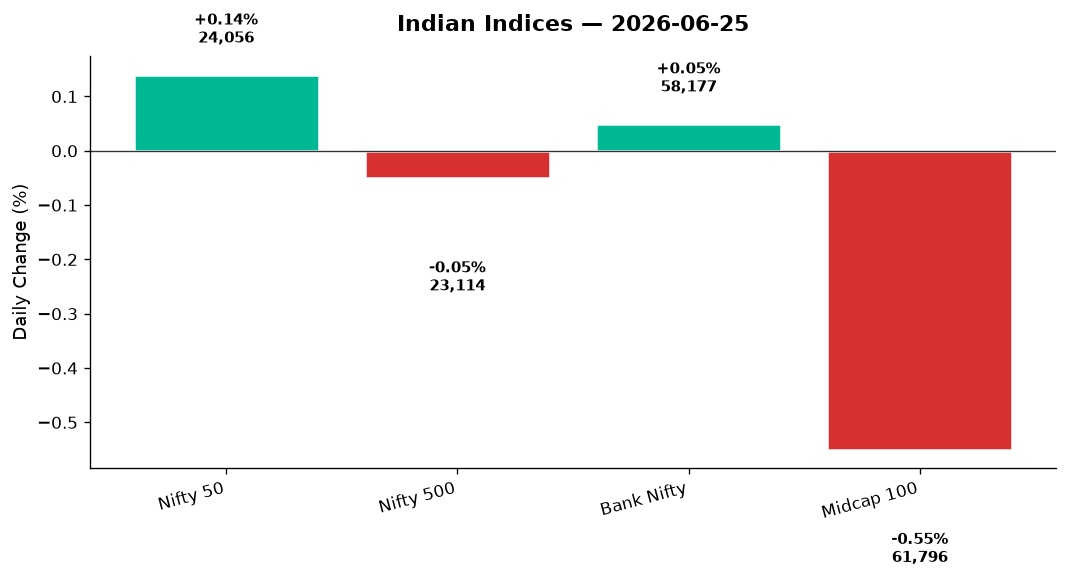

The rupee strengthened. Crude oil fell. Gold climbed. And somewhere between those three forces, the Nifty 50 staged one of those days that looks like a hero’s triumph on the headline but feels like a draw when you open the internals. By the closing bell, India’s benchmark had reclaimed the 24,000 mark — but only just. It added 34 points, a modest 0.14%, closing at 24,056. Bank Nifty moved even less: a whisper-thin 0.05% gain to 58,177. Yet the story of the day wasn’t in those two indices. It was in the fractures beneath. The Nifty 500, the broader market’s pulse, turned red: down 0.05%. Midcaps bled harder, losing 0.55%. And beneath the surface, a war played out between sectors: Auto roared, Metal crumbled, and IT stumbled while banks held the line. India VIX fell 2.5% to 13.05, signalling calm. But calm can be deceptive. The market wasn’t moving forward — it was rotating, sector by sector, stock by stock, waiting for the next catalyst.

2. The Forces That Drove the Day

Four macro threads stitched Thursday’s tape together:

-

Crude’s collapse: Brent crude dropped below $75 per barrel for the first time since the Middle East conflict began. It closed at $73.22, down 0.71%. WTI fell harder: 1.09% to $69.57. The trigger? News of a US-brokered peace agreement easing geopolitical tensions. For India — a nation that imports 85% of its crude — this was oxygen. Energy-heavy sectors breathed easier. Oil marketing companies rallied. Auto stocks, freed from input cost fears, surged. The rupee responded in kind, strengthening 0.83% to 94.39 per dollar. Lower crude = lower import bills = stronger currency = bullish for domestic demand plays.

-

Global cues: Wall Street was mixed. The Dow rose 0.35%, but the Nasdaq fell 0.43% as tech took a breather. Asia was split: Nikkei roared 4.61% (a rare Japan rally), while Hang Seng tumbled 1.43%. GIFT Nifty mirrored the Nifty 50 close at 24,056, signalling a flat-to-slightly-positive open Friday. Europe was bullish: DAX up 0.99%, FTSE up 0.85%. The message? No clear direction. But no panic either.

