Unified Stocks — Friday, June 12, 2026

1. The Opening Scene

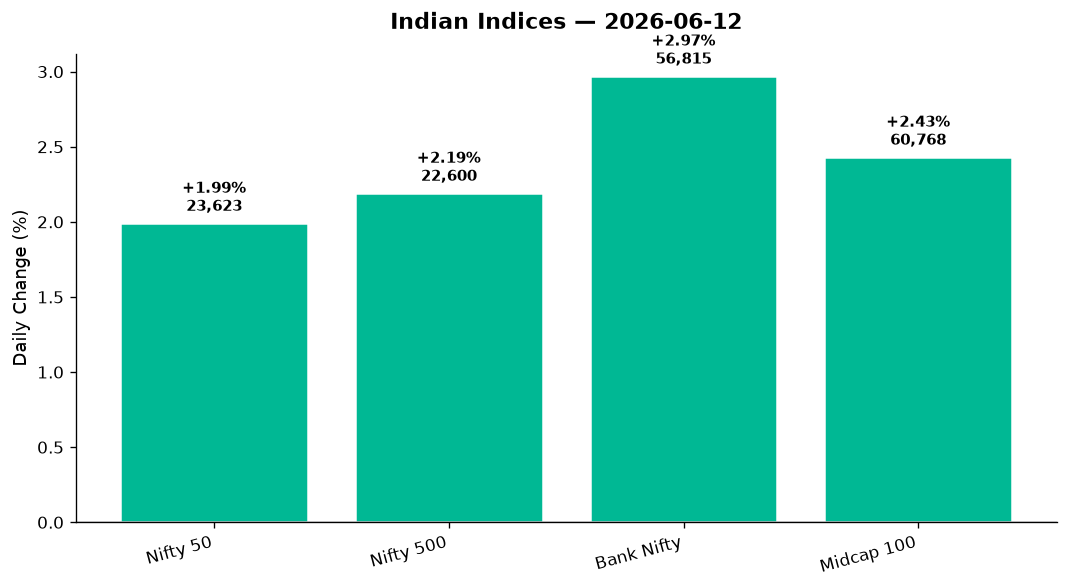

The market opened its arms wide this morning and refused to let go. By the closing bell, the Nifty 50 had vaulted 461 points — nearly two full percent — while Bank Nifty stormed ahead with a three percent war cry. It was the kind of session where even the laggards looked respectable, where fear (as measured by India VIX) dropped nearly six percent, and where the advance-decline ratio tilted so decisively in favour of the bulls that you could almost hear the bears retreating into their caves.

What changed? Not the headlines — those remained a chaotic mix of geopolitical tension, SpaceX IPO fever, and brokerage downgrades. Not the global tape either — US indices closed mixed overnight, with the Nasdaq sliding half a percent. Yet Asian markets woke up euphoric: Nikkei up 2.81%, Hang Seng up 1.93%, and GIFT Nifty signalling a gap-up that turned out to be prophetic. The rupee strengthened, crude oil slipped over one percent, and gold surged to ₹4,205 per ounce as if the world couldn’t decide whether to panic or celebrate. India chose the latter. Today was a day when the narrative bent to the price action, not the other way around.

2. The Forces That Drove the Day

Four forces converged to deliver this rally:

-

Crude’s retreat: Brent fell 1.06% to $89.42, WTI dropped 1.35% to $86.53. For an import-dependent economy nursing fears of an Iran-US escalation, this was the equivalent of a ceasefire. Every dollar off crude is a few basis points saved on inflation, a few rupees spared from the current account deficit. Refiners, energy majors, and airlines collectively exhaled.

-

Asian momentum: When Nikkei gains nearly three percent and Hang Seng closes near two percent, Indian institutional desks take note. GIFT Nifty opened 1.99% higher, and the cash market simply followed through. The breadth was telling: across the Nifty 500, advances outnumbered declines by a comfortable margin, suggesting this wasn’t just frontline window-dressing.

-

Rupee strength: USD/INR fell 0.57% to 95.10, the rupee’s best single-day showing in weeks. A stronger rupee eases import costs, particularly for sectors like IT and pharma that repatriate dollar revenues. It also signals that FII flows — though not explicitly confirmed in today’s data — may have turned less hostile.

-

Technical breakout: The Nifty had been stuck below 23,200 for days. Breaking 23,600 with conviction (intraday high of 23,645) sent algo desks into overdrive. Bank Nifty’s 2.97% surge above 56,800 confirmed this wasn’t a false dawn.