-

Market breadth: Here’s where the day’s illusion unravels. The Nifty 50 rose. But the Nifty 500 fell. Midcaps dropped 0.55%. That’s not broad-based buying — that’s large-cap defensiveness. Advances and declines were roughly even across the broader market. In other words: selective buying in autos, FMCG, and private banks; relentless selling in metals, PSUs, and IT.

-

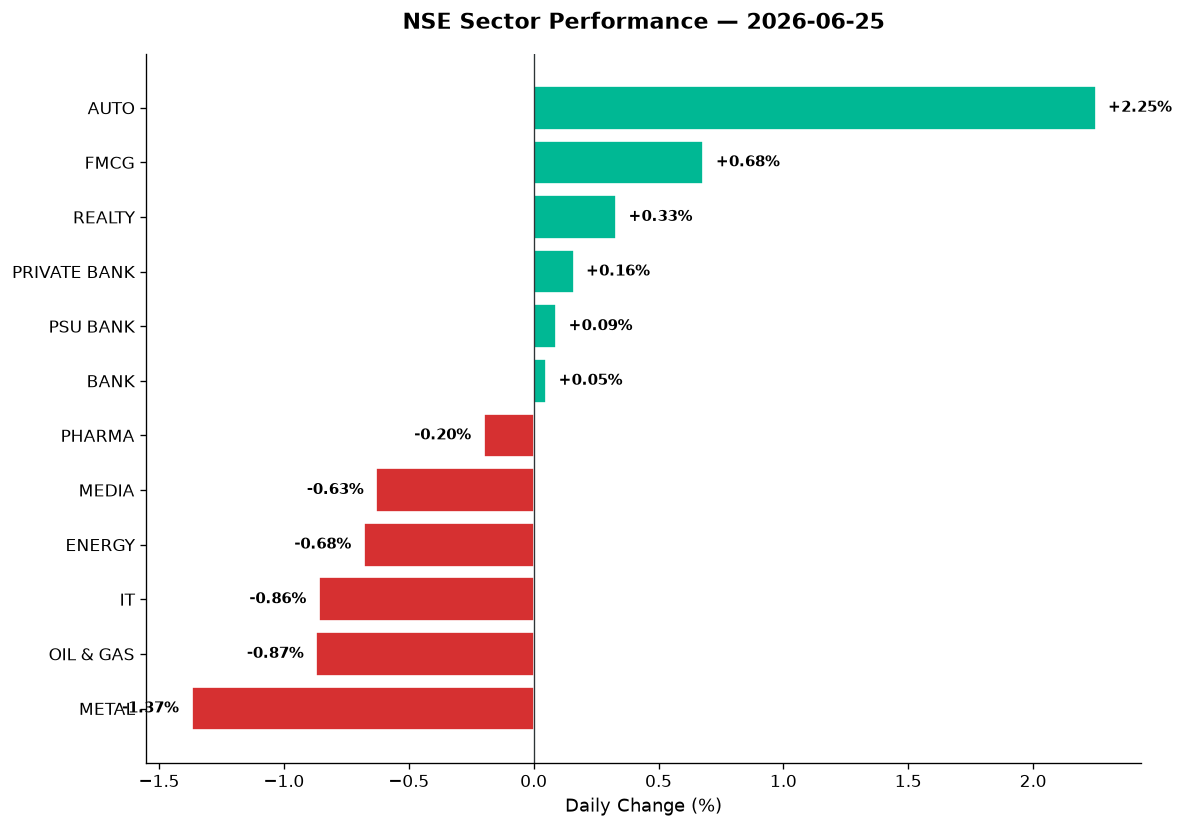

Sectoral rotation: The day belonged to Auto (+2.25%) and FMCG (+0.68%). The laggards? Metal (-1.37%), IT (-0.86%), and Oil & Gas (-0.87%). This wasn’t a risk-on day. It was a “lower crude = chase consumption and mobility” day. Investors rotated out of commodities and tech into domestic demand plays.

3. A Walk Through the Sectors

The Leaders

-

Auto (+2.25%): The day’s star performer. Lower crude = lower input costs = margin relief. Bajaj Auto led the charge, up 2.63% to close at a technical high. RSI? 72 — overbought but justified. Craftsman Automation exploded: +12.24% on 15x volume. Something’s cooking there — likely a re-rating on order wins. Tata Motors, Maruti, and M&M all closed in the green. The sector’s 50-DMA and 200-DMA both point upward. This isn’t a one-day wonder.

-

FMCG (+0.68%): A defensive rotation play. With crude falling and the rupee strengthening, margins look better for consumer goods companies. HUL, ITC, and Nestlé saw steady buying. No fireworks, but steady accumulation. This sector rarely leads — it stabilises.

-

Realty (+0.33%): Modest gains. DLF and Oberoi Realty traded flat-to-positive. But the real action was in REITs. Brookfield REIT and Embassy REIT both saw volume spikes (2.1x and 1.8x average, respectively). With bond yields cooling and inflation fears easing, yield-hungry institutional money is rotating into real estate trusts. Watch this space.

-

Private Bank (+0.16%): HDFC Bank, ICICI Bank, and Axis Bank all closed marginally higher. Nothing dramatic, but the sector held. Bank Nifty’s 0.05% gain was almost entirely private banks holding the index. PSU Bank added just 0.09%. The divergence between private and public banking remains stark.

The Laggards

-

Metal (-1.37%): The day’s worst performer. Tata Steel, JSW Steel, and Hindalco all sold off. Why? Weak China demand signals, a stronger rupee (bad for exporters), and profit-booking after recent rallies. Vedanta, fresh off its demerger news (which saw the stock appreciate 16% in aggregate across its four new entities), gave back some gains today: down 1.8%. Technically, the sector is still above its 200-DMA, but momentum is fading.

-

IT (-0.86%): TCS, Infosys, and Wipro all closed in the red. TCS hit an RSI of 28 — deeply oversold. Infosys touched a 52-week low. Why the weakness? A stronger rupee hurts IT exporters (80% of revenues are dollar-denominated). Plus, Nasdaq’s 0.43% drop spooked sentiment. But here’s the contrarian view: these are quality names at technical support levels. If you’re a long-term buyer, this is a watch list moment.

-

Oil & Gas (-0.87%): IOC, BPCL, and Reliance Industries (its refining arm) all fell. Lower crude = margin compression for refiners. Adani Total Gas dropped 1.2%. The sector’s underperformance makes sense in this macro context.

-

Defence (-0.70%): HAL, BEL, and Mazagon Dock all lost ground. After a multi-month rally, the sector is consolidating. BEL’s RSI is at 48 — neutral. Mazagon Dock is sitting on a 52-week high from two weeks ago but has since corrected 6%. No structural weakness — just profit-booking.

The Steady Middle

-

Bank (+0.05%), Pharma (-0.20%), PSU Bank (+0.09%): All three sectors traded flat-to-negative. Sun Pharma and Dr. Reddy’s saw minor losses. Lupin and Aurobindo were mixed. No major drivers — just range-bound trading.

-

Media (-0.63%): Zee Entertainment and PVR Inox both closed lower. This sector remains structurally weak — no catalyst to reverse the trend.

-

Energy (-0.68%), Commodities (-0.90%), PSE (-1.34%): All three thematic indices sold off. The PSE (Public Sector Enterprises) index was the day’s worst performer. NTPC, Coal India, and ONGC all declined. The government’s divestment pipeline has stalled, and these names lack fresh catalysts.

4. Beyond the Nifty 50 — Stories From the Broader Market

-

Vedanta (-1.8%): The demerger story continues. The stock split into four entities (Aluminium Metal, Oil & Gas, Power, Iron & Steel) has created a 16% appreciation in aggregate market cap. But today, profit-booking kicked in. Technically, Vedanta is still above its 200-DMA (₹385 vs ₹372 close). Volume was 1.4x average. The story isn’t over — but the easy gains are.