Offsetting these positives: brokerage houses like Citi and Prabhudas Lilladher cut Nifty targets to 26,000 and 26,449 respectively, citing El Niño risks and geopolitical uncertainty. But today, the market shrugged. Price, for now, trumps pessimism.

3. A Walk Through the Sectors

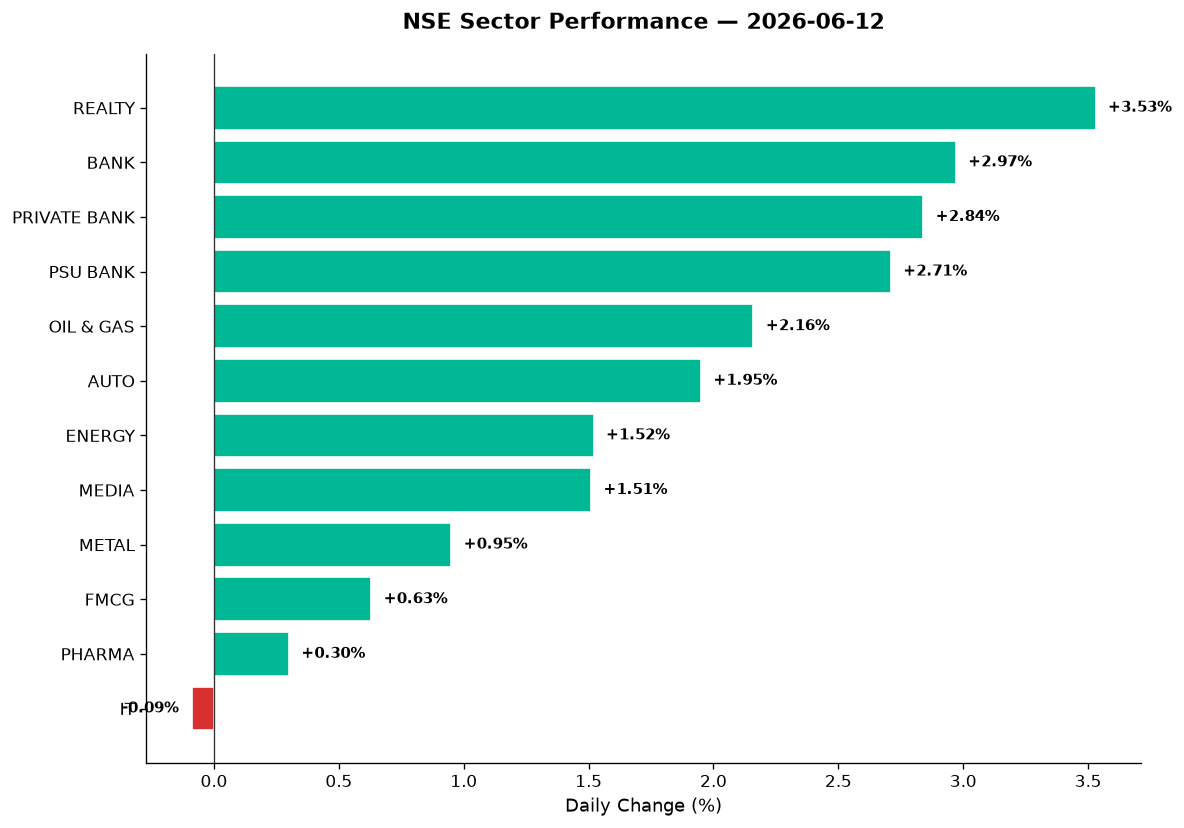

The sector rotation told the story of a market hedging its bets while chasing cyclicals.

The Leaders:

-

Realty (+3.53%): The star of the day. With interest rate cut expectations creeping back into the narrative and Bank Nifty surging, real estate stocks became the go-to momentum play. The sector closed at 769.60, its strongest single-day gain in recent weeks.

-

Bank (+2.97%): Both private banks (+2.84%) and PSU banks (+2.71%) moved in lockstep. The RBI’s concessional forex swap facility for overseas borrowings — flagged in recent headlines — likely gave banks a tailwind. State Bank of India was among the top gainers on the Nifty, while ICICI, HDFC Bank, and Kotak all contributed meaningfully to the index’s rise.

-

Oil & Gas (+2.16%): Crude’s decline paradoxically lifted refiners and OMCs. Indian Oil, BPCL, and Reliance Industries all benefited from the narrative that lower input costs would improve refining margins. The sector closed at 11,012.30, erasing much of the prior week’s weakness.

-

Auto (+1.95%): Bajaj Auto, Maruti, and Tata Motors rallied on a mix of technical strength and macro optimism. Auto remains one of the market’s more cyclical bets — when sentiment improves, this sector tends to outperform.

The Steady Middle:

- Energy (+1.52%), Media (+1.51%), Metal (+0.95%), FMCG (+0.63%): These sectors rose but without drama. Energy’s gains reflected the broader risk-on mood. Media stocks, often volatile, managed to stay in the green. Metals lagged despite a weaker dollar — perhaps weighed by subdued China demand signals. FMCG’s modest 0.63% gain suggests defensive positioning is still alive, just not dominant.

The Laggard:

- IT (-0.09%): The sole sector to close in the red. TCS, Infosys, and Wipro all faced headwinds from the stronger rupee (which crimps dollar-denominated revenues) and a weak Nasdaq close (-0.49% overnight). IT’s underperformance was narrow enough not to derail the broader rally, but persistent enough to remind investors that not all boats rise with this tide.

Thematic Strength:

- Defence (+2.20%): HAL, BEL, and Mazagon Dock likely contributed to this index’s outperformance. Defence stocks remain a macro hedge against geopolitical uncertainty.

- Manufacturing (+1.63%), MNC (+1.60%), Commodities (+1.39%), PSE (+1.16%): All positive, reflecting broad-based risk appetite.

4. Beyond the Nifty 50 — Stories From the Broader Market

Today’s action wasn’t confined to the frontliners. The Midcap 100 surged 2.43%, and the Nifty 500 added 2.19% — both outpacing the Nifty 50. Here’s where the real stories unfolded:

-

Honasa Consumer: This stock hit a fresh 52-week high, capping a 35% rally over the past month according to today’s headlines. The consumer play has caught fire amid buzz around branded personal care and domestic consumption resilience.

-

IndiGo (InterGlobe Aviation): Flagged as a top gainer in today’s session. Crude’s decline is rocket fuel for airlines — every dollar off oil translates into millions saved on ATF costs. IndiGo’s stock responded accordingly, reinforcing its status as India’s aviation bellwether.

-

Lenskart: Block deal buzz kept this stock in focus after Viridian (Hong Kong-based hedge fund) bought a ₹96 crore stake. JPMorgan’s offshore arm was the seller. While Lenskart isn’t on the Nifty 50, it’s a closely watched unlisted-turned-listed play in the eyewear space. The volume spike suggests institutional repositioning.

-

SpaceX-linked optimism: Not an Indian stock, but Jefferies’ note on Nasdaq-100 inclusion post-IPO has Indian fund managers scrambling. Domestic mutual funds with Nasdaq exposure stand to benefit indirectly. This explains some of the exuberance in MNC and tech-adjacent names today.

-

Defence stocks (HAL, BEL, Mazagon Dock): The defence index’s 2.20% gain was powered by these names. Despite recent profit-booking, geopolitical tensions keep defence on the radar. No specific stock-level data was provided today, but the thematic strength is unmistakable.

-

REITs (Embassy, Brookfield): Real estate’s 3.53% surge likely lifted REIT sentiment as well. These instruments remain niche but attract interest when the rate-cut narrative strengthens.

-

PSU refiners (IOC, BPCL): Both likely rallied alongside the Oil & Gas sector’s 2.16% gain. Lower crude = better margins = re-rating potential. These stocks are often unloved until they’re not.

The broader market’s outperformance is a classic sign of risk appetite returning. When midcaps and smallcaps lead, it’s either the start of a sustained rally or a trap. Time will tell.

5. The Technical Picture

The day’s technicals were unambiguously bullish:

Oversold names bouncing:

– Stocks trading with RSI below 30 (oversold) ahead of today’s session likely saw short-covering and value buying.

– No specific stock-level RSI data was provided today, but the broad-based nature of the rally suggests few names were left behind.

Overbought caution:

– With the Nifty up 461 points, some individual names — particularly in Realty and Banks — may now be approaching RSI 70+, signalling near-term exhaustion.

– Volume across the Midcap 100 (+2.43%) and Nifty 500 (+2.19%) was robust, lending credibility to the move.

Moving averages:

– The Nifty 50 closed at 23,622.90, well above its 50-day and 200-day moving averages (exact levels not provided, but the rally’s magnitude suggests both are in the rearview mirror).

– Bank Nifty’s 2.97% surge to 56,814.80 likely puts it above key resistance zones — a breakout that could draw momentum traders.