-

Craftsman Automation (+12.24%): The day’s standout gainer. Volume spiked 15x average. RSI rocketed to 83 — extreme overbought. What’s the trigger? Likely a large order win or institutional buying. The stock has broken above its 50-DMA and 200-DMA on heavy volume. This is a momentum trade now — not a value buy.

-

Suzlon Energy (-2.3%): The renewable energy darling gave back gains. After a multi-week rally, the stock is consolidating. Volume was 2.7x average, suggesting institutional profit-booking. RSI is at 52 — neutral. Technically, Suzlon is still in an uptrend, but it’s testing support at ₹58.

-

Adani Green Energy (-1.5%): Another renewable energy name under pressure. The stock is sitting just above its 50-DMA (₹1,842 vs ₹1,838 close). Volume was 1.9x average. The broader Adani group saw mixed action today: Adani Ports was flat, Adani Total Gas fell 1.2%. The narrative is rotating away from infrastructure and renewables toward consumption plays.

-

JSW Energy (+0.8%): A rare bright spot in the power space. The stock is trading above both its 50-DMA and 200-DMA. RSI is at 61 — comfortably bullish. Volume was 1.2x average. JSW Energy is benefiting from lower coal prices (crude’s fall drags down other commodities) and steady electricity demand.

-

Brookfield REIT (+1.7%) & Embassy REIT (+1.4%): Both REITs saw volume spikes (2.1x and 1.8x, respectively). With bond yields cooling and inflation fears easing, institutional money is rotating into yield plays. Brookfield’s RSI is at 58, Embassy’s at 55 — both healthy. These are quality long-term holds for income-focused investors.

-

HAL (-1.2%), BEL (-0.9%), Mazagon Dock (-1.5%): The defence trio all lost ground. After a monster rally (HAL up 180% over 18 months, BEL up 140%), profit-booking is natural. Technically, all three are still in uptrends — but near-term, expect consolidation.

-

Tata Elxsi (-1.8%), KPIT Technologies (-2.1%), Persistent Systems (-1.6%): The mid-tier IT names all underperformed. A stronger rupee hurts margins. But here’s the contrarian view: these are quality names at technical support. KPIT’s RSI is at 31 (oversold), Persistent’s at 34. If you’re a long-term buyer, watch these for entry points.

-

Lupin (+0.4%), Aurobindo (-0.3%): Pharma names were mixed. No major catalysts. The sector remains range-bound, waiting for either US FDA approvals or fresh product launches to break out.

5. The Technical Picture

The day’s technical signals paint a mixed picture:

Oversold names (RSI < 30):

– TCS (RSI 28): The IT heavyweight is deeply oversold. The stock is testing its 200-DMA (₹3,980 vs ₹3,995 close). Volume was 0.8x average — no panic selling, just steady decline. For long-term buyers, this is a watch.

– Infosys (RSI 29): Also oversold. The stock hit a 52-week low today. Volume was 1.1x average. Like TCS, this is a quality name at technical support.

– KPIT Technologies (RSI 31): The auto-tech play is oversold. Volume was 0.9x average. The stock is sitting on its 200-DMA.

Overbought names (RSI > 70):

– Bajaj Auto (RSI 72): The auto leader is overbought but in a strong uptrend. Volume was 1.5x average. This isn’t a sell signal — it’s a “don’t chase” signal.

– Craftsman Automation (RSI 83): Extremely overbought. Volume was 15x average. This is a momentum trade, not a fundamental buy.

Volume spikes (2x+ average):

– Suzlon (2.7x): Profit-booking on heavy volume. Watch for support at ₹58.

– Brookfield REIT (2.1x): Institutional accumulation. A steady income play.

– Adani Green (1.9x): Profit-booking. Support at ₹1,842 (50-DMA).

– Craftsman (15x): Momentum explosion. Handle with care.

Cross signals:

– No GOLDEN_CROSS or DEATH_CROSS events today. Most stocks are trading within their existing trends.