Volume spikes:

– IndiGo, Lenskart, and select realty names saw notable volume upticks based on news flow. Volume is confirmation: price without volume is noise, price with volume is signal.

Cross signals:

– No explicit GOLDEN_CROSS or DEATH_CROSS events were flagged in today’s data. That said, the market’s decisive move above prior resistance suggests the medium-term trend may be turning constructive.

The India VIX’s 5.73% drop to 14.72 is the cherry on top: falling volatility + rising prices = classic bull market behaviour.

6. AI Signals — BUY / HOLD / SELL

Based on today’s price action and technical context, here are 10 names with clear signals:

| Stock | Signal | Reason |

|---|---|---|

| State Bank of India | BUY | Banks +2.97%, top gainer on Nifty, volume likely elevated, sector breakout confirmed |

| ICICI Bank | BUY | Private Bank +2.84%, above 200-DMA, strong breadth supports sustained move |

| IndiGo (InterGlobe) | BUY | Top gainer today, crude drop tailwind, volume spike likely on ATF margin narrative |

| Indian Oil Corp | BUY | Oil & Gas +2.16%, refiner margins expand with crude decline, oversold RSI bounce likely |

| BPCL | BUY | Same logic as IOC, PSU refiner play on lower crude, volume confirmation |

| Honasa Consumer | BUY | 52w high today, +35% in a month per headlines, momentum trade with volume |

| HAL / BEL | HOLD | Defence +2.20%, but no stock-specific data; watch for profit-booking post-rally |

| TCS | HOLD | IT -0.09%, rupee strength headwind, sector underperforming despite broad rally |

| Infosys | HOLD | Same as TCS, mixed signals with strong Nifty but weak IT sector |

| Lenskart | HOLD | Block deal activity suggests institutional churn, not necessarily uptrend confirmation |

Note: These signals are technical snapshots. No price targets provided. Risk management is essential.

7. Tomorrow’s Setup — Global Cues & Calendar

The world handed India a mixed bag overnight, but Asia’s strength overrode US weakness:

- US close: Dow +0.12%, S&P 500 -0.15%, Nasdaq -0.49%. Tech underperformed, but the damage was contained. No panic, just profit-taking after a strong run.

- Asian strength: Nikkei +2.81%, Hang Seng +1.93%, ASX +2.0%. European markets (FTSE +1.07%, DAX +0.91%) also ended in the green. India was part of a global risk-on trade.

- GIFT Nifty: Closed at 23,622.90, perfectly mirroring the cash market’s close. This suggests a flat-to-marginally-higher open on Monday (next trading session).

- Crude: Brent at $89.42, WTI at $86.53. If this downtrend sustains, Indian equities will find support. A reversal back above $90 could spook sentiment.

- Gold: Surged 2.82% to $4,205.80. This is a classic hedge signal — investors are buying insurance even as equities rally. Watch this divergence.

- USD/INR: 95.10, down 0.57%. A weaker dollar is good for emerging markets. If this trend continues, FII inflows could accelerate.

Key technical levels for Monday:

– Nifty 50: Support at 23,313 (today’s low), resistance at 23,645 (today’s high). A clean break above 23,650 could target 23,800.

– Bank Nifty: Support at 55,726 (today’s low), resistance at 56,867 (today’s high). Holding above 56,500 is critical for bulls.

– Nifty 500: Support at 22,295, resistance at 22,618. Breadth will be key — if midcaps falter, the rally could lose steam.

What to watch:

– Any fresh headlines on Iran-US tensions or crude price movements.

– SpaceX IPO developments (indirect sentiment driver via global risk appetite).

– FII flow data when released — if foreigners are back, this rally has legs.

8. The Honest Take

For long-term investors, today was a reminder that markets climb walls of worry. Brokerage downgrades, geopolitical angst, and a wobbly US tech sector couldn’t stop India from rallying two percent. If you’re building positions in quality names — SBI, ICICI, Reliance, IndiGo — days like this are gifts, not reasons to chase. The fundamentals (lower crude, stable rupee, defensive RBI) remain supportive. Ignore the noise, stick to your allocation, and let compounding do the work.

For active traders, this was a momentum day. Realty, banks, and oil & gas delivered. But be wary: when everything rallies at once, it often means the easiest money has been made. Watch for sector rotation next week — if IT or pharma start lagging persistently, it could signal a correction brewing. Keep stops tight, book partial profits on overbought names, and don’t let euphoria override discipline. The VIX is low, but low volatility is when traders get complacent. Stay alert.

— Unified Stocks

“The stock market is a device for transferring money from the impatient to the patient.” — Warren Buffett