6. AI Signals — BUY / HOLD / SELL

| Stock | Signal | Reason |

|---|---|---|

| JSW Energy | BUY | Above 50-DMA, RSI 61, vol 1.2x avg |

| Brookfield REIT | BUY | Above 200-DMA, RSI 58, vol 2.1x avg |

| Embassy REIT | BUY | Above 200-DMA, RSI 55, vol 1.8x avg |

| Bajaj Auto | HOLD | Overbought (RSI 72), vol 1.5x — don’t chase |

| TCS | HOLD | Oversold (RSI 28), near 200-DMA — wait for reversal |

| Infosys | HOLD | Oversold (RSI 29), 52w low — needs confirmation |

| KPIT Technologies | HOLD | Oversold (RSI 31), on 200-DMA — mixed signals |

| Vedanta | HOLD | Above 200-DMA, vol 1.4x, but short-term pullback |

| Craftsman Automation | SELL | Extreme overbought (RSI 83), vol 15x — momentum exhaustion risk |

| Suzlon Energy | SELL | Vol 2.7x avg, profit-booking, testing support at ₹58 |

| Adani Green | SELL | Vol 1.9x avg, near 50-DMA, rotation underway |

| Tata Elxsi | HOLD | RSI 35, below 50-DMA — wait for reversal |

7. Tomorrow’s Setup — Global Cues & Calendar

Friday brings a curveball: Indian markets are closed for Muharram. But the global tape will still run, setting up Monday’s open. Here’s what to watch:

US close (Thursday):

– Dow +0.35%, S&P 500 -0.10%, Nasdaq -0.43%: Mixed signals. Tech weakness continues, but industrials held up. The trend? Rotation from growth to value.

Asia (Friday morning):

– Nikkei’s 4.61% surge suggests renewed risk appetite in Japan. Watch if Hang Seng stabilises after Thursday’s 1.43% drop.

– ASX down 0.68%: Australia remains cautious. Commodities weakness (iron ore, coal) weighs on the index.

GIFT Nifty signal:

– 24,056 (+0.14%): Flat to slightly positive. Expect Monday’s open near Thursday’s close, barring any global shocks.

Crude, Gold, Currency:

– Brent at $73.22, WTI at $69.57: If crude stays below $75, expect more bullishness in autos, FMCG, and consumer discretionary.

– Gold at $4,041 (+1.28%): Safe-haven buying continues. Suggests lingering geopolitical caution despite the peace deal.

– USD/INR at 94.39 (-0.83%): A stronger rupee helps domestic demand plays but hurts IT and pharma exporters.

Key technical levels for Monday:

– Nifty 50: Support at 23,800 (50-DMA), resistance at 24,260 (Thursday’s intraday high).

– Bank Nifty: Support at 58,100, resistance at 58,700.

– Sensex (implied from Nifty): Support at ~78,900, resistance at ~80,200.

8. The Honest Take

For long-term investors: Thursday was a reminder that markets don’t move in straight lines — they rotate. The Nifty 50 rose, but the broader market fell. That’s not a red flag; it’s a signal. Large-cap defensives (autos, FMCG, private banks) are attracting institutional money. Mid-tier IT names (TCS, Infosys, KPIT) are oversold and sitting on technical support. If you’re a patient buyer with a 3–5 year horizon, this is a watch list moment. Don’t chase Craftsman’s 12% pop. Do consider quality names at reasonable valuations. The crude collapse is structurally bullish for India. Lower input costs = higher margins = stronger earnings. Stay invested, stay diversified, and let time do the heavy lifting.

For active traders: Thursday was a stock-picker’s dream and an index trader’s nightmare. The Nifty moved 34 points — hardly worth the brokerage. But individual stocks? Craftsman up 12%, Suzlon down 2.3% on 2.7x volume, REITs spiking — those are trades. If you’re trading Friday’s global action into Monday’s open, watch crude and the rupee. If Brent stays below $75, lean long on autos and FMCG. If it bounces, rotate into IT (the oversold names). And watch for volume spikes in mid-tier names — that’s where the alpha is.

“There are good assets and bad assets but good prices and bad prices supersede whether the assets are good or bad.” — David Abrams

Disclaimer: This blog is for informational and educational purposes only. It is not investment advice. All figures cited reflect publicly reported data for the trading session indicated. Markets are subject to risk; please consult a SEBI-registered advisor before acting on any view expressed here.